Under ordinary circumstances, an earnings beat represents cause for celebration. When it came to market rewards, Workday (NASDAQ:WDAY) enjoyed its just desserts as its stock rallied to reflect brewing enthusiasm for the underlying cloud-based financial and human-capital management industries. Still, the market represents a forward-looking concept, which raises questions for the enterprise. Therefore, I am neutral on WDAY.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Admittedly, a middle-of-the-road perspective contrasts with the excitement that Workday generated among its cloud-computing peers. Throughout this year, several companies disclosed concerns about negative impacts on their cloud businesses. Therefore, when Workday posted its impressive results for the third quarter, it got market observers to believe again.

According to TipRanks reporter Vince Condarcuri, Workday posted adjusted earnings per share of $0.99, beating out analysts’ consensus estimate of $0.84 per share. Further, “sales increased by 20.3% year-over-year, with revenue hitting $1.6 billion. This beat analysts’ expectations of $1.586 billion.”

Looking forward, Condarcuri wrote, “management raised the low end of its Fiscal Year 2023 subscription revenue guidance to a range of $5.555 billion to $5.557 billion. In addition, it raised its Fiscal Year 2023 non-GAAP operating margin guidance to 19.2%.”

Finally, “Workday is now able to repurchase up to $500 million worth of its own shares through its new buyback program.”

Better yet, analysts weighed in on WDAY stock, largely with a positive framework. “Workday delivered a perfect ‘holiday cocktail’ for investors,” Evercore analyst Kirk Materne wrote in a research report during the midweek session. Presently, Materne has an “outperform” rating for WDAY, along with a $225 price target.

As well, analysts from Mizuho and Oppenheimer reiterated their bullish ratings, anticipating durable growth ahead. Still, it might not hurt to add a little bit of skepticism toward WDAY stock.

WDAY Stock and the Incoming Macro Challenges

Although management posted commendable results for Q3 – especially in light of negative trends in the industry – WDAY stock isn’t exempt from challenges. Unfortunately, no one financial disclosure can entirely change an entity’s paradigm. For Workday, macroeconomic headwinds impose major significant obstacles.

Primarily, WDAY stock may face an erosion of its underlying total addressable market. Because of the confluence of negative catalysts – skyrocketing inflation, a subsequently hawkish Federal Reserve, and supply chain disruptions, to name but a few – several companies announced layoffs.

Unlike prior pink slip distributions, though, many of these cuts now center on white-collar workers. For instance, Amazon (NASDAQ:AMZN) plans to cut about 10,000 workers. According to people familiar with the matter, the cuts won’t impact factory workers. Rather, they will target white-collar employees.

The more high-level, technology-oriented occupations get the proverbial axe, the less likely Workday can continue to enjoy its expansionary trek uninterrupted.

Moreover, as a Forbes article from 2020 mentioned, the cloud is the backbone of remote work. That being the case, investors must ask themselves an important question: what happens if remote work fades away as society comes to grips with COVID-19?

Signs have already materialized that a return to workplace normalization may occur. Per a report by Resume Builder, 90% of surveyed companies stated they will require employees to return to the office at least part of the week in 2023. Of course, a vast majority of workers balked at such notions. Given labor shortages earlier, many companies had no choice but to cave to their employees.

However, as recessionary pressures build and labor markets cool, worker bees start to lose their bargaining power. Since companies tend to be more financially resilient than individuals, employees may cave. If so, the mass-scale return to the office could diminish Workday’s COVID-enhanced relevance.

Is WDAY Stock a Buy?

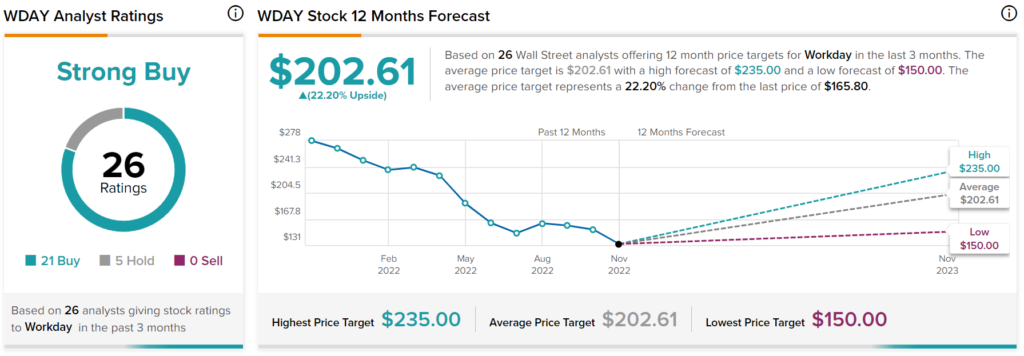

Turning to Wall Street, WDAY stock has a Strong Buy consensus rating based on 21 Buys, five Holds, and zero Sell ratings. The average WDAY price target is $202.61, implying 22.2% upside potential.

Conclusion: Quantitative Data Presents a Perplexing Picture

While WDAY stock may struggle against sector obstacles in the months ahead, it’s far from a lost cause. For instance, despite the turmoil of the market this year, Workday’s Altman Z-Score hit 3.06, reflecting a business that’s generally safe from bankruptcy risk. Still, even in the quantitative financial metrics, WDAY presents a perplexing case.

Most notably, the company’s gross margin stands at 72.23%, beating out nearly 79% of its software competitors. In addition, such a high margin implies flexibility in terms of economies of scale. Should economic pressures continue to mount, Workday appears to have branding and pricing advantages relative to its peers.

However, if circumstances get really bad, these advantages might not matter. Enterprise-level clients may cut to the bone, or they may seek out the absolute cheapest service alternative. It doesn’t help that Workday’s GAAP profit margins are in the negative.

Therefore, investors should be cautious about WDAY stock. Although the underlying company posted encouraging Q3 results, it’s not clear that it can continue exceeding expectations.