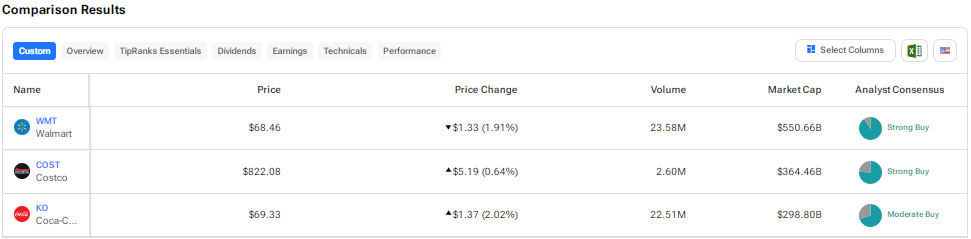

Consumer staples companies generally tend to be resilient during challenging macroeconomic times. This is because they sell products that are considered essential for daily life. Using TipRanks’ Stock Comparison Tool, we placed Walmart (WMT), Costco (COST), and Coca-Cola (KO) against each other to find the best consumer staples stock, according to Wall Street analysts.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Walmart (NYSE:WMT)

Shares of big-box retailer Walmart have rallied about 30% so far this year. WMT impressed investors with its upbeat results for Q1 FY25 (ended April 30, 2024). The 22% growth in Q1 FY25 adjusted earnings per share (EPS) was driven by strong revenue growth, higher gross margin, and membership income.

Walmart’s value offerings continue to attract bargain-seeking customers amid a tough macro backdrop. The company’s grocery business is witnessing strong growth, with many customers preferring to cook at home than dine out at restaurants due to high inflation.

WMT is also gaining from the strength in its e-commerce business. In Q1 FY25, WMT’s e-commerce sales increased 21%, fueled by store-fulfilled pickup and delivery and the company’s growing marketplace. Importantly, the company is trying to enhance its profitability by focusing on high-margin businesses like advertising, membership, marketplace and fulfillment solutions, and data analytics and insights.

Walmart is scheduled to announce its fiscal second-quarter results on August 15. Analysts expect the company’s EPS to increase by 6.5% to $0.65 per share and revenue to grow over 4% to $167.4 billion.

Is Walmart a Good Stock to Buy Now?

Last week, BMO Capital analyst Kelly Bania raised the price target for WMT stock to $80 from $75 and reaffirmed a Buy rating following meetings with the company’s management. The analyst stated that Walmart is well-positioned to increase its EBIT (earnings before interest and taxes) at a faster rate than sales, even as the company continues to make growth investments.

The analyst thinks that management’s expectation of the U.S. e-commerce operations turning profitable in the next one to two years is achievable. Her optimism is backed by a 40% reduction in delivery costs in recent quarters, the benefits of supply chain automation, and a rise in the number of customers agreeing to pay for faster delivery options.

Walmart stock earns a Strong Buy consensus rating, backed by 27 Buys and three Holds. The average WMT stock price target of $74.11 implies 8.3% upside potential. WMT offers a dividend yield of 1.2%.

Costco Wholesale (NASDAQ:COST)

Membership-only warehouse chain Costco Wholesale continues to impress investors with its consistent performance. Costco’s resilient performance is supported by its value offerings and a loyal customer base. The company generally enjoys membership renewal rates of around 90%.

Despite macro pressures, Costco announced better-than-expected June sales. The company’s net sales for the retail month of June (five weeks ended July 7, 2024) increased 7.4% to $24.48 billion. Comparable sales for June rose 5.3%, with e-commerce sales growing 18.4%.

The company recently announced the much-awaited increase in its membership fee. Investors cheered the news as Costco’s membership fee accounts for a significant portion of its operating profit.

What is the Target Price for Costco?

Following the announcement of the membership fee increase, TD Cowen analyst Oliver Chen increased the price target for Costco stock from $850 to $925 and reaffirmed a Buy rating.

The analyst believes the company’s digital innovation, personalization, and marketplace opportunities support its premium valuation.

With 19 Buys versus six Holds, Costco stock is assigned a Strong Buy consensus rating. The average COST stock price target of $910.05 implies about 11% upside potential. Shares have advanced 24.5% so far this year. COST stock offers a dividend yield of 0.5%.

Coca-Cola (NYSE:KO)

Shares of soda giant Coca-Cola have risen about 18% year-to-date. Last month, the company announced better-than-anticipated results for the second quarter, with organic revenue rising 15%. The company’s performance reflected strong execution in a challenging business backdrop.

Given the solid Q2 results, KO raised its full-year organic revenue growth guidance to the range of 9% to 10% compared to the prior outlook of 8% to 9%. The company also increased its comparable earnings growth outlook.

Last week, Coca-Cola was in the news due to an unfavorable development related to its legal dispute with the U.S. Internal Revenue Service. The company is required to pay $6 billion in back taxes and interest to the IRS. While Coca-Cola will pay the tax penalty, it will appeal the federal tax court’s decision.

TD Cowen analyst Robert Moskow stated that there could be adverse implications for the company’s tax rate if KO loses the appeal, though “relatively minor.” The analyst added that his EPS estimates would come down by nearly 5% if KO’s tax rate increased to 24% from 19%.

Is KO a Good Stock to Buy?

Most analysts covering KO stock remain bullish on its prospects. In reaction to Coca-Cola’s Q2 earnings, RBC Capital analyst Nik Modi reaffirmed a Buy rating on KO stock and raised his price target to $68 from $65, citing strong top-line growth, volume momentum, and high-quality earnings in the quarter.

However, the analyst pointed out the company’s commentary about a softer third quarter due to tough comparisons on a sequential basis and softness in some developed markets.

Overall, Coca-Cola has a Moderate Buy consensus rating based on 14 Buys and six Holds. The average KO stock price target of $69.79 indicates that the stock is fairly valued at current levels. KO offers a dividend yield of 2.8%.

Conclusion

Wall Street is highly bullish on Costco and Walmart and cautiously optimistic about Coca-Cola. Currently, analysts see comparable upside potential in Costco and Walmart stocks. Both these stocks have proved the strength of their business models and continue to attract customers with their value proposition.

While Wall Street has a Strong Buy rating on both COST and WMT stocks, it is interesting to note that hedge funds have a Very Positive Confidence Signal on WMT stock but a Negative signal on Costco. Hedge funds increased their WMT holdings by 11.5 million shares last quarter. In contrast, hedge funds decreased their COST holdings by 1.1 million shares in the same period.