At one point in 2021, shares of PayPal (NASDAQ:PYPL) traded hands at over $300. However, with a price of around $62 at writing, it’s much more difficult to convince investors to take a stab at the digital payments specialist. Nevertheless, with buy now, pay later (BNPL) platforms rising in popularity, the relative discount in PYPL stock makes it a bullish idea worth considering.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

PYPL Stock Enjoys a Possible Avenue for Relevance

During the initial fallout of the COVID-19 pandemic, many people turned to retail therapy – dubbed retail revenge – to help lift sunken moods. However, with the crisis fading rapidly, this consumer-focused phenomenon gave way to another: revenge travel. Suddenly, PayPal’s core business of digital payment services didn’t quite make sense, leading to a severe erosion of PYPL stock.

Factor in dramatically boosted competition in the broader payments ecosystem, and longtime stakeholders could only watch – if they didn’t dump shares themselves – as PYPL stock effectively collapsed. However, after the brutal beatdown, it’s possible that an avenue for reemerged relevance has materialized.

As TipRanks reporter Amit Singh mentioned, e-commerce spending during Black Friday increased by 7.5% to hit a record tally of $9.8 billion in the U.S. Obviously, this dynamic offers significant implications for PYPL stock. Moreover, The Wall Street Journal (WSJ) pointed out that the traditional start to the holiday shopping season was strong.

Still, the WSJ observed a wrinkle: it wasn’t just about consumers spending during a period of stubbornly high inflation and rising interest rates. Rather, people turned to BNPL apps and services to pay for their products. Increasingly, this payment methodology has garnered popularity by facilitating the breakdown of large payments across multiple installments.

To be sure, it would not be an easy feat for PayPal to break into the BNPL ecosystem. Yes, it already offers a BNPL service via its Pay in 4 directive. Unfortunately, though, the company was late to the party, with entities like Affirm (NASDAQ:AFRM) offering BNPL services last decade. Still, it’s better late than never.

PayPal’s Roadmap to BNPL Relevance

While it might be easy to dismiss PYPL stock, given its steep losses in the market since 2021 and its late entry into the BNPL ecosystem, from an optimistic framework, PayPal offers an underappreciated investment idea. Even better, the roadmap to relevance isn’t entirely speculative (though it obviously comes with risks).

As another WSJ article stated, in 2020, PayPal saw more than $20 billion worth of in-store volume across its payment types. That might sound like a lot. However, it’s a relative pittance compared to the nearly $1 trillion in total payment volume it posted during the aforementioned year. Still, the company has its foot wedged between the door and the frame.

Granted, competitors will be seeking to crush that foot. While some optimism for an economic recovery exists, other signals – such as the recent decline in luxury watch sales – suggest that the consumer discretionary market is waning. Therefore, rivalries may intensify for a possibly declining addressable market.

However, PYPL stock arguably deserves consideration. No, the underlying enterprise hasn’t always made the right decisions. However, we’re talking about a company that was founded in December 1998. According to some statistics, 431 million people use PayPal worldwide.

That’s a level of trust and brand recognition that BNPL up-and-comers can’t quite match.

Comparatively Undervalued

Currently, PYPL stock trades at 17.5x trailing-year earnings and 2.3x revenue. By themselves, these stats aren’t particularly remarkable. However, when stacked against a direct BNPL competitor like Affirm, it’s difficult not to notice the relative value proposition.

For one thing, Affirm posts net losses, so it’s impossible to make a trailing-earnings-based valuation comparison. As for sales, AFRM trades at a revenue multiple of 7.3x. If you’re going to speculate on a risky industry, you might as well gamble on the more credible and undervalued idea.

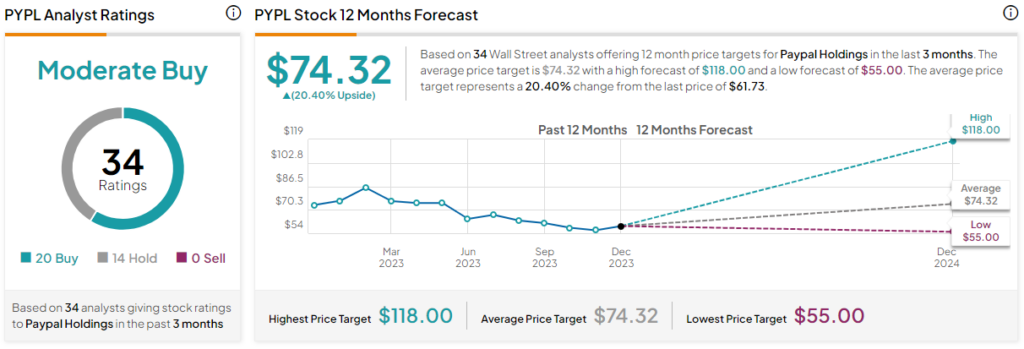

Is PYPL Stock a Buy, According to Analysts?

Turning to Wall Street, PYPL stock has a Moderate Buy consensus rating based on 20 Buys, 14 Holds, and zero Sell ratings. The average PYPL stock price target is $73.13, implying 20.4% upside potential.

The Takeaway: PYPL Stock May Be on a Comeback

Despite a tough 2021 and late entry into the BNPL market, PayPal’s brand recognition, massive user base, and potential for BNPL integration make it a compelling investment. PYPL trades at a significant discount compared to BNPL rivals like Affirm, offering value for investors seeking long-term growth in the rapidly expanding BNPL space.