Chinese e-commerce giant Alibaba Group (NYSE:BABA) is scheduled to release its Fiscal Q4 earnings on May 18, before the market opens. Ahead of the results, Mizuho Securities analyst James Lee remains bullish on the stock’s prospects and expects the company to benefit from the recovering Chinese economy.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The analyst believes retail revenues will remain stable compared to the year-ago quarter. Further, he expects Alibaba’s wholesale business to witness 5% growth “driven by a recovery in business sentiment post-reopening.”

Additionally, Lee sees 14% year-over-year growth in revenue from BABA’s International Commerce unit. This is based on the upbeat performance of AliExpress and exports’ accelerating growth due to the improved European macro climate.

In addition, topline growth for the Cloud segment is projected to increase by 5%. In this regard, Lee claimed that “as China reopens and enterprise sentiment improves, China’s cloud market should be in the recovery stage.”

Lee reiterated a Buy rating on BABA stock on May 9 but lowered the price target to $145 from $155.

Overall, the Street expects BABA to post an adjusted profit of $1.37 per ADS in Q4, compared to the year-ago quarter figure of $1.14 per ADS. Meanwhile, revenue is pegged at $30.05 billion, 6.5% lower than Q4FY22’s revenue of $32.14 billion.

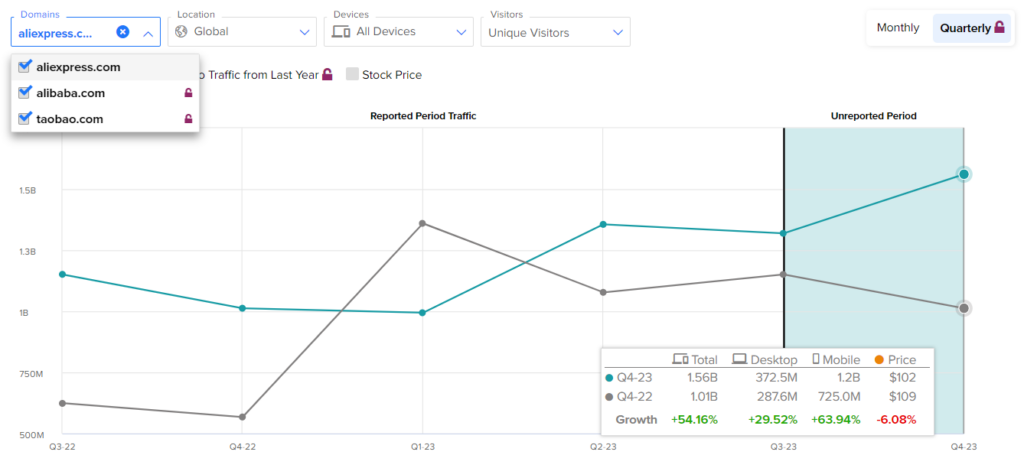

Website Traffic Reflects an Encouraging Picture

The TipRanks’ Website Traffic Tool suggests that things are improving for Alibaba. Our website traffic screener shows that the number of visits to Alibaba’s websites — aliexpress.com, alibaba.com, and taobao.com increased by 54.2% (year-over-year) for the fiscal fourth quarter.

Is BABA a Buy or Hold?

On TipRanks, analysts remain highly optimistic about Alibaba’s long-term potential. With 17 unanimous Buys, BABA stock commands a Strong Buy consensus rating. Moreover, the analyst’s price target of $149 implies 67.9% upside potential.

Ending Thoughts

The company’s broad overhaul plan, which involved splitting the company into six smaller and economically viable units, is likely to support growth. Investors will be closely monitoring the management’s remarks regarding Alibaba’s development since the launch of its own AI-driven chatbot named Tongyi Qianwen last month.