Big-picture thinking is fine. However, when it comes to Wells Fargo’s (WFC) latest round of financial results, the devil is in the details, as the old saying goes. As Wells Fargo shares push toward all-time highs, I am neutral on WFC stock because Wells Fargo’s top-line and bottom-line figures are actually contracting, not expanding, and that’s a cause for concern.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Wells Fargo is a banking giant in the U.S. Consequently, Wells Fargo is highly sensitive to interest rates. That’s a mixed blessing since interest rates are coming down now, and this means borrowing activity will probably pick up, but Wells Fargo will likely have to lower its interest rates on loans.

Frankly, it’s difficult to predict how interest-rate changes will ultimately affect Wells Fargo. What we can do right now, however, is examine Wells Fargo’s recently released data points and how the market responded to that data. I propose that some investors are too optimistic now, especially based on the actual facts that are currently available to the public.

A Note about Wells Fargo’s Valuation

If you’re looking through TipRanks’ Analysis page for Wells Fargo, which I highly recommend, you might notice Wells Fargo’s price-to-earnings (P/E) ratio. From that, you may conclude that the company’s valuation is quite low, and therefore, it’s a great time to load the boat on WFC stock. However, don’t make any hasty investment decisions.

First of all, Wells Fargo’s GAAP-measured trailing 12-month (TTM) P/E ratio is 12.74x, which is lower than the sector median of 13.48x but not by a very wide margin. If we use non-GAAP measurements, Wells Fargo’s TTM P/E ratio is 11.42x versus the sector median of 12.25x. In other words, Wells Fargo’s valuation might be moderately more favorable than the median, but we’re not talking about a “screaming buy” or a once-in-a-lifetime bargain here.

Besides, I invite you to check the stock price chart for Wells Fargo. This tells a tale that the P/E ratio doesn’t. WFC stock jumped 5.61% to $60.99 on Friday, followed by 2% more at the time of writing. This stock is up by more than 50% over the past 12 months. Unless Wells Fargo’s recent financial results are across-the-board spectacular – and in a moment, we’ll discover that they’re not – it’s probably time to take profits, not add to your share position.

Wells Fargo’s Bottom-Line Stats

The good news about Wells Fargo’s bottom-line stats in 2024’s third quarter is that the company reported earnings of $1.42 per share, thereby beating Wall Street’s consensus estimate of $1.28 per share. On the other hand, this still marks a decline when compared to the $1.48 per share that Wells Fargo had earned in the year-ago quarter.

That’s not a terrible result by any means, but it shouldn’t justify the recent spike in WFC stock. Moreover, there’s another bottom-line statistic that you should pay attention to. Specifically, Wells Fargo reported net income of $5.114 billion in Q3 of 2024. Again, we see a fall-off here, as Wells Fargo had recorded a net income of $5.767 billion in the year-earlier period.

Wells Fargo‘s Declining Dollar Figures

Outside of these bottom-line figures, there are declining data points that Wells Fargo’s investors ought to take note of. For one thing, Wells Fargo’s net interest income (NII), an important measure of the company’s lending-business profits, decreased 11% year-over-year to $11.69 billion in 2024’s third quarter.

In addition, Wells Fargo’s Q3-2024 total revenue declined to $20.366 billion from $20.857 billion in the year-earlier quarter. Along with all of that, the company’s average loans fell from $943.2 billion in the year-ago period to $910.3 billion in this year’s third quarter.

These declining dollar amounts shouldn’t cause panic selling. At the same time, they shouldn’t inspire the magnitude of share-buying activity that we observed on Friday and Monday morning.

Is Wells Fargo Stock a Buy, According to Analysts?

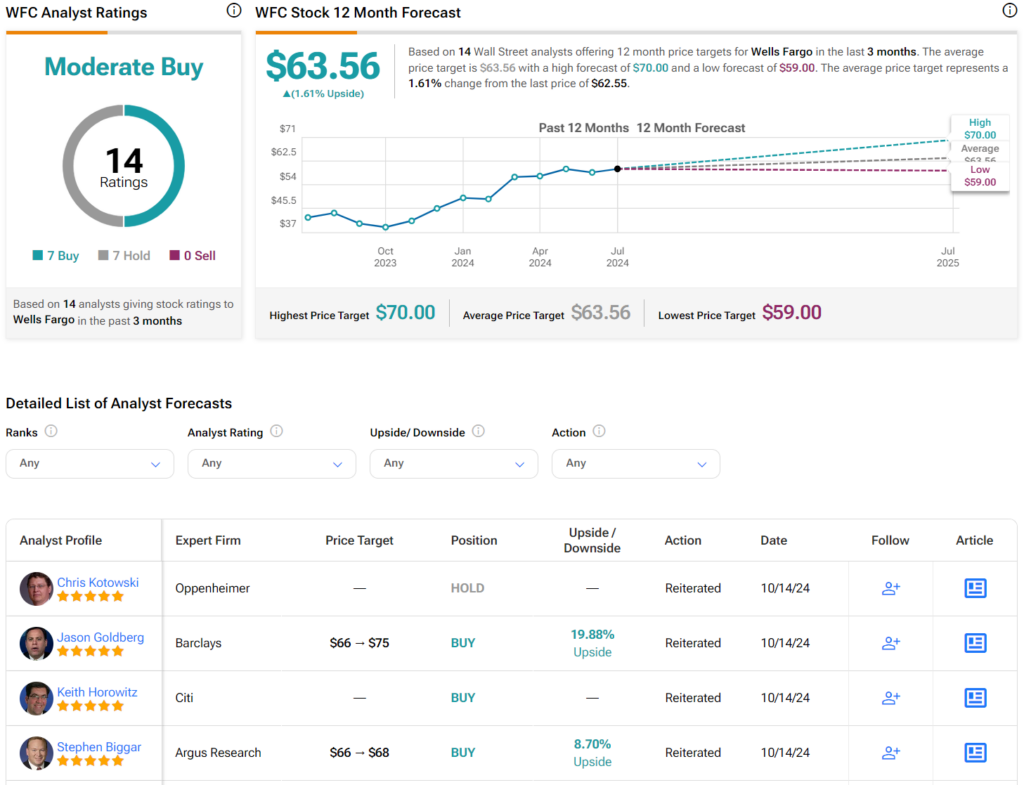

On TipRanks, WFC comes in as a Moderate Buy based on seven Buys and seven Holds assigned by analysts in the past three months. The average Wells Fargo stock price target is $63.56, implying 1.6% upside potential.

If you’re wondering which analyst you should follow if you want to buy and sell WFC stock, the most profitable analyst covering the stock (on a one-year timeframe) is Matt O’Connor of Deutsche Bank (DB), with an average return of 18.18% per rating and a 76% success rate.

Conclusion: Should You Consider Wells Fargo Stock?

Quite possibly, the market set a low bar for Wells Fargo’s Q3-2024 EPS and staged a relief rally when the company cleared that bar. However, beating low expectations doesn’t automatically mean that Wells Fargo is in terrific financial shape.

Multiple declining data points indicate that Wells Fargo can certainly improve in some areas. The market seems to have completely ignored these financial facts, so a near-term retracement in the Wells Fargo share price could be imminent. Consequently, I’m choosing to hang out on the sidelines, and I’m not making any hasty purchases of WFC stock today.