U.S. telecom giant Verizon (VZ) is a favorite among dividend stocks but has taken a hit following a mixed Q2 earnings report. The investment thesis for Verizon centers on its efforts to reduce leverage, boost free cash flows, and support its dividends, with only slight progress made in Q2. Despite slow progress and recent declines in investor confidence due to muted top-line growth, I still believe Verizon’s dividend remains attractive. I’m bullish on the stock, as Verizon continues to be a compelling defensive pick to own.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Verizon’s Q2 Earnings: Mixed Results and Tepid Response

In a nutshell, Verizon reported mixed Q2 earnings: a top-line miss, bottom-line results in line with the consensus, better-than-expected operating metrics, and unchanged P&L guidance. This combination ultimately disappointed investors, leading to a 6% drop in the stock price, though it has since experienced a brief recovery.

Earnings came in at $1.15 per share on an adjusted basis, but this meant another quarter of year-over-year declines in EPS (see below). In fact, Verizon hasn’t been able to grow its bottom line year-over-year since Q2 2022, facing various headwinds in the telecom industry. This is why the stock has significantly underperformed the S&P 500 (SPX) in recent years.

What really disappointed investors this time was the revenue. Verizon posted revenue of $32.80 billion, missing the market’s $33.05 billion estimate and showing only a modest 0.6% year-over-year increase.

The drop is largely due to a decrease in Wireless equipment revenues—smartphones, tablets, and routers—which fell from $5.3 billion in the same quarter last year to $5 billion. According to management, lower promotions and a 13% year-over-year decline in phone upgrades have taken a toll. However, Service revenue, which is crucial due to its higher margins and recurring nature, grew at 3.5%.

Another key point is that Verizon added 148,000 new post-paid phone customers and 391,000 new broadband customers this quarter. Finally, the Fixed Wireless Access (FWA) business segment is on track to reach $2 billion in annual revenue. Nonetheless, Verizon still isn’t seeing significant overall growth.

Net Debt, Cash Flow, and Dividends: What Really Matters

Verizon’s investment thesis heavily relies on its ability to reward shareholders through dividends. Therefore, investors closely monitor the company’s management of leverage and improvement in cash flows.

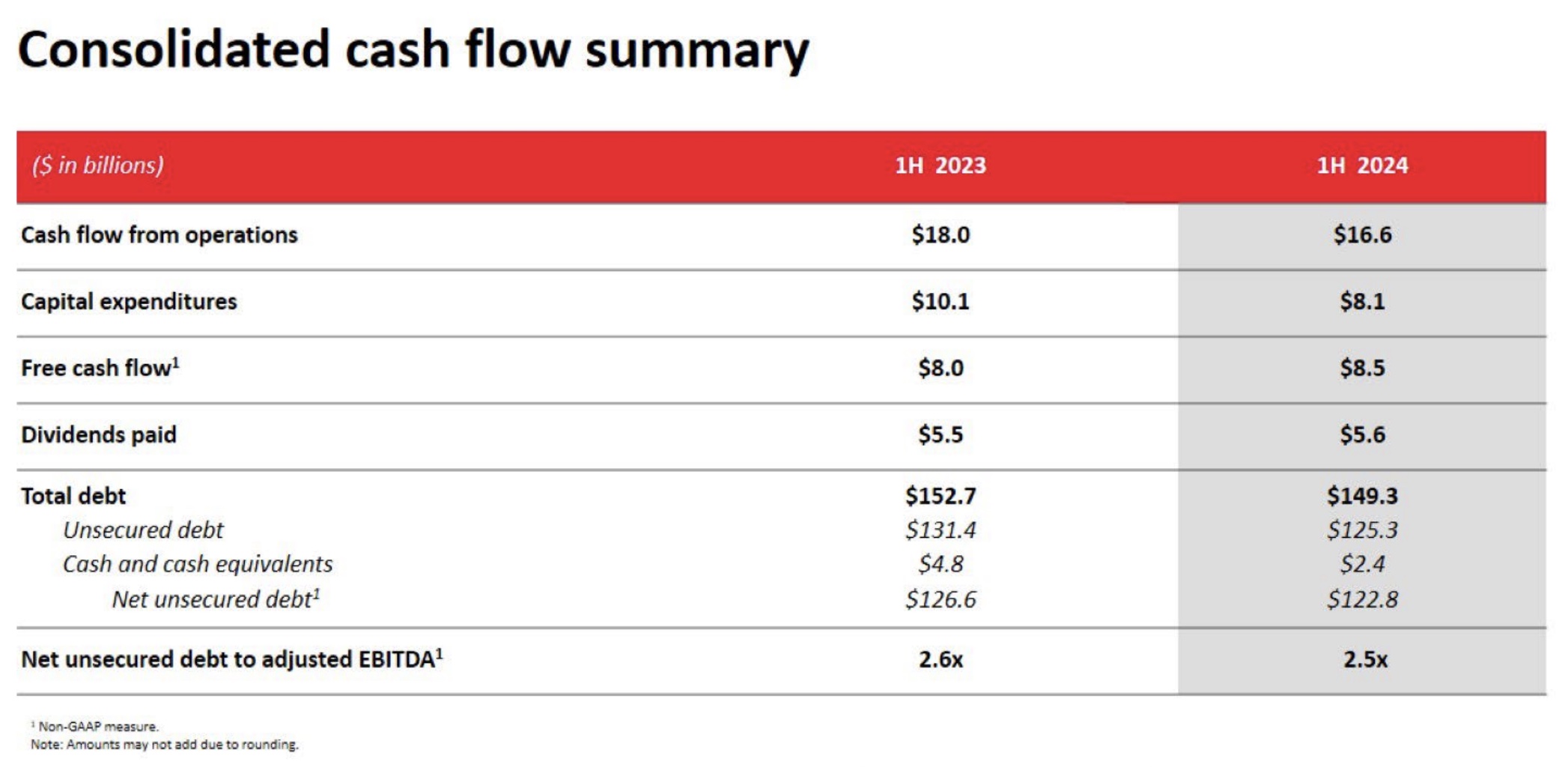

Verizon’s total debt stands at $149.3 billion, which has increased by 40% over the past five years due to its extensive 5G expansion. However, net unsecured debt fell to $122.8 billion in Q2, about $4 billion less than at the start of 2024. Leverage (net debt/EBITDA) also improved slightly to 2.5x, down from 2.6x at the beginning of the year. Despite these modest improvements, interest expenses jumped to $1.7 billion from under $1.3 billion the previous year, reflecting the adverse macroeconomic conditions.

Source: Verizon’s Investor Relations

Verizon’s full-year CapEx guidance remains at $17 billion to $17.5 billion, down from $18.7 billion in 2023 and $23.1 billion the year before. This reduction in CapEx should enhance free cash flow growth. In the first half of 2024, free cash flow rose by 7% year-over-year to $8.5 billion, ensuring a secure dividend payout for the rest of the year.

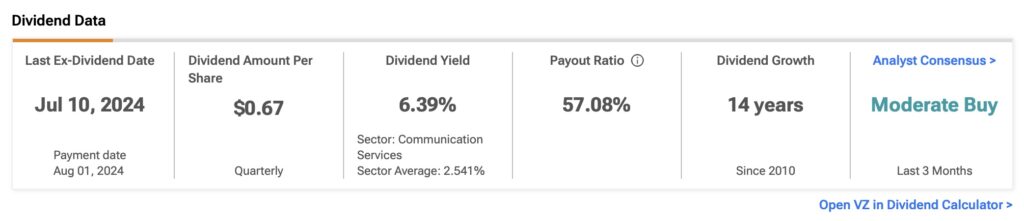

With a dividend yield of 6.4% and a payout ratio of 57%, Verizon’s dividend remains attractive, especially compared to the 4.28% yield on the U.S. 30-year Treasury. The free cash flow comfortably covers the dividend, and the expected modest CapEx requirements in the coming years are good news for income-oriented investors.

Why Owning Verizon Stock Still Makes Sense

It’s tough for many investors to get excited about a stock with forecasted revenue growth of just 0.9% in 2024 and 1.8% in 2025, especially when the bull market is driven by high-flying AI stocks. Defensive plays like Verizon can seem dull in comparison. This lack of excitement also leads to lower valuation multiples. Verizon trades at a forward P/E of 8.7x, about 10% below its historical average over the past five years.

Despite the post-Q2 dip, Verizon has seen a positive performance over the past 12 months, up more than 30%. This shows a shift towards better cash flow generation and debt reduction, bolstering the company’s ability to provide attractive yields for investors.

I believe investors should consider owning Verizon shares strategically. While its business growth might be slow, Verizon can still deliver positive long-term returns, especially through dividends.

Verizon’s low monthly beta of 0.4 over the past five years suggests its stock performance is less volatile and less correlated with the broader market. This low correlation can provide long-term stability, even if it’s not as attractive during a bull market.

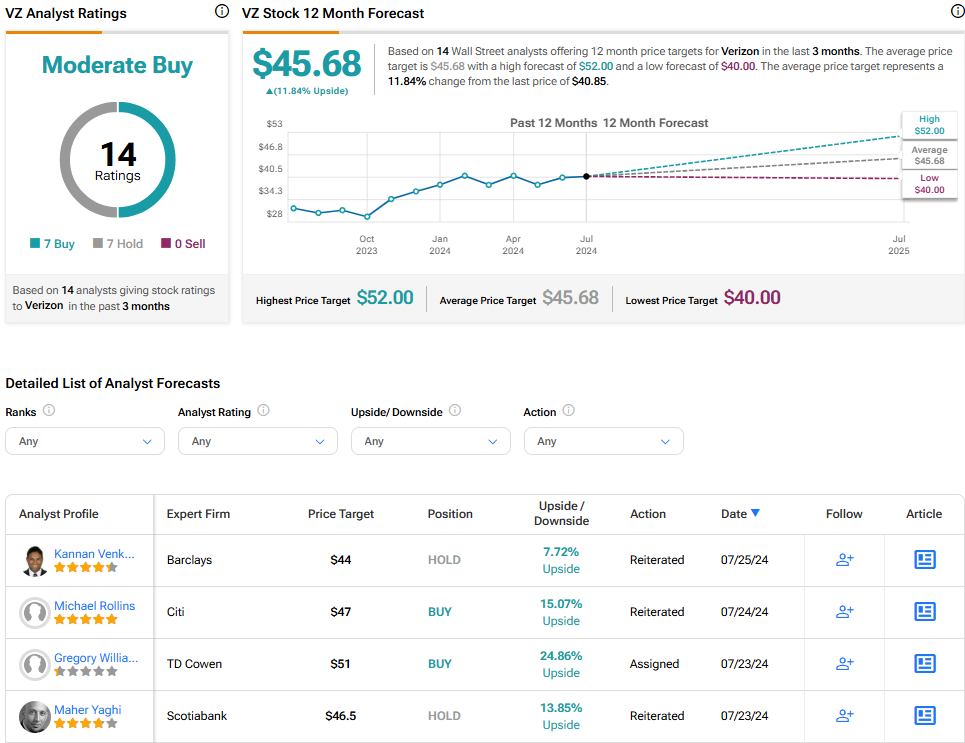

Is VZ Stock a Buy, According to Analysts?

Wall Street analysts are somewhat divided on Verizon stock. The consensus is a Moderate Buy, with seven analysts recommending a Buy and another seven suggesting a Hold. No events from Q2 prompted analysts to adjust their price targets for VZ. The average VZ stock price target is $45.68, indicating upside potential of 11.8% from the latest share price.

Key Takeaway

Arguably, the market is right to be frustrated with the company’s revenue miss and the slow pace of deleveraging and improving free cash flow. However, despite the slow progress, it still represents a step forward that helps ensure the stability of the dividend. The reduction in CapEx this year and possibly next is good news for dividend-seeking investors, especially when strong top- and bottom-line growth isn’t expected.

Additionally, I believe the market is overlooking Verizon’s defensive qualities post-Q2. Once investors recognize this, the stock is likely to rise again.