Qualcomm (QCOM) is an American multinational organization dealing in software, semiconductors, and services related to wireless technology. The company owns a number of patents for technology critical to WCDMA, TD-SCDMA, CDMA2000, 4G, and 5G mobile communications.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

As a semiconductor player focused on the smartphone market, Qualcomm has done well to partner with Apple (AAPL). The company’s growth rate has mirrored that of the American tech giant, with 5G smartphone adoption booming. Qualcomm’s hope is to blanket most cities with 5G devices and remain the dealer in this space.

However, recent concerns around the potential for Apple or others to further encroach on Qualcomm’s market remain.

I’m bullish on Qualcomm’s long-term prospects, though think near-term volatility is likely to remain a way of life in the markets. With this stock trading near its all-time high, perhaps that’s a dangerous view.

How Hard Will Apple Hit Qualcomm’s Core Business?

One of the key factors investors looking at Qualcomm’s business model are continuing to assess is the impact of Apple’s move to design and make its own chips. According to recent estimates, Qualcomm is expected to provide only 20% of the chips used in iPhones, down from what was a majority market share previously.

This is a steep dropoff, and one that certainly is a concern for some long-term investors. The long-term partnership between Apple and Qualcomm has been a big driver of this company’s success. However, judging from the recent stock price performance of Qualcomm, investors don’t seem too worried.

That’s because like Apple diversifying its supplier base, Qualcomm has done the same with its customers. Qualcomm chips are used by a wide range of mega-cap clients, meaning Apple’s business is something Qualcomm could theoretically let go of.

Additionally, Apple’s reliance on partnerships to build its products may entice iPhone manufacturers to request Qualcomm chips moving forward, something that would provide Qualcomm with a boost, should such a situation materialize.

Earnings and Fundamental Analysis

From a fundamentals perspective, there’s a lot to like about how Qualcomm is positioned right now. Despite trading near all-time highs, this stock is valued at roughly 20.5-times earnings. That’s extremely cheap when looking at other high-flying semiconductor players.

A significant portion of this lower valuation multiple can likely be ascribed to the aforementioned headwinds with this company. That said, Qualcomm’s earnings provide a solid base underneath this stock, the key driver most investors look at with Qualcomm.

The company’s recent earnings results highlighted the kind of growth long-term investors like to see. Qualcomm beat expectations on the top and bottom line, showing 30% growth on sales and nearly 50% growth on the company’s bottom line. This kind of performance is hard to find, even in today’s inflation-driven economy.

Branching Out to Accelerate Growth

Amid all the facts and speculation, Qualcomm recently branched out to boost its growth. As noted in a previous piece, Qualcomm and investment group SSW Partners announced the acquisition of an automotive technology firm, Veoneer.

There are many who have been bullish on this deal from the perspective of long-term growth. Veoneer provides a unique avenue for Qualcomm to grow its chip business in the IoT market, with Veoneer’s portfolio of connectivity and application solutions for automobiles and cellular devices worth considering.

Indeed, Qualcomm’s 35% year-over-year growth in its Handheld division signals the strength its recent partnerships and acquisitions have had on the company’s top and bottom line. There are many reasons why long-term investors like Qualcomm stock. However, clearly, the company’s ability to pivot and diversify its customer base are up there among the top of the list.

Wall Street’s Take

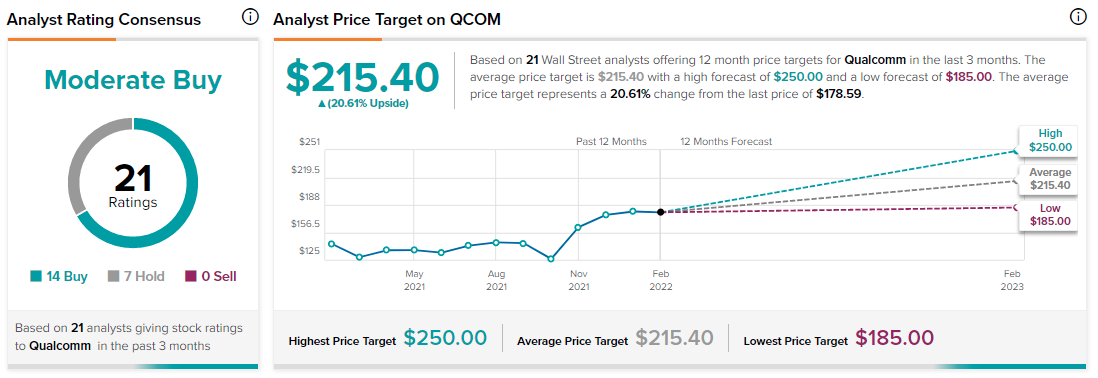

As per TipRanks’ analyst rating consensus, Qualcomm’s stock is a Moderate Buy. Out of 21 analyst ratings, there are 14 Buy recommendations and seven Hold recommendations.

The average Qualcomm price target is $215.40. Analyst price targets range from a high of $250 per share to a low of $185 per share.

Bottom Line

As a leading chip supplier, Qualcomm is certainly an intriguing stock to consider. Those who believe growth in the 5G sector is only likely to pick up may like the secular tailwinds behind this stock.

As the economy continues to open up, and we get more clarity on what the future outlook holds, Qualcomm is a stock that should stabilize into a longer-term growth pattern.

The company’s fundamentals are robust, and more than support Qualcomm’s existing valuation.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure