After a stock price decline of 17% so far this year, shares of NextEra Energy (NEE) are now trading at a significant discount from where they were at the end of 2021. However, that’s not enough to trigger a buying stance now, in my opinion.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

With the stock price coming down from the $80-$81 resistance level on its chart, NextEra Energy’s stock may still not be cheap despite its year-to-date loss.

NEE has major operations in Florida and is a profitable electric utility company with growth potential. However, since the goal of investing in stocks is to take advantage of this growth potential through share price appreciation, I would buy shares when they hit the low range of their recent trading range, around $68-$70 per share, to maximize gains. Therefore, I am bearish on the stock in the short term.

Besides operating in the electric utilities industry, NEE is also active in wind and solar power generation and battery storage, operating as a global leader.

The company produces zero-emission electricity from seven commercial nuclear power plants located across Florida, New Hampshire, and Wisconsin.

Why NEE Stock Can Fall Further

NEE’s stock price is affected by fluctuations in the price of electricity. Keeping that in mind, I forecast that the stock price could drop significantly sometime between late August and mid-October, also driven by continued strong headwinds in the market.

By late August, Florida’s hottest time of the year is over, and people will use less energy to cool down their homes/surroundings. The mix will lower the price of electricity per kilowatt hour (kWh) and can negatively affect NEE stock.

NextEra Energy’s 14-day Relative Strength Index (RSI) of 49 suggests that if the stock price wants to fall further, there is still plenty of room.

The indicator ranges from 30 to 70. A reading of 30 means a stock is oversold, while a reading of 70 means a stock is overbought.

Q1-2022 Results: Higher Earnings with Lower Sales

In the first quarter of 2022, NextEra Energy reported earnings per share (EPS) of $0.74, a 10.5% year-over-year increase, on total revenues of nearly $2.89 billion or nearly 23% less than last year. Q1-2022 EPS beat the average analyst estimate by $0.02.

NextEra Energy Reiterated its Solid Long-Term Guidance

Looking ahead to 2022, the company reiterated its EPS guidance of between $2.75 and $2.85 versus full-year 2021 EPS of $2.55. The average analyst estimate for this year is $2.86.

Furthermore, the company has the following EPS expectations until 2025:

- a 6.6% to 8.1% increase from 2022 to a range of $2.93 to $3.08 in 2023.

- a 6.8% to 8.1% increase from 2023 to a range of $3.13 to $3.33 in 2024.

- a 7% to 8.1% increase from 2024 to a range of $3.35 to $3.60 in 2025.

Meanwhile, analysts estimate that NextEra Energy will grow its EPS by 7.7% in 2023 and by about 8.7% per year in 2024 and 2025.

The company’s growth forecasts are based on a solar portfolio totaling 3,600 megawatts and a backlog of wind projects for commercial operations in 2022 and beyond. The company is also developing solar and battery storage projects.

NEE’s Balance Sheet is Weak but May Improve

NextEra Energy has a relatively weak balance sheet that must be strengthened if it wants to continue expanding its low-cost solar projects and its portfolio of renewable energy and storage projects.

However, if operations continue to perform as well as they did in the first quarter of 2022, then the company’s financial position is on track to improve.

As of March 30, 2022, total cash and equivalents totaled $1.5 billion, nearly 40 times smaller than its total debt of $59.7 billion, raising concerns about the company’s overall financial health.

The interest coverage ratio, which determines how easily a company can pay interest charges on the total outstanding debt, stands at about 1x for NextEra Energy.

Since the ideal value should be 1.5 or higher for a company to be deemed able to bear its financial burden, NextEra Energy may experience difficulties in meeting its financial obligations.

NextEra Energy’s interest coverage ratio is calculated by dividing its TTM operating income of $1.56 billion by the TTM interest expense of $1.55 billion.

Additionally, NextEra Energy has a debt-to-EBITDA ratio of 9.9 as of March 2022, calculated as the total debt of $59.7 billion divided by EBITDA of $6.03 billion, meaning that its current debt is about 10x higher than its annual earnings before interest, taxes, depreciation, and amortization.

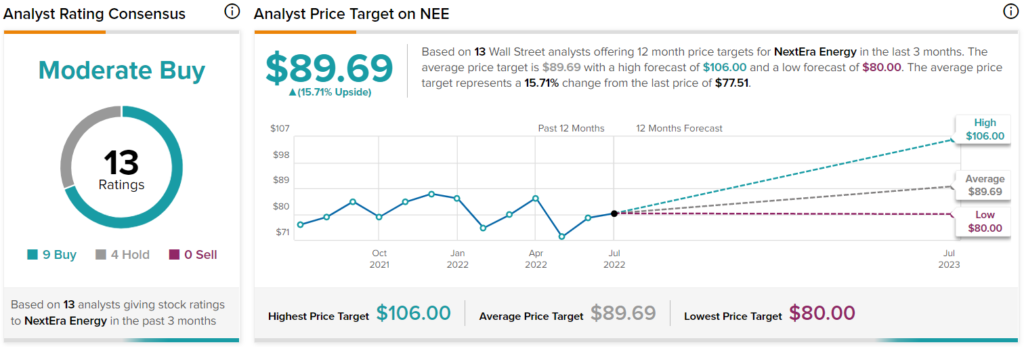

Wall Street’s Take on NEE Stock

In the past three months, 14 Wall Street analysts have issued a 12-month price target for NEE stock. NextEra Energy has a Moderate Buy consensus rating based on nine Buys, four Holds, and zero Sell ratings.

The average NEE price target is $89.69, implying 15.7% upside potential.

The Valuation Isn’t Cheap

Shares are changing hands at $77.51 as of the writing of this article for a market cap of $152.2 billion and a price/earnings ratio of 104.6x. Also, its price/book ratio is 4.2x, and its price/sales ratio is 9.4x.

Next, the stock trades above its 50-day moving average of $75.42 and slightly below its 200-day moving average of $80.88. Therefore, the stock doesn’t seem cheap.

NEE’s enterprise-value-to-EBITDA ratio stands at 33.9x, while its enterprise-value-to-revenue ratio yields 12.6x. These two financial indicators lead to an EBITDA margin of 37.1%, which is above the sector median of 33%, indicating that NextEra Energy’s business is more profitable than most of its competitors.

The company has good growth prospects, but it is likely better to delay buying shares until they’re trading much lower than current levels to make the most of the upside potential. I expect the company to trade lower sometime from late August to mid-October.

Also, the stock price is likely to offer a more attractive dividend yield than the current 2.06%, which is only 44 basis points above the S&P 500’s (SPX) 1.62% yield. Nonetheless, the company has paid out dividends for 32 consecutive years and has increased them for 27 straight years.

Conclusion – NEE Runs Efficiently, but a Better Entry Point May Come

NextEra Energy has good growth potential, but this is probably a Buy to put off until after the summer season, as the stock price is likely to become more affordable than it is today.