Etsy (NASDAQ:ETSY) used to reliably deliver 30% year-over-year revenue growth and healthy profit margins. Investors can look back to its Q2-2019 earnings report for proof. Then, the pandemic brought the stock to new heights. Revenue more than doubled in some quarters, and earnings growth was even higher. Despite its pre-pandemic status as a growth stock and the lockdown-induced surge now over, shares are not undervalued, in my view, and I’ll explain why. I’m bearish on ETSY stock.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Why Some Bulls Believe Etsy Is Undervalued

Most of the argument about Etsy being an undervalued stock is that the share price has fallen off a cliff. Shares are down by roughly 76% from their all-time highs. The company’s P/E ratio has been knocked down to 30, and the forward P/E ratio looks even more enticing, as it currently sits at 20.

Etsy’s growth isn’t what it used to be, but it’s still growing. Investors may feel optimistic about the stock’s 7% revenue growth rate in Q3 2023 and its 13.8% net profit margin. Revenue growth is a far cry from 2020 and even 2019, but it’s something.

Bullish investors may be eyeing Etsy’s all-time high and fantasizing about the returns they could generate if the stock reclaimed that price level. Not all stocks reclaim their all-time highs, though.

Unraveling the Bullish Thesis

The beatdown on ETSY stock has been constant since it peaked in November 2021. The stock has lost roughly half of its value over the past year and is down ~8% year-to-date. While a 20-forward P/E ratio looks good, a 6.6 five-year forward PEG ratio offers a better picture of the stock’s grim prospects.

While the P/E ratio only considers a stock’s price and earnings, the PEG ratio also factors in growth. A low growth rate results in an elevated PEG ratio. Investors who use this ratio believe a stock is undervalued if its PEG ratio is below 1.00. Regarding the PEG ratio, ETSY stock is in another stratosphere.

Etsy will continue to fall unless it fixes one number in its financials — gross merchandise sales. Revenue and net income growth do not matter if gross merchandise sales (GMS) remain flat.

This metric represents Etsy’s ceiling. It’s the total buyer activity on the site, and Etsy makes a percentage of each sale. Below are two quick examples of the correlation between GMS and revenue growth:

Q2 2019:

- GMS growth: 21.4%

- Revenue growth: 36.8%

Q3 2020:

- GMS growth: 119.4%

- Revenue growth: 128.1%

The common theme is that revenue growth is a bit higher than GMS growth. Revenue growth is higher because Etsy can squeeze more out of the lemon through opportunities like higher fees and advertising.

Etsy’s GMS growth came in at 1.2% year-over-year and was flat on a currency-neutral basis. The business will stop growing if GMS stays flat, and there’s only so much Etsy can squeeze out of the lemon before buyers and sellers explore other choices to save money.

Further, the company’s big acquisition of Elo7 did not bear fruit (Etsy ended up selling Elo7), and leadership is citing challenging macroeconomic conditions to justify a sudden slowdown in GMS growth. However, I’m not convinced that macroeconomic conditions are a key factor. Many e-commerce corporations reported better financials, and the advertising industry has rebounded.

Comparing Etsy with Other Stocks

Etsy also mentioned declining discretionary spending as a key issue that has halted GMS growth. However, Target (NYSE:TGT) has experienced the same issue with discretionary spending, and yet, it trades at an 18 P/E ratio, 15.5 forward P/E ratio, and a 1.07 PEG ratio.

Investors may also want to consider how Etsy compares with eBay (NASDAQ:EBAY). eBay followed a similar boom and bust cycle, but both parts of the cycle were less dramatic. eBay’s revenue growth has come to a mid-single-digit crawl, but at least that stock trades at an 8 P/E ratio and a 9.5 forward P/E ratio.

Etsy’s valuation does not make sense when compared to Target and eBay, and these feel like appropriate comparisons, given Etsy’s meaningful revenue deceleration. Investors must be praying that an activist campaign can right the ship.

Is ETSY Stock a Buy, According to Analysts?

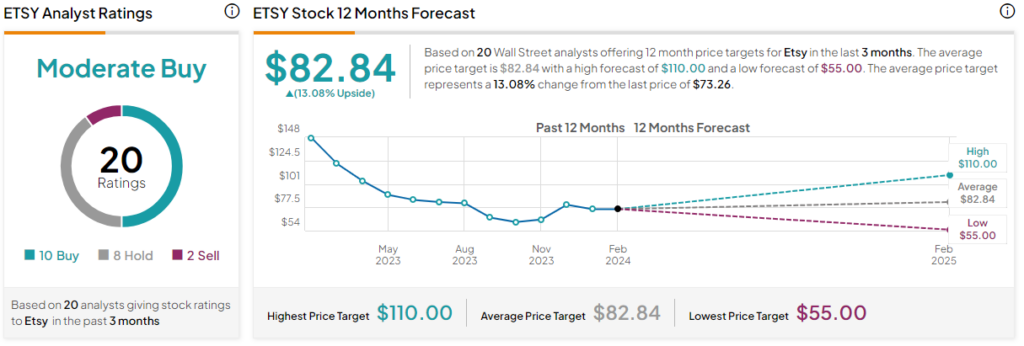

Analysts are more generous than me. On TipRanks, ETSY stock comes in as a Moderate Buy based on 10 Buys, eight Holds, and two Sells assigned in the past three months. Moreover, the average ETSY stock price target implies 13.1% upside potential. The lowest price target is $55, which seems like a more accurate indicator of where the stock is heading, in my opinion.

The Bottom Line on ETSY Stock

Revenue and earnings growth are not the company’s key indicators. It’s GMS growth or bust. If Etsy cannot nudge this number higher, it’s very limited in how it can generate meaningful revenue and earnings growth. If GMS growth rebounds, the rest will follow.

A stock well off its all-time high isn’t necessarily undervalued. While investors may think about pre-pandemic and pandemic growth rates, those days appear to be long gone. Investors have to look at the present situation rather than lean on past results.