This year we saw declines pretty much across the board, with the S&P 500 tumbling ~20%. But last week was the index’s best week since June – the S&P had a weekly gain of about 4.7%. We’ve seen several of these bounces this year, and the question is, are they bullish indicators or merely ‘dead cats’?

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

According to Oppenheimer’s chief investment strategist John Stoltzfus, it shouldn’t really make a difference whether we’re looking at bullish indicators or bear market rallies. The key here is simply taking advantage of a bargain price. That current low prices give investors a chance to ‘love assets when they’re looking their least attractive in some time.’

Stoltzfus goes on to explain today’s opportunities in greater detail: “We often say that there’s no ‘all clear’ signal that sounds when it’s a good time to buy stocks, but for long-term investors and those with cash to put to work, the broad market at these levels offers opportunity, in our view. We can’t say that the market has bottomed at these levels, nor that the bear market might not grind on for some time to come, but with so much bad news already priced in, the potential rewards of investing at these levels are looking more attractive relative to the risks.”

The stock analysts at Oppenheimer are following Stoltzfus’s lead, and picking out stocks that are primed for gains despite the confusing market environment. After running two of these stocks through TipRanks’ database, we found out that the rest of the Street is also on board, as each boasts a “Strong Buy” consensus rating.

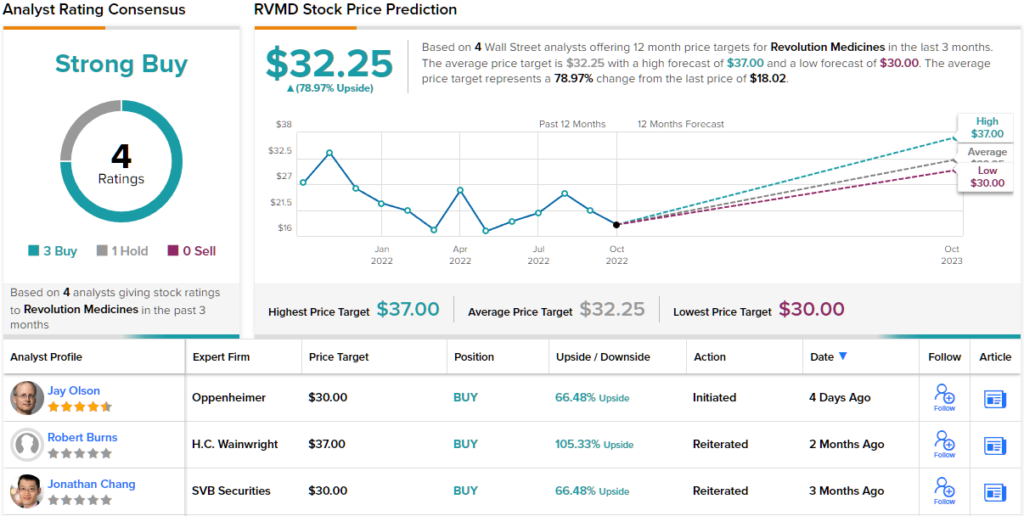

Revolution Medicines, Inc. (RVMD)

We’ll start with Revolution Medicines, a clinical-stage biopharmaceutical company in the precision oncology niche. The company is working on a novel research approach to the treatment of cancer, specifically focusing on drug candidates designed to inhibit RAS-addicted malignancies. The company has an active research pipeline featuring several clinical stage and pre-clinical drug candidates, in two groups, RAS(ON) inhibitors and RAS companion inhibitors.

In the second group, the company’s lead drug candidate, RMC-4630, is under development in conjunction with pharma giant Sanofi. The company reports regular quarterly revenue due to collaboration payments from Sanofi. In the most recent quarterly report, for 2Q22, the company had $9.1 million in such revenues.

Valuable collaborations and solid cash position provide Revolution Medicines with a sound foundation for its research programs, which are proceeding apace. In September of this year, the company announced that it had dosed the first patients in its Phase 1/1b study of RMC-6291, the first mutant selective RAS(ON) inhibitor to reach this stage of testing. RMC-6291 showed a best-in-class pre-clinical profile, and targets cancers that harbor the KRASG12C mutation.

Also at Phase 1/1b is RMC-6236, an orally dosed drug designed to combat cancers with a variety of RAS mutations. The current study is looking at -6236 as a monotherapy and expects to have clinical trial results next year.

The most advanced drug candidate, RMC-4630, is currently undergoing several concurrent clinical trials. The RAS companion inhibitor is being tested as a combination therapy, in conjunction with sotorasib, in a Phase 2 trial overseen by Revolution Medicines. This trial is expected to release results next year. The other two clinical trials of this drug candidate, a Phase 1 and a Phase 1/2, are both being overseen by Sanofi. The first is in conjunction with Keytruda, and the second with adagrasib.

Oppenheimer analyst Jay Olson has initiated coverage of Revolution Medicines, and in his view the company will benefit as its approach meets a ‘high unmet medical need.’

“We view RVMD as a pioneering oncology company developing novel therapies targeting RAS-mutated cancers with potentially best-in-class KRASG12C (ON) inhibitor candidate RMC-6291 and later-stage RMC-4630 targets SHP2 for combination approaches. KRAS-G12D (ON) and pan-KRAS (ON) inhibitors RMC-9805 and RMC-6236, respectively, have first-in-class potential…. We forecast $2.7B of risk-adjusted peak sales for RVMD, and our SOTP analysis ascribes the majority of valuation potential to the KRAS(ON) portfolio,” Olson opined.

Looking forward, Olson gives RVMD shares an Outperform (i.e. Buy) rating, and his price target of $30 implies a one-year upside potential of 66%. (To watch Olson’s track record, click here)

Overall, the 4 most recent analyst reviews of Revolution Medicines include 3 Buys against 1 Hold, for a Strong Buy consensus rating. The shares are selling for $18.17 and their $32.25 average price target suggests an upside of ~79% in the next 12 months. (See RVMD stock forecast on TipRanks)

Tractor Supply Company (TSCO)

Let’s shift gears now, and look at Tractor Supply, a well-known retailer specializing in home, lawn, and garden supplies; livestock and pet supplies for everyone from professional and amateur ranchers and ordinary pet owners; tools and hardware; outdoor apparel and footwear, and hunting gear. The company styles itself as a rural lifestyle retailer, and operates over 2,000 stores in 49 states.

Tractor Supply is a leader in a profitable niche, and the company’s quarterly revenues show the story graphically. It typically posts the highest revenues and earnings in Q2 of a year; this is a well-established pattern for Tractor Supply, based on seasonal shopping in the spring when customers restock on outdoor gear, home improvement supplies, and farm equipment. Overlaid on that pattern is a second trend of consistent year-over-year revenue and earnings gains.

In the latest quarterly report, for 3Q22, the company posted EPS of $2.10 per share, beating the $2.08 forecast and growing 7.7% year-over-year. At the top line, the reported revenue of $3.27 billion was up 8.2% from the year-ago quarter. The company saw its comp store sales grow 5.4% y/y, and returned a total of $225.5 million to shareholders through its share repurchase program and its quarterly dividend.

Brian Nagel, 5-star analyst with Oppenheimer, describes Tractor Supply’s ‘underlying trends’ as ‘decidedly solid,’ and goes on to elaborate on the details: “We look upon continued solid sales and earnings trends at TSCO lately as reflective of the company’s utilizing a now even better-positioned business model to capitalize upon underlying spending strength amongst core consumers and of the ongoing competitive fallout within the broader feed and pet categories. We continue to recommend TSCO as a compelling hedge play within discretionary retail, amid ongoing macro challenges and market concerns of a forthcoming, more severe economic downturn.”

This outlook gains an Outperform (i.e. Buy) rating from Nagel, whose $270 price target indicates room for ~31% share growth in the year ahead. (To watch Nagel’s track record, click here)

All in all, this strongly-positioned niche retailer has picked up 16 recent analyst reviews, and these break down to 12 Buys and 4 Holds for a Strong Buy consensus rating. The average price target of $230 implies ~11% upside potential for the stock on the one-year time frame. (See TSCO stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.