Semiconductor stocks have been dragged lower amid the broader market sell-off. In this piece, we used TipRanks’ Comparison Tool to look closely at three discounted semiconductor stocks — AVGO, NVDA, and AAPL — that Wall Street still believes in despite recent negativity.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Semiconductor shortages have been a major cause of concern for most of the pandemic. Such shortages worked their way through most parts of the economy, affecting everything from cars to next-generation video-game consoles.

After the semi shortage could be a glut, as supply gets back up to full speed (or higher than full speed) and demand looks to fade in the early innings of a recession. However, such a semiconductor glut could lead to markdowns and margin erosion in some of the top semiconductor stocks that have been weighed down by seemingly endless headwinds in recent years.

In any case, 2020 and 2021 showed us just how vital the semis are to a proper-functioning world economy. If firms can’t get their chips, the supply of many consumer goods falls, adding fuel to price increases.

As the semi boom (and shortage) turns into a bust (and glut), there’s no telling how much lower the “chip dip” will go on for. Numerous semiconductor makers see weakness. Indeed, economic recessions tend to be quite unforgiving to the cyclical semi plays.

Looking further out, many secular trends in the tech world are still in play. These trends will outlast the coming recession and associated chip bust. From a longer-term perspective, the chip dip seems more than worth buying. Many Wall Street analysts agree.

Broadcom (NASDAQ: AVGO)

Broadcom is a $202 billion semiconductor behemoth engaged in designing and manufacturing various semiconductor components. The company has been pushing into high-margin software in recent years, thanks in part to strategic acquisitions. Recently, Broadcom bought virtualization software firm VMWare in a deal worth $61 billion.

Many analysts viewed the acquisition favorably, given the modest multiple paid (VMWare stock lost around 53% of its value before Broadcom stepped in). Further, Broadcom has had great success in integrating past software deals, including CA Technologies.

Unlike many tech companies with the urge to merge, Broadcom has been very disciplined in its approach, opting to wait for valuations to come down to reasonable levels before pulling the trigger.

With a growing software presence, Broadcom can become far less cyclical than the semiconductor market. The semiconductor market can be quite cyclical, but software can help hold up the fort. Further, Broadcom’s propensity to buy on dips minimizes risks relative to other tech heavyweights that may have been found guilty of chasing.

Recently, Broadcom clocked in a solid third quarter, with per-share earnings of $9.73, above the consensus estimate of $9.56. Revenue also rose 25% year over year to $8.5 billion. Helping fuel the bottom-line beat was strength in Cloud and Data Centers. Though semis face a tough road ahead, Broadcom remains confident for its coming fourth quarter.

At 25.1x trailing earnings, Broadcom stock trades at a slight discount to its peer group. With less-cyclical software offerings to steady the ship, I think AVGO ought to be worth more of a premium in the face of a downturn.

What is AVGO Stock’s Price Target?

Wall Street can’t get enough of Broadcom, with a “Strong Buy” rating and 12 unanimous Buy ratings. The implied year-ahead upside is also quite high, at 33.3%, with the average Broadcom price forecast coming in at $676.36 per share.

Nvidia (NASDAQ: NVDA)

Nvidia is a graphics-processing unit (GPU) kingpin that’s grown to become one of the most exciting semiconductor plays in the tech scene today. Nvidia’s total addressable market (TAM) is huge, and it’s growing, with a foot in the door of various nascent tech markets, including AI, connected cars, video gaming, and the metaverse.

Though Nvidia is leaving its rivals behind with every product iteration, the stock has become incredibly frothy in recent years. As semiconductor demand goes from boom to bust, Nvidia stock could see its lofty valuation multiple contract further. Despite shedding more than 59% of its value from its peak, Nvidia stock is still up significantly from its pre-pandemic high.

It’s not just a slowing market or a recession that could hit Nvidia stock; new rules surrounding exports of leading AI GPUs to China and Russia could weigh on demand. Nvidia stock got pummelled, as government-mandated export limits will surely take a bite out of sales.

Despite the macro challenges, Nvidia continues to be one of the most innovative forces in Silicon Valley. In due time, its abilities will shine through again. In the meantime, the hefty 12.7x sales multiple, the recent quarterly flop (Q2 2023), and recession woes could be an overhang on the former high-flyer.

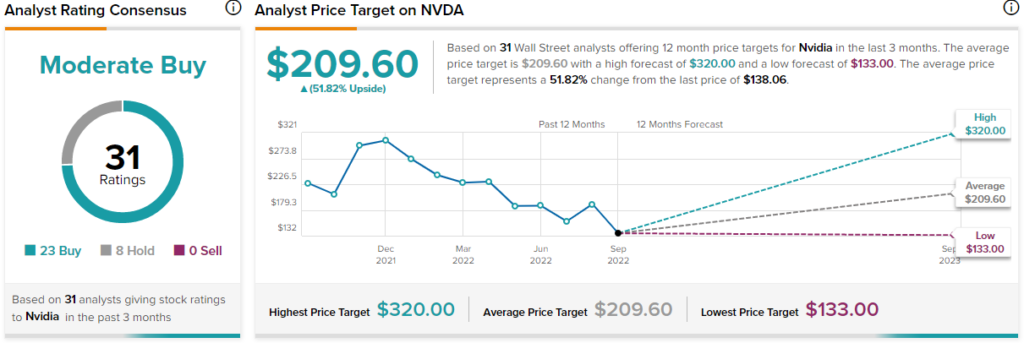

What is NVDA Stock’s Price Target?

Wall Street thinks the dip in NVDA stock is worth buying, with 23 Buys and eight Holds assigned in the past three months. The average NVDA stock price target of $209.60 suggests 51.8% upside potential over the coming year.

Apple (NASDAQ: AAPL)

Apple may not be a semiconductor pure-play, but it’s made quite a splash in chips over the past few years with its M-series Silicon. Further, Apple is reportedly looking to in-house many other semiconductor components used in its iPhones. According to Bloomberg, one of Apple’s new offices may look to create wireless radios and semiconductors used for Bluetooth and Wi-Fi connectivity.

Cutting firms like Broadcom out of the equation could do wonders for Apple’s margins while giving it more control during times when they are significant constraints on the global semiconductor market. Indeed, semi shortages have weighed on Apple’s past quarters. As the company looks to lower its dependence on other chip makers, Apple may be the hardware maker its rivals strive to be.

At the end of the day, Apple is all about finding the perfect balance of hardware, software, and services. The company has done a fantastic job of turning the M-series chip into something special. The product is leaving competing chips for dead. As Apple looks to become the maker of its own components, I’d look for similar performance and power-efficiency improvements across the board.

What is AAPL Stock’s Price Target?

Wall Street loves Apple, with 22 Buys, four Holds, and just one Sell. The average AAPL stock price target of $183.12 implies 17.1% year-ahead upside potential.

Conclusion: Analysts are Most Bullish on NVDA Stock

Broadcom, Nvidia, and Apple are chip makers that Wall Street continues to pound the table on. Of the three names on the list, analysts expect the most from Nvidia.