Although one of the biggest brands in the big-box retail industry, Target (NYSE:TGT) could be in for a rough second half. With management admitting that organized retail crime – specifically shoplifting – has negatively impacted its business, the news may represent a harbinger. I am regrettably bearish on TGT stock because of the harsh realities it faces.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Target Sounds the Warning

On May 17, Target announced its financial results for the first quarter of Fiscal Year 2023, which management characterized as a framework of “continued traffic and sales growth in an increasingly challenging environment.”

Regarding profitability, the big-box retailer reported Q1 GAAP earnings per share of $2.05, down 4.8% against the year-ago quarter’s EPS of $2.16. Adjusted EPS of $2.05 fell 6.2% compared to last year’s tally of $2.19. On the other hand, total revenue of $25.3 billion represented a lift of 0.6% compared with Q1-2022’s result.

However, the news item that captured everyone’s attention was the profitability guidance. Target Chair and CEO Brian Cornell stated in part that “As we look ahead, we now expect shrink will reduce this year’s profitability by more than $500 million compared with last year. While there are many potential sources of inventory shrink, theft and organized retail crime are increasingly important drivers of the issue.”

Further, the head executive declared, “We are making significant investments in strategies to prevent this from happening in our stores and protect our guests and our team. We’re also focused on managing the financial impact on our business so we can continue to keep our stores open, knowing they create local jobs and offer convenient access to essentials.”

TGT Faces Potentially Perilous Roads Ahead

The fact that retail crime catalyzed a half-billion-dollar reduction in expected profitability is already bad enough. However, such incidents at scale don’t just neatly and exclusively affect the inventory count, like a controlled demolition. Rather, they can create aftershocks that erode consumer confidence and employee trust. Thus, TGT stock faces a more difficult path than perhaps many investors realize.

For one thing, the retail crime issue isn’t just a 2023 problem. Last year, TipRanks reporter Sheryl Sheth mentioned that supermarkets, grocers, and restaurants suffer the brunt of rising crimes in this country. As a result, some companies made the painful decision of reducing their physical footprint in certain problematic locales.

Naturally, such downsizing impacts affected local economies, which eventually may trigger even more retail crimes out of desperation. Besides, even among workers that continue to enjoy employment, that status is not guaranteed to last as they face an increasingly unruly public.

Further, customers themselves may no longer wish to patronize retailers like Target due to underlying social volatility. “Cities including Seattle, Los Angeles, Chicago, and New York are facing the most surge in shootings and hate crimes driven by the pandemic-triggered stress, easy availability of weapons, and increased usage of alcohol and drugs,” wrote Sheth.

More worryingly, PBS stated in April of this year that mass shootings in the U.S. are “on a record pace.” If circumstances worsen, more folks may decide that going to brick-and-mortar stores just isn’t worth it. Under this framework, Target could lose business to e-commerce competitors like Amazon (NASDAQ:AMZN). Obviously, that wouldn’t be ideal for TGT stock.

No Solution on the Horizon

Under ordinary circumstances, the solution for organized crime of any nature is to expand the presence of police officers. However, that will likely prove tricky in the post-pandemic environment. Essentially, no immediately viable solution appears on the horizon for TGT stock.

The reason for pessimism centers on the push for historical awareness and social equity. While representing meaningful initiatives, many social justice advocates, unfortunately, leveled heavy criticism on the police. As a result, The Wall Street Journal reports that fewer people seek careers in law enforcement. Unfortunately, then, security falls increasingly on individual and corporate entities’ zone of responsibility, adding enormous pressure on embattled businesses.

Moreover, given the current political climate, companies like Target must be careful in how to address the crimes. Based on various sociological research, it’s too easy for companies to be perceived as being part of the problem rather than part of the solution if their security protocols disproportionately focus on disenfranchised communities.

Is TGT Stock a Buy, According to Analysts?

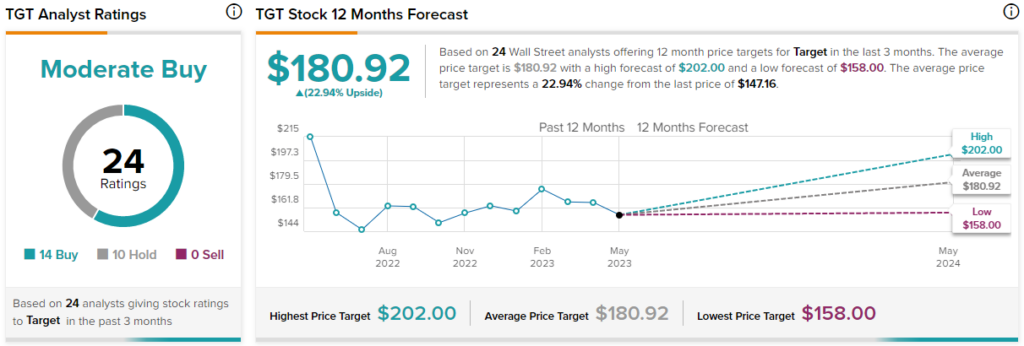

Turning to Wall Street, TGT stock has a Moderate Buy consensus rating based on 14 Buys, 10 Holds, and zero Sell ratings. The average TGT stock price target is $180.92, implying 22.9% upside potential.

Takeaway: TGT Stock is Stuck in an Ugly Situation

To clarify, Target is a victim of circumstances. It’s not management’s fault that so much of society has apparently lost its marbles. At the same time, just because Target carries no fault in the matter doesn’t mean TGT stock is attractive. Sadly, it may face more struggles before potentially bouncing back eventually.