Inflation started taking off last year and is now near 40-year highs. Last week, the world’s major central banks took a pivot toward an anti-inflationary policy stance, bumping up interest rates in a move that was expected but also a cause for concern. While the prospect of central bank action to tame inflation is a net positive, the required interest rate bumps could also push the economy into recession.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

In the meantime, investors are busy waiting. Waiting for the next Fed move, and waiting for the next data release, and waiting to see what will happen in the coming months. According to Sameer Samana, senior global market strategist at Wells Fargo, “If we’ve seen the worst of the rate of change from long-term interest rates, it may create room for equities to do a little bit better.”

Taking this into consideration, our attention turned to two stocks that Wells Fargo thinks have solid growth prospects, with the firm’s analysts forecasting at least 50% upside potential for each. Using TipRanks’ database, we found out both tickers also sport a “Strong Buy” consensus rating from the rest of the Street. Let’s take a closer look.

Match Group (MTCH)

The first Wells Fargo pick is a Texas-based company in the online dating field, Match Group. This tech firm owns and operates an active portfolio of online dating and matching services, including leading names like Tinder, Match.com, and OKCupid. Match Group boasts an enormous reach, from the online world to the real world, with apps that have been downloaded over 750 million times – and with 40% of all interpersonal relationships in the US starting online, Match Group’s total addressable market is substantial.

While Match Group has had a long run of success, the company is now coping with coming changes. Earlier this month, the company announce that long-time CEO Shar Dubey is resigning after 16 years of service. Dubey will be succeeded by Bernard Kim, who comes to Match Group from the social gaming firm Zynga.

Match Group controls the highest grossing, most downloaded dating app in the world, Tinder, and that is reflected in the company’s top line. At $799 million, the top line was up 20% year-over-year for 1Q22, a quarter which the company admitted was impacted by both COVID and the Russia-Ukraine war. The company saw an overall increase of 13% in total payers, to 16.3 million, a gain that was driven by the 34% increase in the Asia Pacific region. The company finished Q1 with a strong balance sheet, holding $921 million in cash and liquid assets.

Despite Tinder’s widespread use and success, the company’s stock is down 45% this year. However, 5-star analyst Brian Fitzgerald, of Wells Fargo, is not overly worried, and paints an upbeat picture of Match Group’s prospects in the long term.

“MTCH for the first time disclosed companywide MAU, pushing back on recent bear thesis (fueled by third-party app data of questionable accuracy) on declining user engagement. While we expect crosswinds to continue (likely for multiple quarters), we view fundamental opportunity as very much intact and valuation as compelling at current levels,” Fitzgerald opined.

What this adds up to for Fitzgerald is a stock that deserves an Overweight (i.e. Buy) rating. The Wells Fargo analyst also sets a price target of $115, suggesting an upside of ~58% going forward. (To watch Fitzgerald’s track record, click here)

Tech firms of Match Group’s size don’t lack for Wall Street attention, and MTCH shares have 17 analyst reviews on record. These include 15 Buys and 2 Holds, for a Strong Buy consensus rating. The $119.59 average price target implies ~64% one-year upside from the current trading price of $73.07. (See MTCH stock forecast on TipRanks)

MaxLinear, Inc. (MXL)

Now we’ll shift our attention to a semiconductor chip company, a resident of the niche that quite literally makes the digital world go ‘round. MaxLinear is a designer and distributor of integrated radio-frequency analog and mixed-signal semiconductors, chips used in applications from automotive and industrial connectivity to wireless access and ethernet switches to router and extender hardware. MaxLinear’s products have also found wide use in the continuing rollout of 5G infrastructure systems.

That alone would give this company a solid position in the chip world – but MaxLinear recently took a step to firm up that position. On May 5, the company announced that it will be acquiring fellow chip firm Silicon Motion. The combination of the two firms will create an entity with a combined revenue exceeding $2 billion, a total addressable market worth $15 billion, and instant entry into the ranks of the ten largest fabless chip suppliers. The transaction is expected to close in 1H23, and will value Silicon Motion at $3.8 billion, to be paid in both cash and stock.

Shortly before making the merger announcement, MaxLinear announced financial results for 1Q22. At the top line, quarterly revenue hit a record level of $263.9 million, up 26% year-over-year. On earnings, the company’s non-GAAP EPS jumped from 55 cents in the year-ago quarter to $1 in this latest report. And, the company finished the quarter with a net cash flow of $132.2 million, up leaps and bounds from the $40 million in 1Q21 and the $16 million 4Q21. MaxLinear guided toward $275 million to $285 million in revenue for 2Q22, a sequential gain of 6% at the midpoint. That guidance, of course, came before the Silicon Motion acquisition announcement.

Looking at the Silicon Motion deal, Wells Fargo’s 5-star analyst Gary Mobley writes: “While initial investor reaction has been negative, we view this deal as a long term opportunity for MXL. While investors don’t always react favorably to financially engineering EPS accretion (e.g., resulting EPS accretion doesn’t always get market valuation multiples), we view this MXL+SIMO transaction as one that enhances shareholder value.”

Unfortunately for investors, MaxLinear stock has been falling, and is down 46% year-to-date. However, Mobley remains upbeat regarding the company’s prospects, writing: “We are more bullish on the MXL story as shares have traded off to a point at which we have to say shares are grossly undervalued… We also like the fact that MXL’s rev has little direct correlation w/ direct consumer spending & is more tied to telco, cable MSO & data center cap ex, more durable areas in the current macro backdrop.”

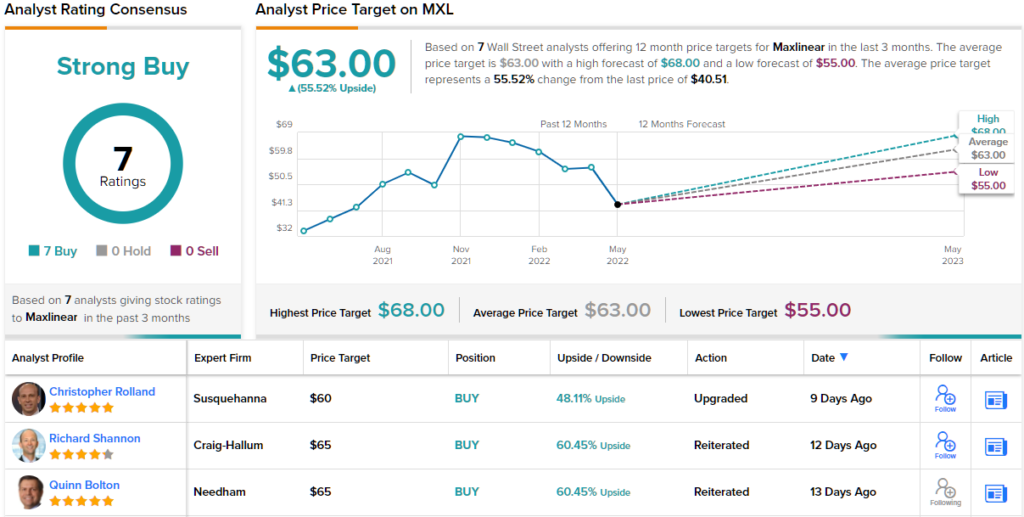

Based on the above, Mobley rates MXL shares an Overweight (i.e. Buy), and sets a price target of $66, indicating his belief in ~63% upside this year. (To watch Mobley’s track record, click here)

All in all, Wall Street clearly likes what it sees in MXL, because the stock has a unanimous Strong Buy consensus rating based on 7 positive reviews. The stock is priced at $40.51 and its $63 average price target suggests it has an upside of ~55% in the next 12 months. (See MXL stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.