Amazon (NASDAQ:AMZN) enjoyed huge success during the pandemic with its online retail business tailor-made for the era of global lockdowns but that was followed by an understandably weak period of growth once normalcy resumed.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

At the same time, the company invested heavily in expansion and over a three-year period between 2019 and 2022, its fulfillment network more than doubled in size to ~541mm square feet. However, partly due to lower fulfillment utilization, the consequent result of all that activity was operating margin compression.

Now, according to Wedbush analyst Michael Pachter, Amazon is poised to enter a new era.

“With comp issues fading and capacity utilization rising, Amazon’s core business is now well positioned with an industry-leading fulfillment infrastructure delivering 4x as many same-day or next-orders in the U.S. versus 2019,” Pachter said. “Amazon’s fulfillment capabilities are unrivaled competitively and the company continues to invest with plans to double the number of U.S. same – day delivery facilities in the coming years.”

Elsewhere in Amazon’s sprawling ecosystem, other areas of the business are poised for growth. In an environment of macro uncertainty and rising interest rates, enterprises and startups began managing costs and optimizing cloud spending, and as such, growth in Amazon’s cloud computing segment, AWS, slowed down during the second half of last year. However, with fears of a recession in the US now abating and interest rate hikes moderating, Pachter believes AWS growth has “stabilized and is poised to reaccelerate in 2H23 and into 2024.”

Additionally, against a backdrop of an improving digital advertising industry, Amazon’s high-margin advertising business should see continued growth. Pachter reckons the segment will generate revenues of more than $46 billion in 2023. With margins significantly higher than AWS, that should help the overall operating margin expand and will go toward funding “growth initiatives” across its various segments such as grocery, healthcare, autonomous vehicles, and Kuiper, Amazon’s satellite broadband network.

So, down to business, what does all this mean for investors? Considering Amazon a “top pick,” and including it on the Wedbush Best Ideas List, Pachter initiated coverage with an Outperform (i.e., Buy) rating and a $180 price target. Should the figure be met, a year from now, investors will be pocketing returns of 26%. (To watch Pachter’s track record, click here)

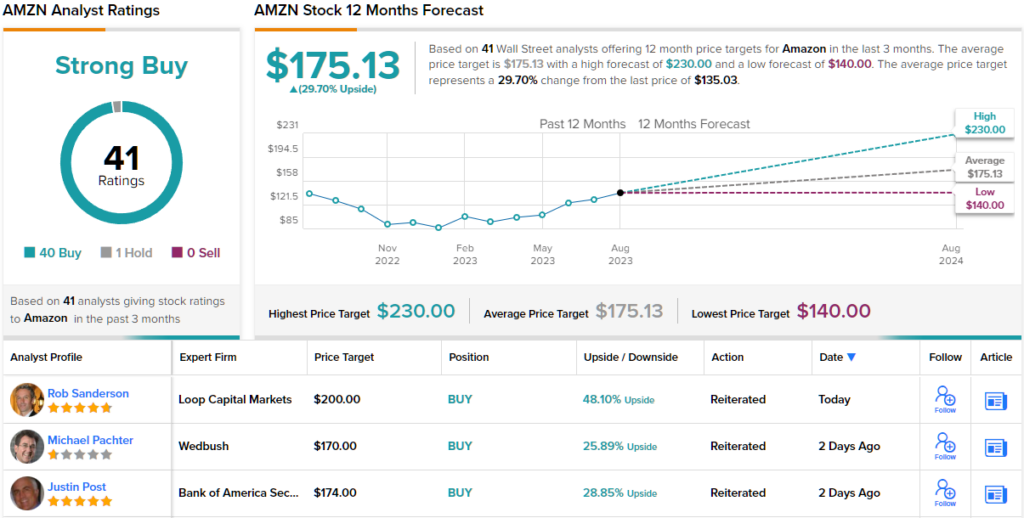

Pachter is by no means alone in his bullish outlook. Barring one fencesitter, all 40 other recent AMZN reviews are positive, culminating in a Strong Buy consensus rating. The average price target stands at $175.13, suggesting the shares will surge ~30% over the 12-month timeframe. (See Amazon stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.