Will it happen or not? That is the question economy observers have been grappling with over the past year regarding the prospect of a looming recession.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

But while not long ago the consensus was that one was all but inevitable – and a full-blown recession at that – the tune has changed more recently. Factoring in the resilient economy and the hasty retreat of prior alarming inflation levels, many financial experts now think that if a recession does materialize, it will be of the mild variety.

One of those is billionaire Dan Loeb, who moving forward sees “continued favorable economic conditions driven by declining inflation.” And that should eventually result in less hawkish monetary policy.

“While we recognize that consumers are vulnerable to the depletion of savings accumulated from fiscal stimulus and other pandemic-era emergency measures, we also see potential for the Fed to begin an easing cycle around the time American consumers begin to run low on cash, which should make for a mild recession,” the money manager said. “We also believe that since consumers and businesses (other than perhaps the commercial real estate industry) would be going into any economic slowdown with healthy balance sheets, the risk of a credit dislocation is minimal in the coming year, also reducing the risk of a severe recession.”

With the outlook appearing favorable, then, it’s worth checking out Loeb’s portfolio to find which stocks he thinks are worth leaning into right now. After all, he is the founder and CEO of Third Point, a New York-based hedge fund that oversees $14 billion.

Loeb thinks there is “healthy upside” ahead for his portfolio, and with this in mind, we ran two Loeb-favored tickers via the TipRanks database to see what Wall Street’s cadre of stock experts make of these picks. Turns out, they’re backing their chances too. Both are rated as ‘Strong Buys’ by the analyst consensus. Let’s check the details.

Hertz Global (HTZ)

We’ll first head to the car rental industry and one of the segment’s most well-known names: Hertz Global. It is one of the largest vehicle rental companies in the world, operating brands such as Hertz, Dollar, and Thrifty vehicle rental. With a history spanning over a century, Hertz has built a vast network of rental locations across various countries, enabling it to serve millions of customers annually.

However, its recent history has not been without blemishes. Hertz was an early victim of the devastating impact of the Covid-19 pandemic and went bankrupt in May 2020. It officially emerged from bankruptcy a little over a year later, in a much healthier state.

The Q2 report can bear witness to that. The company generated adjusted Net Income of $227 million, equivalent to $0.72 per share, surpassing the Wall Street estimate of $0.64.

Volume rose by 12% compared to the same period a year ago, benefiting from a utilization rate of 82%. Monthly revenue per unit in the quarter reached $1,516, marking a 230 basis points improvement compared to 2Q22.

On the top line, revenue climbed 4% year-over-year to $2.44 billion, but it missed Street expectations by $10 million.

The revenue miss, along with an adjusted EBITDA miss, did not sit well with investors, leading to a drop in shares following the report’s release.

Meanwhile, Loeb is staying long and strong. His HTZ position consists of 6,350,000 shares, currently worth over $100 million.

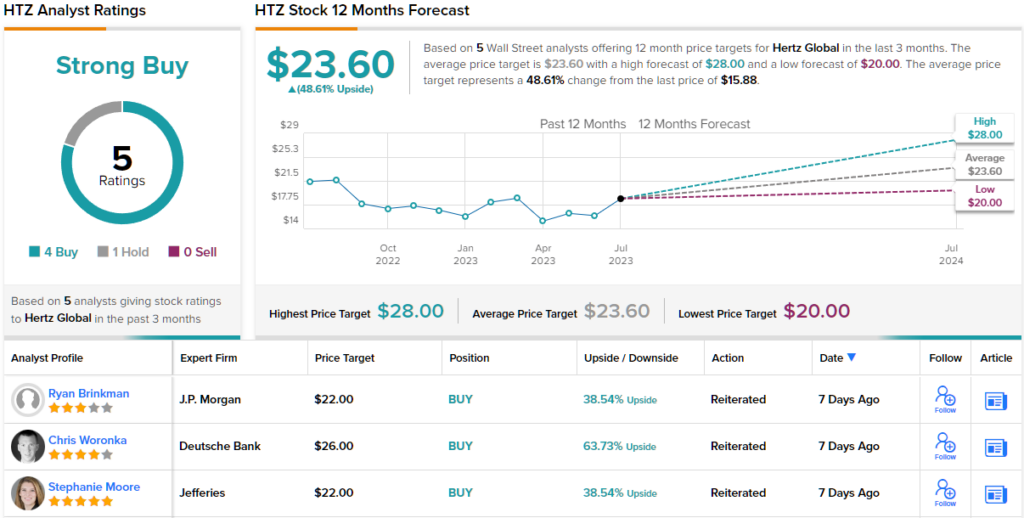

For investors seeking guidance after the post-earnings drop, Jefferies analyst Stephanie Moore has some simple advice.

“What to do with HTZ shares?” the 5-star analyst asks, “Buy more if you believe it can see pricing and margins structurally higher vs. pre-COVID given improved rationality in the industry, as well as HTZ’s more ROA mindset and ongoing productivity/ cost initiatives. Beyond what continues to be a favorable industry backdrop (low supply/high demand), we’re bullish on its strategy to play in the EV/ Rideshare channel, as well as the LT opportunity regarding autonomous vehicles/managing fleets.”

Quantifying this stance, Moore has a Buy rating on HTZ shares to go alongside a $22 price target. The implication for investors? Upside of 38% from the current trading price. (To watch Moore’s track record, click here)

Are other analysts in agreement? Most are. 4 Buys and 1 Hold have been issued in the last three months. So, the message is clear: HTZ is a Strong Buy. Given the $23.60 average price target, shares could surge ~49% in the next year. (See HTZ stock forecast)

HCA Healthcare, Inc. (HCA)

Next up is a healthcare giant. HCA Healthcare is one of the largest and most prominent healthcare providers in the US. The company oversees a vast network of hospitals, surgery centers, freestanding emergency rooms, and other healthcare facilities, serving communities in numerous states across the country. In fact, by operating 182 acute care hospitals, it is the country’s biggest non-governmental operator of such facilities. HCA Healthcare concentrates its efforts on sizeable metropolitan areas that display positive prospects in terms of population characteristics and economic conditions.

It’s a model that served the company well in its recently reported Q2 print. Boosted by strong demand for the services, revenue climbed by 7% year-over-year to $15.86 billion, in turn beating the Street’s call by $240 million. Likewise, at the other end of the equation, adj. EPS of $4.29 outpaced the $4.24 anticipated by the analysts.

The outlook was good too. The company raised both its 2023 revenue and adjusted EBITDA forecast to $63.25 – $64.75 billion (from $62.5 – $64.5 billion) and $12.3 – $12.8 billion (from $12.1 – $12.7 billion), respectively. The analysts were looking for revenue of $63.4 billion and adj. EBITDA of $12.5 billion.

As for Loeb’s involvement, he currently owns 860,000 shares, which command a market value of more than $232.8 million.

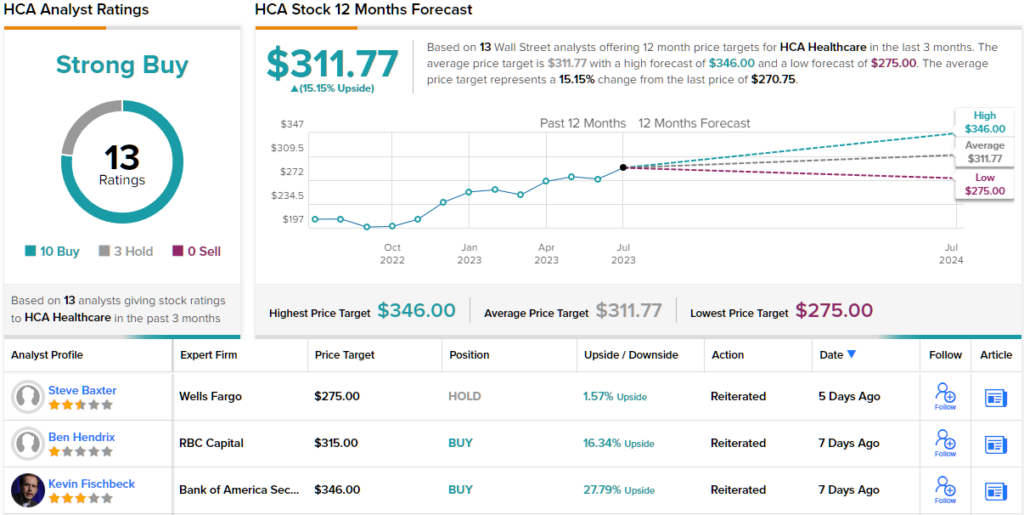

HCA also gets the backing of Truist analyst David S. MacDonald, who after scanning the Q2 readout, has plenty of good things to say.

“We remain bullish on HCA following 2Q results featuring solid volumes and top-line growth, adjusted EBITDA slightly ahead and raised FY guidance which points to stronger 2H trends. Labor continues to show improvement across metrics, and we expect ongoing volume momentum. Financial flexibility remains robust, providing ample flexibility for ongoing capital deployment/footprint expansion and the pipeline of projects is significant,” MacDonald opined.

These comments underpin MacDonald’s Buy rating, while his $340 price target suggests shares will climb ~26% higher over the coming year. (To watch MacDonald’s track record, click here)

Turning now to the rest of the Street, where other analysts are also mostly positive. The stock claims a Strong Buy consensus rating, based on 10 Buys vs. 3 Holds. Going by the $311.77 average target, a year from now, shares will be changing hands for a 15% premium. (See HCA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.