As the COVID-19 pandemic lockdowns took effect in early 2020, it seemed as if e-commerce giant Amazon (NASDAQ: AMZN) was absolutely unstoppable. Yet, trends occur in cycles, and it’s possible that the pendulum might be swinging back toward brick-and-mortar retailers now. In light of evidence that there’s growth afoot in these downtrodden businesses, I’m optimistic about big-box store chains like Barnes & Noble, Ross Stores (NASDAQ: ROST), and TJ Maxx and Marshalls parent company TJX (NYSE: TJX).

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

It’s not impossible, believe it or not, for big-box stores to regain some of the U.S. retail market share that Amazon seized during the COVID-19 pandemic. Besides, not everyone is happy to buy shares of Amazon when the company’s P/E ratio remains uncomfortably elevated at 78x.

AMZN stock could have a long way to fall, and so could the e-retailer’s stranglehold on the nation’s retail space. Surprisingly enough, an often-ignored bookseller may lead the way in a big-bog revival that could leave Amazon reeling in 2023.

Barnes & Noble Rapidly Expands Its Real Estate Footprint

In a twist of irony, Amazon started out as a bookseller, and now a bookseller could pose a serious threat to Amazon’s dominance. In particular, Barnes & Noble is now switching from contraction to expansion mode in its network of brick-and-mortar stores.

Just recently, The Wall Street Journal broke the story that Barnes & Noble intends to add 30 stores to its network in 2023. CEO James Daunt assured that Barnes & Noble now has “both the profitability and the confidence to start opening up stores again.”

Of course, it will take much more than executive-level confidence to get this bookseller back on track. After having peaked in 2008, Barnes & Noble currently has 125 fewer stores and a whole lot of catching up to do.

Yet, despite the Amazon effect, the past decade or so hasn’t been all bad news for Barnes & Noble. In actuality, according to Daunt, Barnes & Noble benefited from people reading books at home during the COVID-19 lockdowns. Plus, while Barnes & Noble locations were closed, the company was able to make improvements to those stores.

Daunt has had the daunting task of renovating Barnes & Noble bookstores that were “really bad” and “dull, unengaging, and dispirited.” Clearly, a revamping was necessary; Daunt acknowledges that if a book retailer is boring to the customers, “your sales go down by a lot, and you end up having to close stores.”

Here are Two Big-Box Store Stocks to Consider Today

Barnes & Noble is nobly taking on Amazon, but it’s not the only soldier in the battle. There are at least two other U.S.-based big-box retailers in expansion mode, and they’re actually investable right now.

Unfortunately, Barnes & Noble isn’t directly tradable on a major American stock exchange. However, enterprising investors don’t have to stay out of the big-box trade completely. They can buy shares of clothing retailers Ross and TJX, which are also waging war against Amazon.

If you like to shop at T.J. Maxx and Marshalls, you’ll be glad to know that TJX added 104 net new store locations in 2022 and plans to add another 1,500 in the coming years, according to a company spokesman (via the Wall Street Journal). TJX’s P/E ratio of 27.2x and 1.5% annual dividend yield should pique the interest of value and income investors, as well (remember, Amazon doesn’t pay a dividend).

Meanwhile, Ross “expects to add 92 net new off-price clothing and home-accessories locations in 2022,” according to The Wall Street Journal. That’s a pretty good start, and hopefully, Ross will ramp up its expansion pace in the coming year, leading to improved revenue and earnings. Ross also has a P/E ratio of 27.9x and pays a 1.08% dividend yield, so ROST stock could be the big-box buy-and-hold you’ve been searching for.

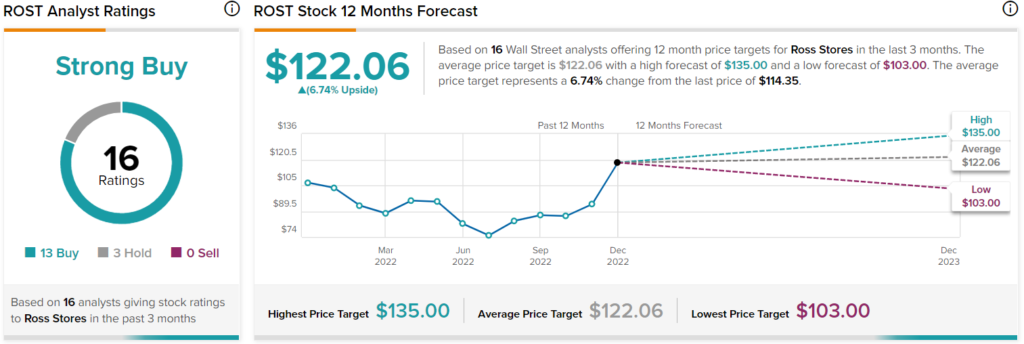

Is ROST Stock a Buy, According to Analysts?

According to TipRanks’ analyst rating consensus, ROST is a Strong Buy, based on 13 Buys and three Hold ratings. The average Ross Stores price target is $122.06, implying 6.7% upside potential.

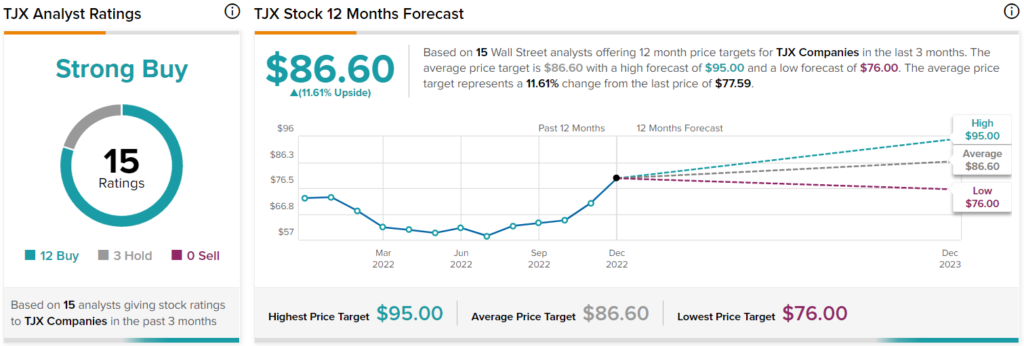

Is TJX Stock a Buy, According to Analysts?

Meanwhile, TJX is a Strong Buy, based on 12 Buys and three Hold ratings. The average TJX price target is $86.60, which implies 11.6% upside potential.

Conclusion: Should You Consider Big-Box Retail Stocks?

Barnes & Noble appears to be leading a big-box rebellion against the Amazon monster, while analysts consider ROST and TJX shares as Strong Buys. Is now the time to take a long position in ROST and TJX, then?

Personally, I like AMZN stock even though it’s pricy, but ROST and TJX could actually post bigger gains next year due to their favorable growth-and-value combos. So, don’t count America’s big-box store chains out, as some of them might win the war against – or at least take back some market share from – the e-commerce beast we call Amazon.