As a business that’s often taken for granted, waste and environmental services firm Waste Management (NYSE:WM) has been uncharacteristically exciting. Since October 3, shares have been flying higher. While that might cause some investors to question whether any additional upside remains, the company is worth a look because it aligns with Generation Z’s focus on sustainability. That, along with the entity representing a critical infrastructure play, makes me long-term bullish on WM stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

WM Stock is Practically a No-Brainer Market Idea

Invariably, anything involving the capital markets carries risks. However, for investors seeking the closest idea to a no-brainer, it’s difficult to overlook WM stock. Essentially, Waste Management benefits from a natural monopoly. Due to the various regulations needed to operate landfills and other disposal facilities, the company is practically ingrained into the broader infrastructural ecosystem. As well, sustainability trends arguably make WM stock relevant.

While the company may be called Waste Management, its leadership team, over the years, implemented protocols to align the organization with contemporary sustainability trends. Indeed, the issue has been forced on the wider industry in many respects. With Americans generating about 4.4 pounds of trash per day, landfill space is quickly filling up. Therefore, it’s vital that the waste services sector get ahead of the wave.

To that end, Waste Management features innovative recycling and waste solutions that undergird the circular economy. This system focuses on the reuse and regeneration of materials or products, thus extending the life cycle of products. Basically, it’s a social directive to reduce waste to the bare minimum.

As part of its sustainability goals, Waste Management aims to increase the recovery of materials by 60% to 25 million tons. In addition, it seeks to reduce emissions and deploy more renewable energy uses. Finally, it’s not leaving out social responsibility, with a directive to improve both female and minority representation.

These attributes should easily win with the Gen Z demographic. According to one survey, 82% of this cohort expressed concern about the planet’s condition. Further, 72% stated that they have modulated their behaviors to limit their environmental impact. So, efforts to promote social equity should resonate more deeply with young consumers and investors.

Better yet, even if WM stock fails to line up with any of the aforementioned attributes, people will continue to generate waste. Given this reality, Waste Management enjoys “job security.”

Options Traders Lend Their Support

Despite the many positives underlying WM stock, it’s natural for investors to be somewhat hesitant. Since the beginning of October, shares have gained nearly 22%. Waiting for a pullback might seem prudent, especially with the average analysts’ price target implying little to no growth potential. Nevertheless, options traders seem to have a completely different take.

According to TipRanks’ unusual options activity screener, since the January 12 session, 34 of the most unusual transactions feature bullish implications. In sharp contrast, only 16 feature bearish implications. What’s more, the highest-volume transactions are bullish ones.

In particular, two transactions stand out: 544 contracts of the WM Feb 16 ’24 185.00 call and 502 contracts of the WM Feb 16 ’24 180.00 put. Let’s tackle the easier one first.

Call options give holders the right (but not the obligation) to buy the underlying security at the listed strike price. Assuming a face-value interpretation that’s not part of a complex multi-leg strategy, buying a call is bullish. In this case, investors are betting that by the February 16 deadline, WM stock will reach (and perhaps exceed) $185. That’s a very reasonable bet, considering WM’s momentum.

Now, the bullish put is a bit more complicated. At face value, put holders have the right (but not the obligation) to sell the underlying security. It’s a way to profit from falling stocks, which appears contradictory in this case. However, puts can be bullish if one sells/shorts them.

Effectively, sold (written) puts allow traders to collect income from the sale of the contract. Should the target stock fall to or below the strike price, the contract writer must buy shares. In some ways, you can look at the strike price of a sold call as the support line.

At $180, that’s an elevated support line, lending itself to a bullish assessment.

Not Discounted but Predictable

When it comes to a reliable and predictable investment like WM stock, it must give up something, usually in the form of a high multiple. And that’s the case here. Currently, WM trades at a trailing-year earnings multiple of 32.7x. That’s not outrageous by any means. However, when stacked against norms for similar industries, it’s not a discount by any measure.

Still, that doesn’t mean WM stock isn’t a good deal. For one thing, it’s a consistently profitable enterprise, a dynamic that likely won’t change anytime soon. Also, it provides a dividend yield of 1.52%. It’s not the most generous rate of passive income. However, shareholders have banked on it, with management upping the payout consecutively for more than 15 years.

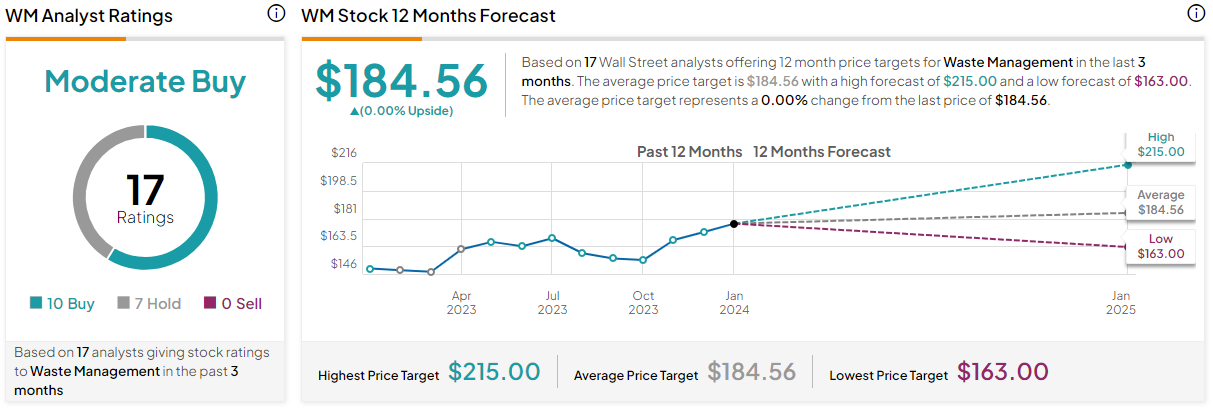

Is WM Stock a Buy, According to Analysts?

Turning to Wall Street, WM stock has a Moderate Buy consensus rating based on 10 Buys, seven Holds, and zero Sell ratings. The average WM stock price target is $184.56, implying that the stock is fairly valued at current levels.

The Takeaway: It’s Not Exciting, but You Can Bank on WM Stock

Waste Management offers a compelling, reliable opportunity, thanks to its focus on sustainability and “natural monopoly” status. Gen Z’s environmental concerns and the company’s innovative recycling solutions align perfectly, while options traders and analysts are generally bullish. Despite the stock not trading at a discount, WM stock enjoys consistent profitability and a rising dividend, making it a predictable and valuable long-term investment.