Have you been patiently awaiting a better entry point for Waste Management (NYSE:WM) stock? Well, you are not alone! Despite its attractive qualities, this industry leader has historically commanded a higher valuation, causing many value-focused investors to hesitate. Interestingly, even in the face of significant interest rate increases, Waste Management has maintained its premium valuation, casting doubt on the possibility of a significant price drop and a more compelling buying opportunity.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The reason I support this case is that, precisely due to Waste Management featuring some exceptional qualities amid an uncertain market environment, investors might continue to be willing to pay a premium valuation “indefinitely.” On the one hand, this could suggest further upside to the stock as Waste Management’s revenues and profits grow. On the other hand, investors getting rug-pulled is always a possibility and a risk that should not be ignored. Hence, I am neutral on the stock.

What’s Driving Waste Management Stock Higher?

Looking at Waste Management’s stock price chart, one can only be impressed with the stock’s incredibly consistent tendency to move upwards. WM has held its ground firm even with interest rates rapidly rising, which is odd given that most equities have experienced a valuation compression to a degree.

In my view, Waste Management’s invariable long-term appreciation is due to its underlying set of unique qualities that is like no other, setting up the company for continuous success even during the harshest trading environments. Let’s break them down!

1. Recession-Proof Cash Flows

Concerns about a potential recession have remained prevalent among investors since the onset of the pandemic. However, regarding Waste Management, the likelihood of the company facing any significant impact in such a scenario is exceedingly low. Waste Management can be rightfully considered a “recession-resistant” stock, owing to the indispensable nature of waste management services, which are essential across all communities and remain resilient even during economic downturns.

Both communities and businesses consistently generate waste, irrespective of economic conditions, thereby ensuring a steadfast demand for waste management services. This robust demand has proven consistent through various challenging periods, encompassing events such as the Great Financial Crisis and the COVID-19 pandemic. It’s noteworthy that Waste Management has never posted an unprofitable year for over two decades, attesting to its remarkable recession-resistant character.

2. Lack of Competition

Another critical factor that consistently piques investor interest in Waste Management stock is the limited competitive landscape within this tightly-knit industry. The waste management industry demands substantial capital investment, characterized by steep startup costs and extensive infrastructure prerequisites. Consequently, these formidable barriers pose significant challenges for potential newcomers attempting to penetrate the market and vie with well-established corporations.

Overall, Waste Management, along with its peers like Republic Services (NYSE:RSG), effectively constitutes an oligopoly. Examining the previous year’s market share in terms of landfill volume managed in the United States, it becomes evident that Waste Management, Republic Services, and municipal entities jointly command an impressive 75% market share. Notably, Waste Management holds the leading position, exerting control over 29% of the market.

The oligopolistic nature of this industry yields several notable advantages, such as robust pricing power, a dearth of substantial competitors, and the facilitation of long-term planning due to reduced uncertainty—attributes that garner significant appreciation from investors.

3. Consistent Growth

You might be surprised to know that the waste management industry is growing quickly. The industry as a whole is expected to expand at a compound annual growth rate (CAGR) of 5.4% from this year to 2030 (when it’s expected to reach $1.96 trillion). Given Waste Management’s stronghold position in the space, the company has consistently captured the ever-present trend of growing waste, which has been evident both in its historical results (five-year net income growth of 10.6%) and its most recent numbers.

In particular, in its most recent fiscal Q2 results, revenues grew by 1.8% to $5.12 billion, powered by higher pricing power and higher processing volumes, partially offset by a slightly weaker disposal yield. Notably, the core price growth stood at an impressive 6.9%, a testament to the management’s adeptness in securing price increases to match the inflationary environment. Further, adjusted EPS came in at $1.51, up from $1.44 last year.

Waste Management’s Valuation Premium is Not Going Away Soon

The longer I follow Waste Management, the more I grow convinced that its valuation premium is not going away anytime soon. Sure, the company’s qualities are one of a kind. Nevertheless, I expected that with rates on the rise, Waste Management’s valuation would be bound to normalize, but even with growth slowing down in its most recent Q2 results, investor interest in the stock has yet to ease.

Consensus estimates for Fiscal 2023 point toward EPS of $5.94, implying a forward P/E of about 27. This is on the very high end of the stock’s past-decade historical average, even in the face of interest rates reaching their highest levels within this timeframe. Hence, while I do remain cautious over the possibility of a potential valuation multiple compression, I wouldn’t be surprised if investors’ strong appetite for the stock is sustained throughout this macro turmoil.

Is WM Stock a Buy, According to Analysts?

Turning to Wall Street, Waste Management has a Moderate Buy consensus rating based on four Buys and six Holds assigned in the past three months. At $177.55, the average Waste Management stock forecast implies 10.95% upside potential.

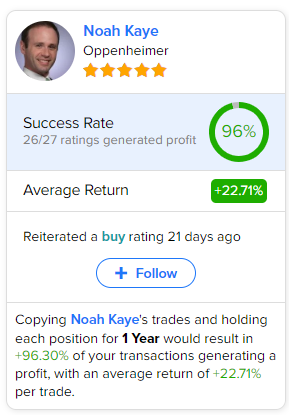

If you’re wondering which analyst you should follow if you want to buy and sell WM stock, the most accurate analyst following the stock (on a one-year timeframe) is Noah Kaye from Oppenheimer, featuring an average return of 22.71% per rating and a 96% success rate. Click on the image below to learn more.

The Takeaway

Waste Management’s enduring trend of commanding a premium valuation has persisted, even in the face of mounting interest rates and a deceleration in revenue growth. On the one hand, compelling factors underpin investors’ fascination with Waste Management. These include its recession-resistant cash flows, the industry’s oligopolistic structure, and the sustained demand for waste management services anticipated throughout this decade’s conclusion.

However, it’s crucial for investors to exercise vigilance against potential market shifts. The looming possibility of Waste Management’s valuation reverting to its historical average (around 20x earnings) poses a genuine threat to investors’ overall returns. Thus, I recommend considering a cautious approach when considering the stock’s investment potential.