Investors looking for alpha in an uncertain market environment could do worse than following in the footsteps of legendary stock pickers and probably none can match Warren Buffet’s reputation. Not for nothing the “Oracle of Omaha” is considered one of the all-time greats and for nearly 60 years, between 1965 and 2022, his Berkshire Hathaway firm’s returns have doubled those of the S&P 500.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

So, it’s definitely worth nosing through Buffett’s portfolio to see which stocks he currently holds. And when some of those stocks also get the endorsement of one of Wall Street’s top banks, such as Morgan Stanley, it sends an even stronger signal these names could be ripe for the picking.

With this in mind, we opened up the TipRanks database to pull up the details on a pair of stocks that get a thumbs up from both of these investing institutions. Here’s the lowdown.

Nu Holdings (NU)

Warren Buffett hates bitcoin, right? Maybe so, but interestingly, he holds a position in Nu Holdings, Brazil’s leading fintech company and one that already offers bitcoin payments.

That tidbit of information aside, this financial disruptor provides a digital banking platform and already caters to more than 36% of Brazil’s adult population, while it has also expanded to Mexico and Colombia. The strong penetration has been accrued via its mobile app, which offers a wide range of financial services. Although Latin America has 600 million people, the region’s rates of banking and credit card penetration are among the world’s lowest. Therefore, NU is in a good position to win a sizable portion of this underserved market.

The growth on tap has been impressive, as was the case in the most recent quarterly readout, for 4Q22. Boosted by the expansion of its active Brazilian client base and product cross-selling, revenue rose by 128% year-over-year to $1.45 billion, while adj. net income increased dramatically from $3.2 million in Q4 2021 to $113.8 million. The company saw out 2022 with 74.6 million customers, amounting to a 38% y/y increase.

It’s no wonder, then, that Buffett likes this name. He currently owns 107,118,784 shares. At the current market price, these are worth north of $508 million.

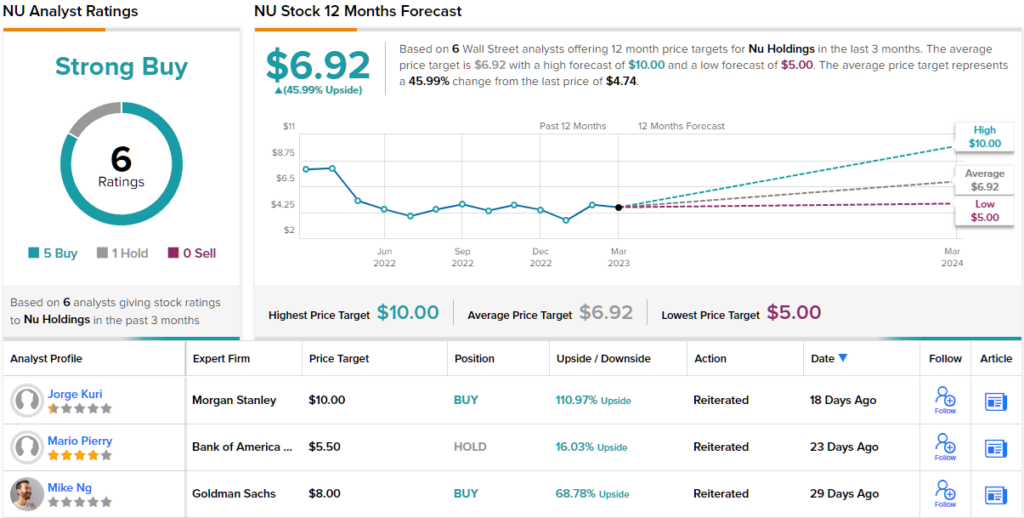

Meanwhile, Morgan Stanley analyst Jorge Kuri has not been shy in laying out the bull-case for this LATAM bank disruptor.

“We think Nubank is well-positioned to build one of the largest and most valuable banking franchises in Latam, on the back of superior technology, best-in-class customer satisfaction, valuable brand and strong cohort performance and unit economics,” Kuri explained. “The company has multiple attractive avenues to increase top line growth, including a rapidly expanding client base, roll out & cross-sell of new products, new geographies, M&A, and potential expansion into new business verticals. Favorable demographic trends provide durable growth opportunity.”

These comments form the basis for Kuri’s Overweight (i.e. Buy) rating, while his $10 price target makes room for one-year gains of a hefty 111%. (To watch Kuri’s track record, click here)

Turning now to the rest of the Street, other analysts are on the same page. With 5 Buys and 1 Hold, the word on the Street is that NU is a Strong Buy. The shares are currently trading for $4.75 and have an average price target of $6.92, suggesting a one-year gain of 46%. (See NU stock forecast)

Snowflake Inc. (SNOW)

The second stock we’re looking at, Snowflake, is a data cloud provider, offering a public service that allows organizations to pool resources and benefit from nearly unlimited scale and performance. Looking at Snowflake by the numbers, we find it has over 7,800 customers (including 330 million-dollar-plus customers) and $3.7 billion in the work backlog.

When Snowflake made its loud entrance to the public markets in September 2020, it did so as the largest-ever software IPO and doubled its market cap on its debut trading day. The shares, though, have not been immune to the overall market conditions, and have retreated 41% over the past 12 months.

That said, the company’s fourth quarter of fiscal 2023 results provided beats on both the top-and bottom-line. Revenue climbed by 53.5% year-over-year to $589.01 million, outpacing expectations by $13.56 million. Adj. EPS of $0.14 beat the $0.05 forecast. Additionally, the company also authorized a $2 billion stock repurchase program.

Investors, however, were disappointed with the outlook, which suggested the growth will slow down. For 1QF24, the company anticipates product revenue in the range between $568 million and $573 million, amounting to a y/y growth rate of 44% to 45%. The Street was looking for $582.1 million.

Buffett, who is known to have a “buy and hold forever” strategy, must also has have heard the oft-repeated phrase “data is the new oil.” He holds 6,125,376 SNOW shares, which are currently worth $842 million.

Morgan Stanley enters the frame here with 5-star analyst Keith Weiss, who believes the soft F24 outlook is nothing to be concerned about.

“While disappointed in the slower pace of growth now expected in FY24, we remain confident in the longer-term opportunity ahead for Snowflake and the company’s competitive positioning for that opportunity. Over the course of FY23, Snowflake made progress in expanding the solution portfolio with new solutions like Snowpark and Streamlit, orienting its go-to-market, towards specific industry verticals and expanding its partner ecosystem – including a notable expansion of the go-to-market partnership with AWS, and at the same time rapidly expanding margins,” Weiss wrote.

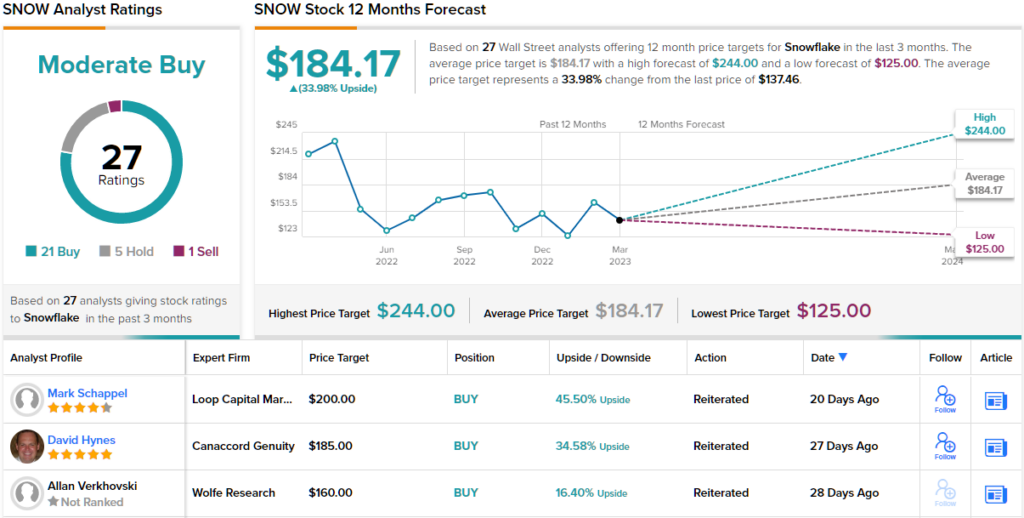

Accordingly, Weiss rates SNOW shares an Overweight (i.e. Buy) backed by a $215 price target. That should see the shares post gains of 56% over the next 12 months. (To watch Weiss’s track record, click here)

Elsewhere on the Street, the stock receives an additional 20 Buys, 5 Holds and 1 Sell, for a Moderate Buy consensus rating. The analysts expect the shares to appreciate by 34% over the coming year, considering the average target stands at $184.17. (See Snowflake stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.