Markets tanked yesterday, there’s no other way to put it. The NASDAQ fell more than 5%, the S&P 500 fell more than 4%, and the Dow Jones shed 1,200 points, also a 4% loss. The sharp drops hit after the official August inflation numbers came in substantially worse than expectations.

The data release has also firmed up convictions that the Federal Reserve will enact another 75 basis point rate hike later this month. Taken together, rising prices and higher interest rates increase the chances of a severe recession in the near future.

But there are concrete steps that the investors can take, now, to protect themselves in a difficult economic environment. Perhaps the easiest defensive stance to take is a move into ‘recession proof’ dividend stocks. Legendary investor Warren Buffett is a long-time advocate of this strategy.

Buffett keeps two main criteria when choosing dividend payers for his stock portfolio. First, Buffett always looks for companies with “an ability to increase prices rather easily without fear of significant loss of either market share or unit volume.” And second, he seeks out companies that also have “an ability to accommodate large dollar volume increases in business with only minor additional investment of capital.”

Buffett’s company, Berkshire Hathaway, currently makes dividend payers a majority of its portfolio. We’ve used the TipRanks platform to pull up details on two major dividend stocks in which the billionaire has invested billions. Let’s take a closer look at them, using the latest data and the analyst commentary.

Citigroup, Inc. (C)

The first stock we’ll look at, Citigroup, is one of the ‘Big Four’ banks in the US; it is the owner of Citibank, and boasts over $2.3 trillion in total assets. Citigroup is headquartered in New York City and does business globally; the company has a presence in more than 160 countries, providing a wide range of financial services and products to corporate, investment, institutional, governmental, and individual customers.

The company’s top line has been making gains year-over-year; the $19.6 billion reported in 2Q22 was up 11% from the year-ago quarter. Earnings beat the forecast, but declined y/y. The company reported total net income $4.5 billion, or $2.19 per diluted share; the total net was down 27% from 2Q21. EPS, while down 23% from the prior year, beat the $1.68 forecast by a wide margin.

Of interest to investors here, Citigroup returned $1.3 billion worth of capital to common shareholders during the second quarter, through both share repurchases and dividend payments. Citigroup has a long history of keeping up a reliable dividend, a history that stretches back to the late 1980s. The common share dividend now stands at 51 cents per quarter. It’s been held at this level for the past three years, and was kept steady despite the corona pandemic crisis. The dividend annualizes to $2.04 and gives a yield of 4.1%.

Warren Buffett remains long and strong, and made no changes to his position during the quarter. Berkshire Hathaway owns 55,155,797 shares worth over $2.7 billion right now.

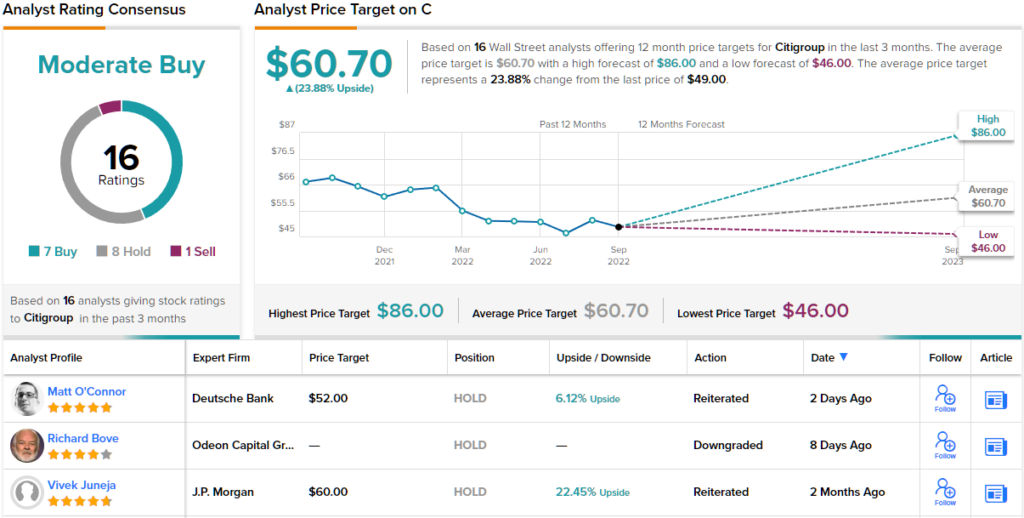

Oppenheimer’s 5-star analyst Chris Kotowski also likes what he sees here. Acknowledging that C shares are trading well below the company’s total book value (TBV), he writes: “It’s amazing to think that just getting back to TBV would equate to a 61% return, and there’s a 4.1% dividend on top of that. Of course, there is more to play for here than the embedded capital in the company. There is a powerful client franchise… and 2Q22 results began to show some of the earnings power of that franchise.”

To this end, Kotowski puts an Outperform (i.e. Buy) rating on these shares, and his price target, set at $86, implies a robust 75% one-year upside potential for the stock. (To watch Kotowski’s track record, click here)

The Oppenheimer view represents the bulls here; the Street shows a definite split in the reviews for C. Out of 16 recent analyst reviews, there are 7 Buys, 8 Holds, and 1 sell, for a consensus rating of Moderate Buy. The stock is priced at $49 and the $60.70 average target suggests it has ~24% upside for the coming year. (See Citigroup stock forecast on TipRanks)

Kraft Heinz (KHC)

From banking, we’ll shift our sights to the food and grocery sector. As ‘recession proof’ sectors go, this is one of the classics – no matter what happens to the economy, food producers will continue to make sales. The same argument can be made for food firms as ‘inflation shelters;’ even though the August food index segment of the CPI showed an 11.4% increase over the past year, the higher prices don’t mean that people have stopped buying food.

And this brings us to Kraft Heinz. This is one of the best-known names in the global food sector; it is North America’s third largest food and beverage company, and the world’s fifth largest. In both 2020 and 2021, Kraft Heinz saw $26 billion in annual sales revenue. The company’s quarterly revenues have, for past several years, consistently come in between $6 billion and $7 billion. Kraft Heinz shares are up 1% this year — more than enough to outperform the broader markets.

Kraft Heinz has been paying out a common share dividend since 2012, and has kept that dividend reliable – never missing a payment – through that time. The payment has been held at 40 cents per common share since the start of 2019, and at this rate, annualized to $1.60, it gives a yield of 4.5%.

This stock is one that caught Buffett’s attention years ago. The billionaire first bought into KHC in the third quarter of 2015, and he currently holds well over 325 million shares of Kraft Heinz, representing a 26.6% ownership in the company. Buffett’s stake is worth approximately $11.4 billion at current valuations.

Buffett is far from the only bull here. 5-star analyst Christopher Growe, of Stifel, covers this stock and writes: “The company is managing inflation quite well with robust pricing and low levels of elasticity in a portfolio less influenced by private label (below the food industry average). This backdrop has supported a stronger sales and earnings growth performance for the business thus far in 2022 and this improved business and portfolio of brands should continue to support this top-tier growth for the company.”

Turning to the dividend, Growe expresses “confidence in the company’s [4.5%] dividend yield and we expect that dividend to grow in line with earnings going forward.”

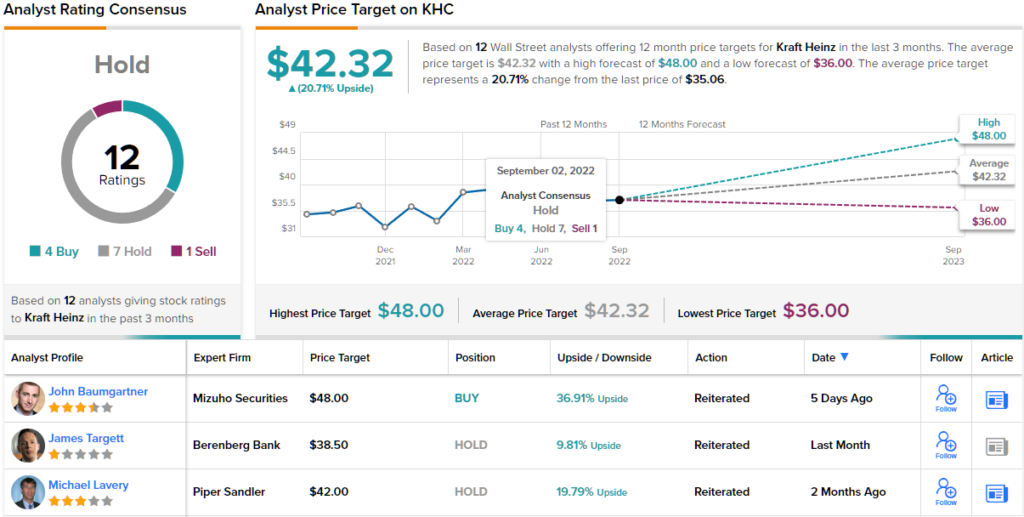

In Growe’s view, KHC gets a Buy rating, and his $43 target price indicates his expectation of ~23% share gain going forward. (To watch Growe’s track record, click here)

While Growe is bullish here, the Street is not fully convinced. KHC shares have a consensus rating of Hold, based on 12 analyst reviews that include 4 Buys, 7 Holds, and 1 Sell. But the analysts might as well have said “buy” — because, on average, they think the stock, currently at $35.06, could zoom ahead to $42.32 within a year, delivering ~21% profits to new investors. (See KHC stock forecast on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.