Today’s market environment is a volatile roller coaster, featuring sudden shifts up or down from day to day, backdropped by a drumbeat of news items – inflation data, unemployment data, the SVB collapse, the Federal government’s promise of a bailout, the uncertainty on the Federal Reserve’s next interest rate decision. It’s all enough to make an attentive investor’s head spin, looking for a guide through the data noise.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Fortunately, there are guides available. The professional stock analysts on Wall Street, the experts who have built careers and reputations based on the accuracy of their stock recommendations, have the knowledge and know-how to cut through volume of market data and find the important nuggets that indicate the right stocks for any market conditions.

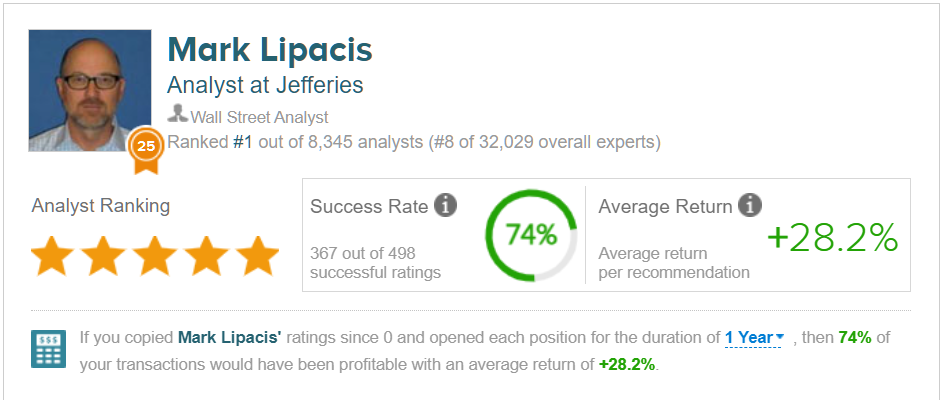

Here, we’ll turn to Jefferies analyst Mark Lipacis, who going by the past couple of years’ performance holds the #1 rating out of more than 8,300 analysts in the TipRanks database. Lipacis’ high ranking is based on his high success rate in calling stocks; he has 498 recommendations on file, with a 74% success over the past 12 months. And – following Lipacis’ calls over the past year would have brought in a 28% return.

In the last few months, as 2023’s volatility has picked up steam, Lipacis has been busy pointing out solid stocks. Let’s take a look at a few of his calls – 3 stocks also rated as Strong Buys by the analyst consensus – using his commentaries and the latest data from the TipRanks platform.

Applied Materials (AMAT)

The first stock on our list is Applied Materials, a firm that fills a vital link in the semiconductor industry’s production chain. Applied Materials designs and builds the software and equipment necessary in the production of integrated circuits, equipment used in chip production but also found in a range of other devices, including the flat panel displays so ubiquitous in smartphones, tablets, and laptops. The size of this niche is clear from two numbers: AMAT boasts a $100 billion-plus market cap, and generated more than $25.5 billion in revenues last year.

So AMAT is a giant, in a growing industry. But it’s not just financial size that’s important here; AMAT also has more than 17,000 patents protecting its intellectual property, and a $2.8 billion investment in technology R&D. This supports a strong business, that generated a 7% y/y revenue increase for Q1 of fiscal year 2023, for a top line of $6.74 billion.

Of particular interest to return-minded investors, AMAT also generated $2.27 billion in cash from operations in its fiscal Q1, a total that allowed the company to return $470 million directly to shareholders. This was split between $250 million share buybacks and $220 million in dividends. The company is clearly committed to capital return, as its most recent dividend declaration, for the payment to go out on Jun 15, included a 23% increase to 32 cents per common share.

In his coverage of Applied Materials, Lipacis dives into the firm’s tech and market share to come up with a bullish bottom line. The analyst writes, “Strength in AMAT’s ICAPS (IoT, Communications, Automotive, Power and Sensors) business reflects the resiliency of WFE (wafer fabrication equipment) spending as the industry benefits from: 1) bigger chip; 2) increasing manufacturing complexity; 3) Tectonic Shift to IoT era driving demand for trailing node demand; and 4) semi-nationalization ala CHIPS Act et.al. We expect AMAT to re-rate to a 10%-to-20% premium to the SPX over the next several years as market appreciates the secular drivers… we view the risk/reward ratio as attractive.”

AMAT remains a “top pick” for Lipacis, who rates AMAT as a Buy, and his price target, set at $140, implies a 14% upside for the coming year. (To watch Lipacis’ track record, click here.)

There are 20 recent analyst reviews on record for this stock, and the breakdown – 16 Buys, 3 Holds, and 1 Sell – gives a Strong Buy consensus rating. The shares are selling for $122.60 and have an average price target of $135.92, suggesting a one-year gain of 11%. (See Applied Materials’ stock forecast at TipRanks.)

Marvell Technology Group, Inc. (MRVL)

Next up is Marvell Technology, another player in the semiconductor chip industry. But where AMAT, above, deals with the equipment needed to make semiconductors, Marvell both designs and produces the actual silicon chips. The company, which boasts a $34 billion market cap, is considered a leading player in the data center industry, and its chips are used in ethernet networks, server stacks, and storage accelerators.

The chip industry still hasn’t shaken off the woes of last year’s supply chain disruptions, and as a result, Marvell’s recent fiscal 4Q23 numbers were somewhat mixed. The company’s top line of $1.42 billion was up 6% year-over-year, but declined 7.7% quarter-over-quarter; the Q4 revenues did beat the forecast by a modest $10 million. At the bottom line, Marvell reported a non-GAAP EPS of 46 cents; this as down 8% y/y, and came in 1-cent below the Street’s expectations.

For the full year, Marvell reported $5.92 billion in revenue, compared to $4.46 billion in fiscal year 2022. The company’s non-GAAP earnings for fiscal 2023 came to $2.12 per diluted share, based on total net income of $1.82 billion.

Looking ahead to the fiscal 1Q24 results, due out in June, Marvell is guiding toward a top line of $1.3 billion and non-GAAP diluted EPS of 29 cents. These figures are estimated at +/- 5% and 5 cents, respectively.

Turning to Mark Lipacis, we find that the analyst describes Marvell’s last quarterly results as ‘meet/miss,’ but sees better times ahead for the company. Lipacis writes of Marvell’s status and prospects, “We think MRVL is shipping below consumption in datacenter, and we expect a snapback there along w/ 5G and ASIC cycles will translate to upward revisions through CY23… MRVL expects tailwinds in (1) cloud-optimized silicon for compute and (2) networking infrastructure for interconnects. MRVL views high-speed optical connections to be best suited to support AI supercomputers highlighting YY 4x growth in AI-related PAM DSP revenue in F23.”

These comments, for Lipacis, justify a Buy rating, and he gives the shares a price target of $55 to indicate a potential upside of 38% on the 12-month horizon.

The Street’s view on MRVL is clearly bullish, too, as the 22 recent reviews include 20 Buys against just 2 Holds, for a Strong Buy consensus rating. The shares have an average price target of $55.35 and a current trading price of $39.97, implying a 38% one-year upside potential. (See Marvell’s stock forecast at TipRanks.)

SMART Global Holdings (SGH)

The last stock on our list is SMART Global Holdings, another semiconductor chip firm. SMART operates through a network of subsidiaries, making components for OEM providers. Specifically, SMART makes memory chipsets for communications systems, mobile computing, networking, and storage systems. SMART produces chips for DRAM, Flash storage, and solid-state memory circuits, and its products are found in smartphones, tablets, laptops, and desktop computers.

Over the past two years, SMART’s quarterly revenues have held in a range, roughly between $437 million and $470 million. The company’s most recent report, from fiscal 1Q23, showed a top line of $465 million, at the top end of that range – and up 6.3% sequentially. The top line came in nearly $20 million above the Street’s forecast.

On earnings in 1Q23, the company’s non-GAAP EPS was reported at 79 cents per share; while down from 80 cents in 4Q22 and $1.08 in 1Q22, that 79-cent figure beat the forecast by a wide margin of 22 cents, or 38%. Also of note, SMART showed a non-GAAP gross margin in the quarter of 27.8%, an increase of 320 basis points quarter-over-quarter.

Top analyst Mark Lipacis was duly impressed by SMART’s performance in a difficult environment, and wrote just after the fiscal 1Q23 release, “Despite significant weakness in LED/Brazil, SGH’s multi-year strategy of diversifying from its memory business yielded strong profitability results with record GMs. While mgmt did not provide visibility on trough for Brazil and LED, we believe street revs for FY23 are adequately de-risked as the company is well-positioned for LT resilient earnings growth.”

Along with these comments, Lipacis gives the stock a Buy rating and a price target of $19 to suggest a 22% gain for the year ahead.

While SMART Global Holdings only has 5 recent analyst reviews on record, they are all positive, making the Strong Buy consensus rating unanimous. The shares have a current trading price of $15.60 and an average price target of $23.80, implying a robust 52% one-year upside in the offing. (See SMART’s stock forecast at TipRanks.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.