Walgreens Boots Alliance stock (NASDAQ:WBA) currently offers a massive 9.3% dividend yield – right around the highest in the company’s near-40-year history in the public markets. Shares of the pharmacy giant have plummeted to multi-decade lows, signaling the market’s expectation for an impending dividend cut. Thus, Walgreens’ legendary 47-year dividend growth streak may soon be coming to an end.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Still, a dividend cut could unlock notable upside potential from the stock’s current levels. Thus, I am neutral on the stock.

Is Wall Street Correctly Predicting a Dividend Cut?

Wall Street has persistently anticipated challenges surrounding Walgreens’ ability to sustain its dividend. Shares have been on a downward decline since 2018, as the company’s gradually worsening profitability against a gradually growing dividend doesn’t really sound like a sustainable combo. Indeed, Walgreens’ adjusted EPS peaked in Fiscal 2018, when it came in at $6.02. Since then, it has declined almost every year. In fact, adjusted EPS for Walgreens’ Fiscal 2023, which ended this past August, landed at just $3.98.

For some context here, let’s take a look at the company’s most recent Fiscal Q4 results. For the quarter, revenues actually grew by 9.2% to $35.4 billion compared to last year, or by 8.3% in constant currency. Increased revenues were driven by robust sales growth in both the U.S. Retail Pharmacy and International segments and a significant contribution from the U.S. Healthcare segment.

Nevertheless, as per the company’s report, a decline in demand for COVID-related services, a consumer base exhibiting greater caution, and a preference for value-driven choices, combined with a milder respiratory season, collectively exerted margin pressures during the quarter.

Thus, Walgreens’ adjusted operating margin dived to just 1.6%, resulting in an adjusted operating profit of just $683 million, down 9.8% year-over-year. As a result, adjusted net income, which also accounts for interest amongst other expenses, fell by 17.1% to $575 million.

With the company’s profitability getting compressed this fast — and remember, this has been a continuous trend since 2018 — it’s no wonder the market is bracing for a dividend cut. Given the quarterly dividend’s substantial demand of approximately $415 million per quarter, totaling $1.66 billion annually, a prudent move for management would be to prioritize deleveraging. This proactive approach is crucial to avoid further erosion of the bottom line, which seems increasingly inevitable.

The heightened likelihood of a dividend cut is underscored by the company’s customary July dividend increases being foregone. Notably, this past July marked an exception, with the company skipping its usual hike, signaling the lack of adequate affordability. Although WBA maintains a remarkable 47-year streak of dividend growth, the recent deviation suggests that this legendary track record may end sooner rather than later.

A Dividend Cut Could Unlock Upside Potential

Walgreens cutting its dividend may seem bad on the surface, especially to income-oriented investors who have been collecting growing dividends from the company for decades. However, it could unlock notable upside potential.

As I previously mentioned, implementing a strategic cut would enable the company to channel additional funds toward mitigating its expenses, ultimately enhancing its overall profitability. The adverse impact of escalating rates on the company’s financial performance is evident in the substantial 45% year-over-year increase in interest expenses in Fiscal 2023, reaching $580 million. Considering that Walgreens’ total debt stood at $34.5 billion at the close of Fiscal 2023, expediting efforts to deleverage emerges as a prudent move.

In such a scenario, there is a potential for a resurgence in Walgreens’ profitability, unveiling the undervalued nature of its stock. How? Well, management anticipates the adjusted EPS for Fiscal 2024 to fall between $3.20 and $3.50. This projection aligns with Wall Street’s consensus estimate of $3.34 for the year. Although this implies a decline compared to the previous year’s adjusted EPS of $3.98, analysts anticipate a gradual rebound from this point onward.

Considering the current valuation of approximately 6.3 times next year’s projected adjusted EPS, a dividend cut catalyzing a positive earnings growth trajectory is likely to expose the stock’s undervaluation, presenting significant upside potential for investors.

Is WBA Stock a Buy, According to Analysts?

Regarding Wall Street’s view on the stock, Walgreens Boots Alliance maintains a Hold consensus rating based on two Buys, six Holds, and one Sell assigned in the past three months. At $26.56, the average Walgreens stock forecast implies 28.37% upside potential.

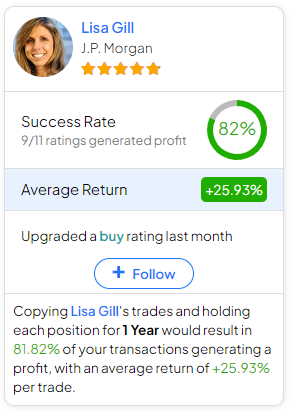

If you’re wondering which analyst you should follow if you want to buy and sell WBA stock, the most accurate analyst covering the stock (on a one-year timeframe) is Lisa Gill from JPMorgan (NYSE:JPM), with an average return of 25.93% per rating and an 82% success rate.

The Takeaway

Walgreens Boots Alliance is at a crossroads, with its dividend yield near an all-time high and a historic 47-year growth streak under threat. Wall Street’s foresight on a potential dividend cut seems well-founded, given the persistent decline in adjusted EPS since 2018. However, this doesn’t necessarily make me bearish on the stock.

While a dividend cut may disappoint income-focused investors, it could serve as a strategic move to enhance overall profitability and address the company’s mounting financial challenges. This, in turn, might unlock substantial upside potential for the stock, presenting a decent opportunity for investors. Thus, I remain neutral on the stock.