Market conditions these days are best described as ‘unsettled.’ Inflation was lower in the October print, but remains stubbornly high, while the Fed’s reactive interest rate policy is pushing up the price of capital, but has not yet constricted retail or other purchasing activity – or inflation. Other headwinds include continued bottlenecks in global supply chains, made worse by recurring COVID lockdown policies in China, and the ongoing Russian war in Ukraine.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

So, should investors stick to a defensive approach? Not according to Ari Wald, head of technical analysis at Oppenheimer. Wald believes investors should forego the obvious defensive strategy and move toward offensive stocks.

“As momentum investors, we’re aware that offensive stocks with low-momentum scores, in this case growth stocks, are likely to be bid higher when the final market breakaway develops. This leads us to think the bigger risk to our portfolio is that our exposure isn’t bullish enough. We believe owning relatively strong stocks, those that fit our discipline, in low-momentum industries should help balance this risk,” Wald explained.

So, bullish enough or not, that is the question. Oppenheimer’s top stock analysts are taking out solidly bullish positions on three interesting stocks, predicting double-digit upside potential despite the difficult economic indicators. We ran these names through TipRanks’ database to see what other Wall Street’s analysts have to say about them. Let’s take a closer look.

Shoals Technologies (SHLS)

We’ll start with Shoals Technologies, a company focused on electrical balance of systems (EBOS). These are vital components for solar energy products; the combiner boxes, junction boxes, splice boxes, in-line fuses, racking, PV wire, cable assemblies, recombiners, and wireless monitoring systems that make it possible to set up and connect solar power installations. Shoals has 20 patents in this technology, and over 40 gigawatts of power in construction, under contract, or operating, making the company the world’s largest EBOS supplier.

The combination of social and political impetus pushing forward on solar power has also pushed Shoals to record revenue levels. The company reported a 52% year-over-year increase at the top line in 3Q22, to $90.8 million. This was driven by an 80% y/y gain in systems solutions revenue, which hit $69.5 billion and made up 77% of the total top line.

Earnings also hit a record high in the third quarter. Adjusted net income came in at $16.6 million, up 43% from the year-ago period, and the adjusted EPS came in at 10 cents per diluted share – up 42% from the 7-cent figure reported in 3Q21. The company’s high revenues and earnings found support from a solid line-up of backlogged and awarded orders, which represent future work commitments. These categories together were up 74% y/y, at a record level of $471.2 million.

Among the fans is Oppenheimer’s Colin Rusch, who is impressed by Shoals’ ability to execute on revenues. The 5-star analyst writes: “With SHLS posting strong numbers across the board including award and bookings growth of $144M in the quarter, we believe investors will be increasingly confident in SHLS’ growth trajectory. We believe the value of shortened construction timelines and skilled labor savings are driving outsized growth, supplementing a strong demand environment of solar where higher electricity prices are outpacing costs from inflation and increased interest rates.”

“We expect bookings/awards to accelerate through year-end into 2023 as a larger volume of customers get familiar with those products. We remain bullish on SHLS shares,” Rusch summed up.

Putting these comments into quantifiable terms, Rusch gives SHLS an Outperform (i.e. Buy) rating, and a $41 price target that implies ~35% upside in the coming months. (To watch Rusch’s track record, click here)

Turning to the rest of the Street, opinions are split almost evenly. With 4 Buys, 4 Holds and 1 Sell assigned in the last three months, the word on the Street is that SHLS is a Moderate Buy. (See SHLS stock forecast on TipRanks)

Home Depot, Inc. (HD)

The second Oppenheimer pick is one of retail’s most recognizable names, Home Depot. This company is the world’s leader in the home improvement big-box, or superstore, retail niche, and caters to the DIY crowd, as well as contractors large and small and the ordinary homeowner with a list of small projects.

Earlier this month the company reported solid results for 3Q22. The top line grew 5.6% year-over-year, or $2.1 billion, to reach a total of $38.9 billion. Globally, comps grew 4.3%, while in the US market they were up 4.5%. This performance was achieved despite the pressures of stubbornly high inflation, and despite higher interest rates putting a squeeze on consumers’ credit access.

The positive sales numbers found support from do-it-yourselfers, as well as professional builders and contractors. Professional customers, according to HD sources, reported solid backlogs supporting their business purchases.

Along with increased revenues, Home Depot saw increased earnings. Net income grew year-over-year from $4.1 billion to $4.3 billion; on a per-share basis, the increase was 8%, from $3.92 per diluted share to $4.24.

Along with the quarterly results, Home Depot also announced its latest dividend payment, for 3Q, at $1.90 per common share. This payment is scheduled for release on December 15, and will mark the fourth payment at this level. With an annualized rate of $1.90, the dividend yields 2.4%, slightly above the market average. Home Depot has maintained a reliable dividend payout going back to 1987.

Oppenheimer’s Brian Nagel, a 5-star analyst and an expert on the home improvement retail sector, is sanguine on the company’s outlook, given its leading position in the niche.

“We look upon indications of persistent sales and profit strength at HD as a testament to the operational prowess of the company and positioning of Home Depot within the still vibrant home improvement marketplace… In our view, any economic weakening is increasingly likely to prove short-lived and shallow and give way to continued, structurally solid backdrop for HD and the home improvement space, anchored to favorable demographic trends, aging housing stock, and underlying healthy consumer dynamics,” Nagel opined.

In line with this view of HD’s underlying strength, Nagel rates the stock an Outperform (i.e. Buy), with a $470 price target implying a 12-month upside of ~45%. (To watch Nagel’s track record, click here)

With 20 analyst reviews on record, breaking down to 15 Buys against 5 Holds, Home Depot’s stock gets a Strong Buy from the analyst consensus.(See HD stock forecast on TipRanks)

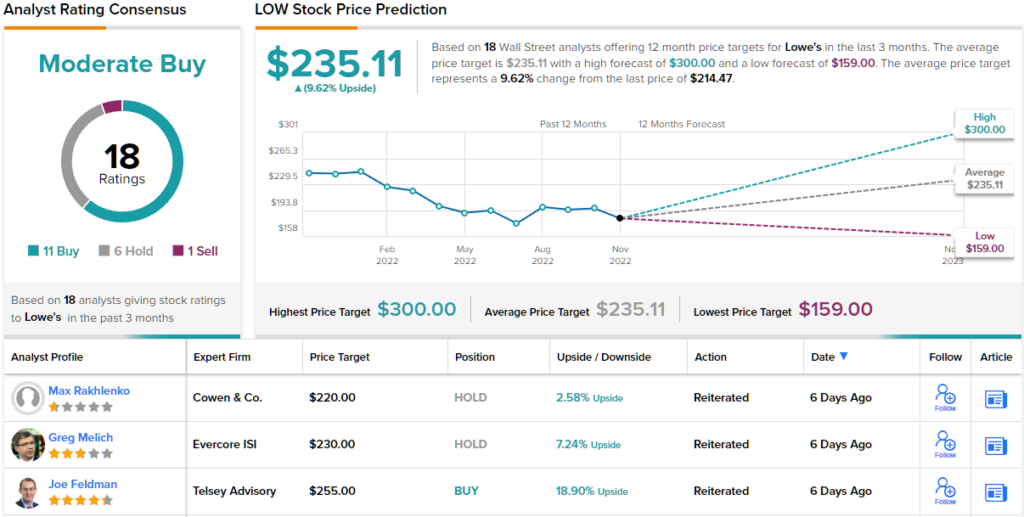

Lowe’s Companies (LOW)

Last but not least is Home Depot’s chief competitor within the big-box home improvement retail space, Lowe’s. Lowe’s is the second-largest company in the home-improvement niche in the US, and in recent year the company has been engaged in a series of steps to improve its retail basics. CEO Marvin Ellison, who took the helm in 2018, engaged in a hands-on approach, focusing on improving customer service, merchandising, and stocking – while also pursuing a series of hard cost-cutting measures including large layoffs and shutdowns of non-performing locations.

In recent years, Lowe’s performance has showed the results of Ellison’s initiatives. The company consistently showed year-over-year growth at both the top and bottom lines. In the most recent quarterly report, for Q3, Lowe’s had revenues of $23.5 billion, up from $22.9 billion in the year-ago quarter, with adjusted diluted EPS of $3.27 – up more than 19% y/y.

Lowe’s also pays out a regular dividend. The most recent declaration is for a payment of $1.05 per common share, to go out on February 8 next year. At that rate, the dividend annualizes to $4.20 and yields 2%, almost exactly the market average. Lowe’s has kept up a reliable dividend history stretching back to 1980.

We’ll check in with industry expert Brian Nagel again, whose stance on Lowe’s is remarkably similar to his stance on HD; clearly, Nagel believes that the home improvement retail space is big enough to support two giants.

“We look very favorably upon recent trends at LOW and believe that the chain’s persistent sales and profit strength and upside reflect management capitalizing well upon a still healthy backdrop for home improvement and significant, internal repositioning efforts that have taken hold over the past few years. As indicated in prior reports, while risks for LOW and the home improvement sector persist, we increasingly look upon market concerns of a forthcoming, meaningful deterioration in trends as overly pessimistic,” Nagel noted.

Going forward, Nagel gives LOW shares an Outperform (i.e. Buy) rating, along with a $300 price target. If the target is achieved, the stock could provide a potential total return of ~40% over the next 12 months.

All in all, Lowe’s has picked up 18 recent analyst reviews; these include 11 Buys, 6 Holds, and 1 Sell, for a Moderate Buy consensus rating. (See LOW stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.