It seems that hedge funds have a love/hate relationship with the biotechnology sector, and it’s easy to see why they are split on the sector. In this piece, we used TipRanks’ Comparison Tool to evaluate two biotech stocks. Vertex Pharmaceuticals (NASDAQ: VRTX) and Sarepta Therapeutics (NASDAQ: SRPT) are two of the biggest players in biotech, but the two couldn’t be more different. While VRTX is a steady, profitable company, SRPT is riskier but may offer a better opportunity.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Taking the Plunge into Biotech

Biotechnology has become a critical part of the healthcare sector. It’s important to understand the difference between biotech and pharmaceuticals. While both develop medicines, those made by biotech firms are derived from living organisms, while those produced by pharmaceutical companies are usually chemically derived.

Additionally, many biotech companies have developed their own platform technologies to speed up the development of new medicines.

After a steady run throughout 2020 and into 2021, the biotech sector has plunged, as evidenced by the SPDR S&P Biotech ETF (XBI). The exchange-traded fund tumbled from its peak of around $175 in February 2021 to about $79 in September 2022.

Year-to-date, the ETF is off about 30% as high-growth sectors fell far out of favor amid the bear market. At one point in 2021, S&P Global (NYSE: SPGI) found that biotech companies were the most-shorted stocks amid concerns about the Biden administration’s increased scrutiny of everything healthcare. One key issue right now is that many biotech companies are unprofitable, and Wall Street has been punishing cash-losing names.

Even though biotech as a whole has sold off, some corners of the market are doing quite well. In fact, Vertex Pharmaceuticals and Sarepta Therapeutics are both up significantly year to date, with Sarepta up 23% and Vertex gaining 32%.

Vertex Pharmaceuticals (VRTX)

As far as valuation, Vertex Pharmaceuticals sits right about where it should be with a P/E of around 23.4x, compared to Bristol-Myers Squibb’s P/E of about 23.3x and Johnson & Johnson’s P/E of about 23.6x. As a result, a neutral position appears appropriate for Vertex at its current valuation, although investors might want to keep an eye on this company in case an attractive entry price appears. There is plenty to like about Vertex, so the only holdup at this time is its valuation.

Vertex Pharmaceuticals is credited with being one of the first biotech companies to use a strategy of rational drug design instead of chemistry. Rational drug design involves designing drugs that bind to a particular target, like a protein. Companies using such a strategy often develop a platform technology that can be used to create multiple drugs.

On its website, Vertex lists six medicines as having been approved and many others that are still in its pipeline. The company is working on treatments for cystic fibrosis, chronic pain, sickle cell disease, Duchenne muscular dystrophy, type 1 diabetes, and several other illnesses, each in different phases of drug trials or research.

Vertex Pharmaceuticals is profitable, reporting product revenues of $2.2 billion with $810 million in net income for the second quarter. It gets most of its sales from Trikafta and Kaftrio, which treat cystic fibrosis. In fact, Vertex has a monopoly on treatment for the disease. Management also boosted its full-year sales guidance to between $8.6 billion and $8.8 billion for 2022.

One key issue for pharmaceutical companies is patent expiries, and Vertex Pharmaceuticals is in a good position for the next several years. Its patents for Orkambi, Kalydeco, and Symdeko expire toward the end of the decade, but the patent for its highly successful cystic fibrosis drug Trikafta doesn’t expire until 2037.

Thus, with a healthy pipeline and several drugs whose patents don’t expire for several years, Vertex is in an excellent position. The company even has a healthy balance sheet with $9.25 billion in cash and equivalents and only $3.65 billion in total liabilities, so what’s not to like?

What is the Price Target for VRTX stock?

Vertex Pharmaceuticals has a Moderate Buy consensus rating based on eight Buys, six Holds, and zero Sell ratings assigned over the last three months. At $299, the average Vertex price target implies upside potential of 3.3%.

Sarepta Therapeutics (SRPT)

Unlike Vertex, Sarepta Therapeutics is unprofitable, which is a firm strike against it in the current climate. However, there’s been significant buying activity among corporate insiders, who have snapped up $11 million worth of shares over the last three months. Thus, for this reason, and others to be explained, a bullish view may be appropriate for Sarepta Therapeutics.

However, investors may want to keep an eye on the company because its lack of profits and sudden surge in its stock price suggests that it could be risky, nonetheless.

Insider buying is generally a bullish sign, and in this case, it came as Sarepta shares surged to over $109 after bottoming out around $63 in mid-June. As a result, insiders seem to feel that the stock must have more room to rise despite its dramatic climb over the last few months.

The company also has a steady balance sheet after raising more cash through the sale of $1 billion in convertible senior notes. Sarepta has $1.93 billion in cash and equivalents and $2.27 billion in total liabilities. The company’s ability to access the capital markets as the cost of capital is increasing speaks to its strength.

The biotech firm trades at a price-to-sales ratio of around 11.6x, firmly below its peaks between 33x and 27x in 2020 and 2021, respectively. One thing that makes Sarepta so much more attractive than other unprofitable biotech firms is that it isn’t pre-revenue. The company does have sales, albeit not enough to keep it from losing money each quarter.

Sarepta currently has three FDA-approved therapies for Duchenne muscular dystrophy patients with specific genetic mutations. Given how rare DMD is, the market for these treatments is quite small. However, Sarepta also has a pipeline with more than 40 additional programs, which is essential because the patent for one of its approved drugs is due to expire in 2025.

For the second quarter, the company reported $233.5 million in total revenues, which includes collaboration revenues and $211.2 million in net product revenues, a 49% year-over-year increase. Sarepta’s net loss amounted to $231.5 million.

A key question for investors is when the company will become profitable, and that milestone might not be too far away. The analyst consensus suggests that Sarepta will become profitable in 2024, although, as is always the case with risky stocks, estimates could be dead wrong.

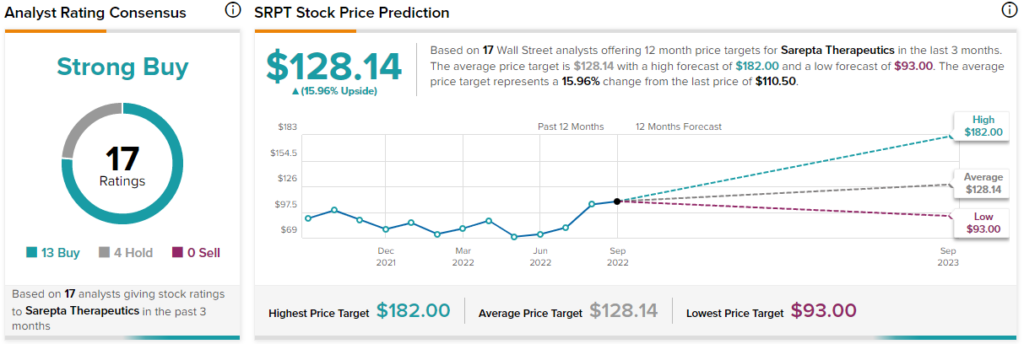

What is the Price Target for SRPT Stock?

Sarepta Therapeutics has a Strong Buy consensus rating based on 13 Buys, four Holds, and zero Sell ratings assigned over the last three months. At $128.14, the average Sarepta Therapeutics price target implies upside potential of 16%.

Conclusion: SRPT May Offer a Better Risk/Reward Opportunity

It’s important to realize that great risk brings the possibility of great reward, although there is also a chance of significant loss. As things stand now, Sarepta Therapeutics appears to have a bright future, but its lack of profitability presents a precarious position for investors. As a result, those with enough appetite for the high level of risk involved could find Sarepta to be a good addition to their portfolio, making a bullish view appropriate for them.

On the other hand, Vertex Pharmaceuticals looks far steadier, but its valuation should give pause, at least for now. If or when the market re-rates and biotech multiples rise, Vertex will likely become a Buy, given its stability, which is rare in the biotech market.