Visa (NYSE:V) will post its Q4 results after next Tuesday’s (October 24) closing bell. Operating within a dynamic trading landscape, the global payment processing giant faces the forces of inflation, interest rates, and consumer spending that can sway its results either way. With that in mind, let’s delve into the key points to look for in Visa’s forthcoming report, a release that I view with great optimism. In light of this perspective, I continue to maintain a bullish outlook on Visa stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Will Macroeconomic Headwinds Impact Payment Volumes?

Visa’s performance intricately hinges on the payment volumes it handles. In light of the challenging macroeconomic landscape that the company is currently navigating, the paramount focal point in its upcoming Q4 report should undeniably be this crucial metric.

Despite persistent challenges, I believe that Visa is poised to post robust payment volumes. Remarkably, the company has consistently achieved this feat over the past four years, demonstrating resilience in the face of adversities. In the aftermath of the COVID-19 pandemic, the global landscape has been marred by tumultuous macroeconomic conditions, including surging inflation, sharp interest rate hikes, and an increasingly precarious geopolitical environment. Still, Visa has maintained resilient payment volumes.

How? Well, the company’s performance is being boosted by vigorous consumer spending and favorable tailwinds, notably from a thriving travel industry that plays a pivotal role in enhancing its cross-border processing capabilities. In its latest Q3 report, the company showcased 9% growth in global payments volume. When benchmarked against the pre-pandemic year of 2019, global payments volume exhibited a substantial surge of 48%.

Regarding the travel sector’s positive influence, year-over-year growth in cross-border travel-related spending (excluding intra-Europe transactions) reached an impressive 34%. Furthermore, the cross-border travel index, excluding intra-Europe and referencing data from four years ago, saw a notable increase from 134 in March to 139 in June. Asia also posted strong numbers.

Given Visa’s resilience recently, as well as the fact that the macro landscape has not worsened since then, it makes sense to expect another strong report in payments volumes in Q4. This expectation is bolstered by the positive signals in recent data, such as September’s retail sales figures, which underscore the continued strength of consumer spending in the face of rate hikes. The same indication is also supported by the consistently low unemployment rate, which currently stands at a healthy 3.8%.

What Does Wall Street Expect to See in Visa’s Q4 Report?

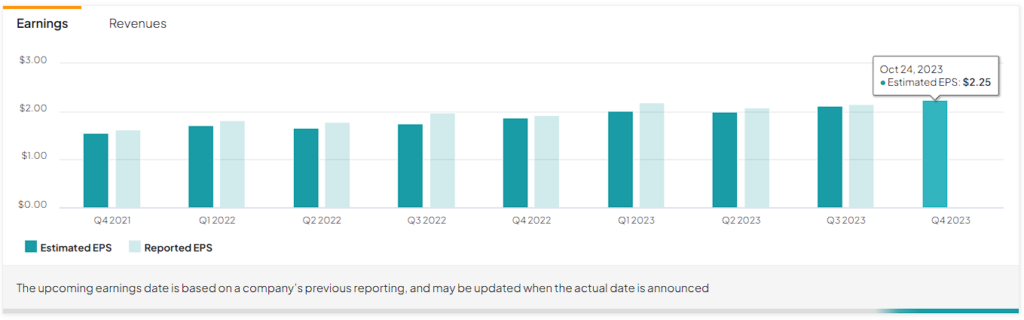

Wall Street analysts seem to be optimistic about Visa’s processing volumes in its upcoming Q4 report, too. Evidently, consensus estimates point toward revenue growth of 9.9% to $8.56 billion. Visa’s EPS is also expected to land at about $2.25, implying a strong increase of 16.3%. The stronger expected rise in EPS against revenues can be attributed to higher margins due to Visa’s royalty-type business model and buybacks.

Note that Visa’s results are likely to come out even stronger, as the company has a strong track record of beating both Wall Street’s top and bottom line estimates over the years. Impressively, Visa has beaten consensus revenue estimates in 14 out of the past 16 quarters. It has also beaten Wall Street’s EPS estimates in 15 out of the past 16 quarters.

Don’t Forget That the Valuation Matters

Regardless of Visa’s Q4 performance and its alignment with Wall Street estimates, it’s crucial to stay mindful of the stock’s valuation. Despite challenges faced by other tech companies in recent quarters, Visa’s shares continue to maintain a premium, reflecting its remarkable resilience. Currently, shares are trading at a forward P/E of 25.5, roughly in line with its decade-long average. This is despite the fact that interest rates are currently at their highest levels during this period.

Is V Stock a Buy, According to Analysts?

Regarding Wall Street’s view on the stock, Visa features a Strong Buy consensus rating based on 20 Buys and four Holds assigned in the past three months. At $278.70, the average Visa stock forecast implies 19.2% upside potential.

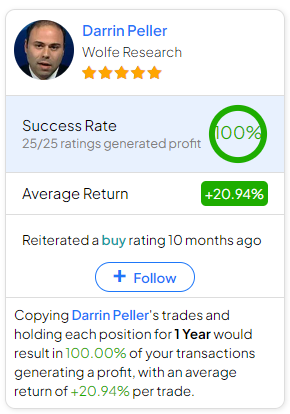

If you’re wondering which analyst you should follow if you want to buy and sell Visa stock, the most accurate analyst covering the stock (on a one-year timeframe) is Darrin Peller from Wolfe Research, boasting an average return of 20.94% per rating and a 100% success rate.

Conclusion

In conclusion, as Visa gears up to unveil its Q4 results, the spotlight rests on its ability to navigate a complex economic landscape. The company’s remarkable strength, evident in its sustained payment volume growth despite macroeconomic headwinds, positions it optimistically. Moreover, the positive trajectory fueled by consumer spending and a thriving travel industry bodes well for another robust report.

Wall Street’s bullish expectations align with Visa’s history of consistently surpassing estimates. However, I believe that prudent investors should remain mindful of the stock’s valuation, recognizing the premium it holds despite the recent interest rate hikes.