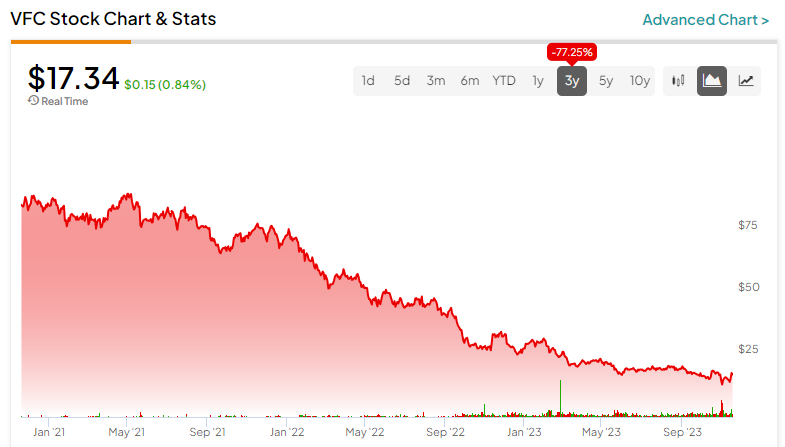

Shares of apparel company VF Corp. (NYSE:VFC) have been in free-fall for more than two years now, with shares now off more than 82% from their pre-pandemic all-time high, just shy of $100 per share. The stock has been battered severely, but negative momentum has slowed in recent months, potentially signaling that the firm has finally hit rock bottom.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

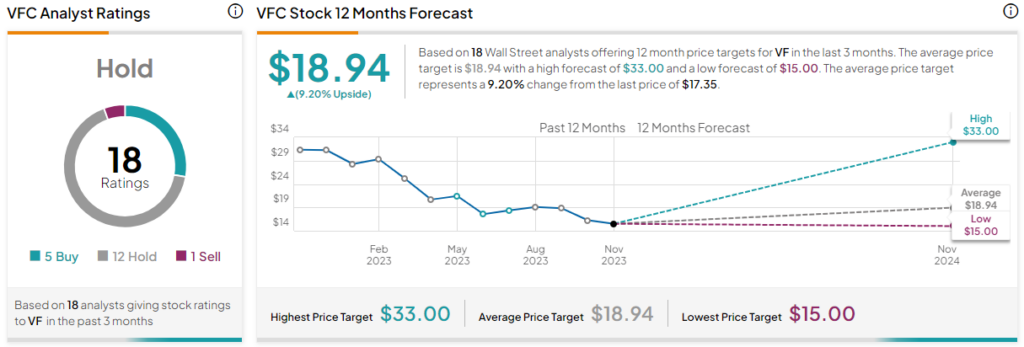

However, just because the worst is in the rear-view mirror does not mean the stock’s ready to roar higher again. Though expectations have been lowered, the company still faces stiff challenges in this less-than-ideal consumer environment. For now, most of Wall Street views VFC stock as a Hold.

Still, while it may be the safer move to take on a wait-and-see approach, I believe there’s a lot to gain by getting in before the herd has a chance to turn bullish. So, from a long-term perspective, I can’t help but be bullish on VFC stock as it hovers around multi-year depths. Nonetheless, I acknowledge that bottom-fishing for such a name could lead to more pain in the near term.

Indeed, the company behind brands like The North Face may not have much going for it these days. That said, even such a severely distressed firm can be a buy in the face of economic weakness if the price of admission is depressed enough.

Though I have no idea if a bottom is in or near, the risk/reward looks intriguing, with shares going for just 0.61 times price-to-sales (P/S) at the time of writing. That’s below the apparel manufacturing industry average of 0.8 times.

Too Much Negativity after a Rough Second Quarter

Undoubtedly, VFC stock deserves to trade at a discount to the peer group, especially following its second-quarter miss that was accompanied by a guidance cut for Fiscal Year 2024. That said, there is hope for the company should consumer trends shift drastically in the new year. With a lower bar ahead of it, it’s arguably a better idea to go against the herd with a contrarian position.

At the end of the day, VF Corp. sells durable discretionary goods that won’t sell well when the consumer is in a bad place. Once economic tides turn, though, it’s not hard to imagine a pick-up in demand for things like Vans sneakers or North Face jackets as consumers save enough to justify buying a new jacket or pair of kicks.

In the latest quarter, it was revealed that people are buying North Face products (sales rose 19%) but not Vans (sales sagged 21%). The lumpiness in performance across banners isn’t doing the stock many favors. Still, I think the strength of The North Face shouldn’t be ignored as consumers heal and the weather gets chillier.

VFC Stock Gets a Big Upgrade on Wall Street

More recently, things have been looking up for VFC stock. Last week, VFC stock soared 14% on the back of an upgrade (to Hold from Sell), courtesy of JPMorgan (NYSE:JPM) analyst Matthew Boss.

Though Mr. Boss isn’t exactly bullish on the firm, he expects a “profit inflection point” in 12-18 months, thanks partly to the company’s cost-savings program. I’m inclined to agree with Mr. Boss. Though VFC stock may not be the timeliest of battered value plays, it certainly has the means to turn a corner, even without too much help from the broader economy.

Sure, a drastic turn in consumer spending would help. However, the company has the means to repair margins, even if conditions stay hostile for longer. With a bit of pressure from activist investors like Engaged Capital, which has a stake in the firm, the company may have the catalyst it needs to shake things up. When it comes to battered companies, I view activist involvement as a good thing. Sometimes, it takes an outsider to push for changes drastic enough to be transformational.

Is VFC Stock a Buy, According to Analysts?

On TipRanks, VFC stock comes in as a Hold. Out of 18 analyst ratings, there are five Buys, 12 Holds, and one Sell recommendation. The average VFC stock price target is $18.94, implying upside potential of 9.2%. Analyst price targets range from a low of $15.00 per share to a high of $33.00 per share.

The Bottom Line on VF Corp.

There are no easy solutions for VF Corp. as consumers speak with their wallets. Nevertheless, with a depressed multiple, little in the way of expectations, and activists pushing for change, I’d be more than willing to give VFC stock the benefit of the doubt. It’s just way too cheap, given the timeless brands in its portfolio. Plus, the macro environment should improve with time. Until then, look for major changes to help improve the firm’s ability to weather the storm.