Shares of fallen telecom titan Verizon (NYSE: VZ) have been tumbling endlessly this year. As a result, dividend-seeking bargain hunters should take notice of the name, as its dividend yield looks to break the 7% mark. Though Verizon has lost its competitive edge in the wireless scene to some pretty tough rivals, it’s hard to pass on the underdog at these depths for those who seek to stretch every investment dollar as far as it can go.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

It’s hard to believe that Verizon stock has fallen to a 12-year low. At just 8.2 times trailing earnings, shares of Verizon may very well be one of the best bargains this market has to offer. That said, Verizon has a slate of issues that will not be easy to cure as we head into a potential economic downturn.

It’s hard to tell when the telecom market will form a new equilibrium. It’s probably not going to be anytime soon, given the 5G race is still nowhere close to the finish line. Given the aggression of Verizon’s peers, the fallen telecom titan can’t afford to play a passive defense. It needs to one-up its rivals to win back share and drag its stock out of its multi-year rut.

It’s never easy to bet on an underdog that’s been bettered by its rivals. Still, I remain bullish on the stock. The valuation (and expectation) is just so incredibly depressed, with a bountiful payout that’s still on relatively solid ground.

Recession and Competitive Pressures Weigh on Verizon Stock

As macro headwinds mount while industry competitors become more aggressive, Verizon stock seems more like a value trap than any sort of market bargain. With such negative momentum behind the stock, a lack of medium-term catalysts, and underwhelming subscriber metrics, it’s not a mystery as to why Warren Buffett may have parted ways with the stock.

It’s been open season for Verizon’s telecom rivals over the past year. That said, I don’t expect the company will stand around like a sitting duck, as its rivals have their way.

It won’t be easy to stand up to aggressive peers without sacrificing a further slice of margin. Verizon will need to continue putting its foot on the gas in terms of capital expenditures to catch up to the likes of T-Mobile (NASDAQ: TMUS) in the race for 5G supremacy.

Further, AT&T (NYSE: T) has gone from an industry laggard weighed down by diseconomies of scale to a wireless juggernaut that could continue to outpace Verizon. Thanks to a spin-off, AT&T is lean, and it’s sure to be mean as it tackles Verizon and T-Mobile. In the third quarter, AT&T brought on 708,000 postpaid phone subscribers versus just 8,000 for Verizon.

Verizon may be having a tough time playing defense against two bitter rivals that are flooring it on wireless growth. Regardless, I think Verizon can reignite subscriber growth if it’s willing to take a hit right to the margin to offer customers a better value proposition in a recession year.

Verizon Stock: Costly Plans Have Subscribers Jumping Ship

Verizon’s pricier plans were supposed to give profits a jolt. Instead, the firm may have shot itself in the foot, with subscribers jumping ship to competitors in search of a better value. With a recession up ahead, consumers will likely continue pursuing the cheapest option. Verizon may have a top-notch wireless network, but that’s no longer enough to command pricing power in the face of an inflationary economic downturn.

Recently, the firm noted it lost 189,000 worth of monthly phone subscribers, thanks in part to recent pricing changes. Perhaps Verizon overestimated its inflation resilience.

If Verizon is to turn the tide, it may have no option but to trim prices and bolster promotions. In a rising-rate environment, any resulting profitability prospects will surely be met with distaste.

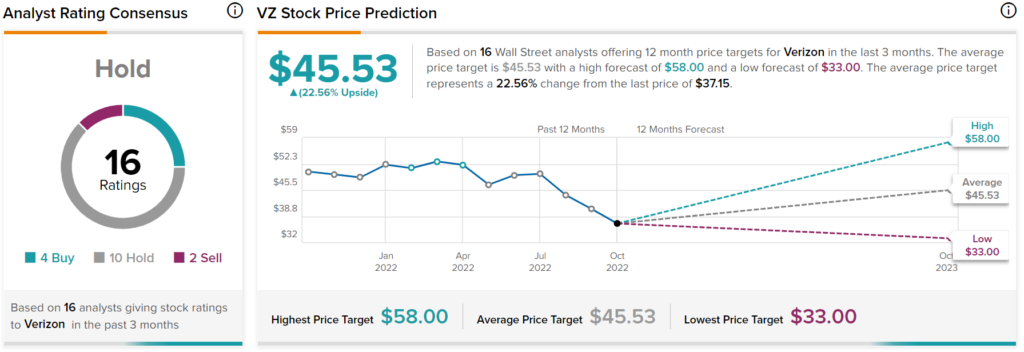

What is VZ Stock’s Price Target?

Turning to Wall Street, VZ stock has a Hold consensus rating based on four Buys, 10 Holds, and two Sells assigned in the past three months. The average Verizon stock price target is $45.53, implying 22.56% upside potential. Analyst price targets range from a low of $33 per share to a high of $58 per share.

Conclusion: Verizon Stock’s Valuation is Difficult to Ignore

Verizon stock is between a rock and a hard place as it heads into a recession without an answer to its hungry competitors. Even without a plan to one-up its rivals, it’s hard to overlook the dividend and rock-bottom price tag on shares. The nearly 7% dividend yield and 0.35 beta look compelling for investors looking to dampen market-wide fluctuations.