2023 has been a good year for growth stocks, which shone as the economy proved to be more resilient than was expected, while the obsession with all things AI injected optimism into the markets. However, looking ahead, this might be a good time to incorporate some value into the portfolio. Value stocks are trading at a 50% discount to their fair value, and the economic outlook provides ample reasons for them to regain their posture.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Tech Tide Lifted Growth Boats

This year, in stark contrast to 2022, was the year of growth stocks – companies which are expected to grow their revenues or earnings at a faster clip than the market average, leading to fast stock price appreciation. Most of the companies in this category are technology and biotech firms, which generally hold the high level of debt needed to finance fast growth. Naturally, growth investors are willing to pay higher prices for stocks that promise outsized price gains; they also accept these stocks’ high volatility as a part of the overall “growth package.”

After a dismal 2022, expectations were for a recession that would push the Fed’s hand to start cutting rates soon. As the bulk of the growth companies’ profits are future earnings, they are less impacted by the current economic conditions than by interest rates. Thus, the expectations at the beginning of the year created a winning environment for growth, which was also mightily helped by the exuberance of artificial intelligence (AI) technology. Meanwhile, value stocks – solid, stable companies whose stocks are selling below their intrinsic value – were all but forgotten.

The wide disparity between the performances of growth and value this year can be illustrated by moves in ETFs based on these two styles: Vanguard Value Index Fund ETF (VTV), which has declined 2% so far this year, and Vanguard Growth Index Fund ETF (VUG), up almost 36% year-to-date.

Source: Google Finance

Stunted Growth Gives Way to Value

U.S. stocks have had a pretty good year so far, despite higher rates and the prevalent pessimism about the economic prospects, as markets were spurred by the resilience of the U.S. job markets and consumers, as well as by stronger-than-expected corporate profits and hope that these profits will be further lifted by the artificial intelligence. The companies that have led the market’s gains are now trading at forbidding valuations; outside of these stocks, valuations are largely reasonable.

As we have progressed through the year, the picture has shifted from an impending disaster to lower, but still robust, economic growth, leaving little chance for rate cuts anytime soon, especially given much lower than in 2022 but still persistent inflation pressures. Moreover, there’s now a widespread recognition that the higher rates are here to stay for longer than previously thought. In addition, the initial AI craze has subsided, as the fact that the technology, albeit truly revolutionary and life-changing, will have most of its effects further in the future, has dawned on the markets.

It looks like, at least for a while, we are entering a world with high interest rates and modest economic growth – nothing disastrous, but not very exciting, to say the least. The absence of a “tide lifting all boats,” i.e., a strong rally catalyst, suggests that stock market investors may want to reassess their exposure to different economic styles, employing a more discriminative approach and putting some more emphasis on valuations.

Namely, as we are approaching 2024, it may be a great time to access value stocks. Thus, JPMorgan’s (JPM) analysts see a lot of opportunities among the value cohort. JPM believes that inflation will come down to a 2% Fed target by the end of 2024, and the resurgence in economic optimism will first reward the lower-valued stocks that have more room to rise.

Taking Turns at the Fore

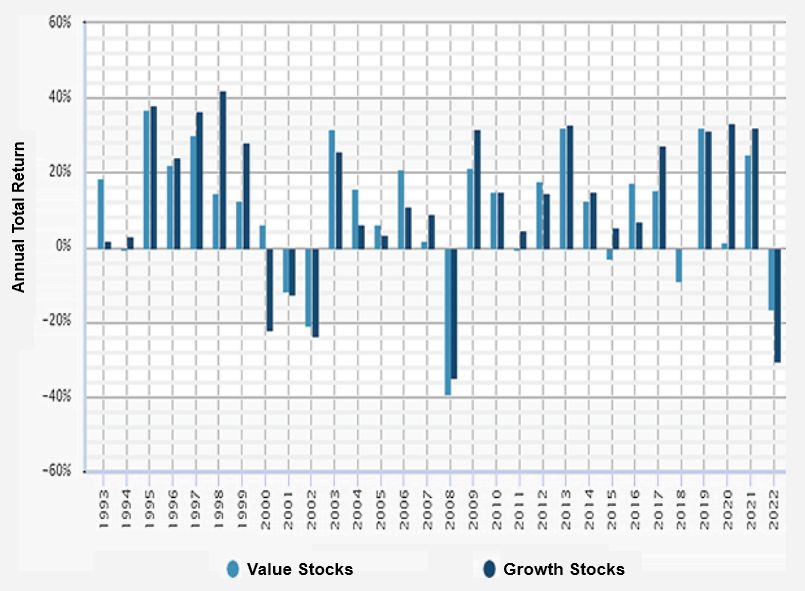

Growth stocks have generally reigned supreme in the period since the Global Financial Crisis (GFC), fueled by an extra-low interest rate environment, although within this time frame, there were several periods of value outperformance. Before the GFC, the style performance picture was almost symmetrically opposite.

Source: Bank of America

Some studies have shown that over the long term, value investing has outperformed growth when taking into account the compounding dividends, which growth companies usually lack. Value companies are usually found among larger, more established companies, which offer larger shareholder compensation for lower capital growth from stock price appreciation. On the other hand, growth stocks offer higher potential rewards for the much greater risk associated with growth investing, as well as for their much greater volatility, on average.

Historically, growth stocks beat the value at times of falling or low interest rates, as they need cheap money to fuel fast growth. Growth also usually excels during bull markets and periods of economic expansion; on the other hand, they usually suffer the most when the economy is in a downturn and market sentiment turns sour. However, when the economy is already in a recession, growth may at times win over value, albeit the actual performance varies between sectors and depends, among other factors, on each company’s characteristics.

Conversely, value stocks tend to outperform in the early stages of the economic recovery, as they tend to have healthier fundamentals, allowing them to come out of a recession with much lesser damage. In many cases of bear markets or significant corrections, value stocks declined much less than growth, with the latter one’s underperformance stemming from the aggressive repricing of previously overvalued stocks. Value also usually shines in a higher inflation environment, simply because it includes many companies providing bare necessities, such as banking, utilities, and consumer basics.

Having established that different investment styles take the lead at different times, it looks prudent for investors to include value stocks in their portfolios, along with growth. Incorporation of value stocks into the portfolios may especially benefit long-term investors, according to Vanguard Financial Advisor Services’ research, as “deviations from fair value and future relative returns share an inverse and statistically significant relationship over five- and 10-year periods.” Vanguard said (in September 2023) that value stocks were trading at an average discount of 50% to their fair value estimates, which gives them more-than-significant room for a bounce back to the mean.

Beware the Traps

Since we exited the joyous period of the “everything rally” of the 2010s, building a winning investment portfolio isn’t an easy task, necessitating discerning analysis of company fundamentals and sector prospects in different economic scenarios.

This is also true regarding value investments. Although by definition, value stocks are the market’s “sale items,” there are more factors to consider than just the low price, since “value stocks” don’t equal “cheap stocks”.

Value investing focuses on calculating a company’s intrinsic value, based on fundamentals, and finding stocks that trade below that value. That can happen for a number of reasons, such as short-term mispricing, information gaps, sector volatility, market overreaction to negatives that don’t hamper the company’s quality, and others. These factors can push stock prices to low levels, creating buying opportunities for value investors: when the markets realize their true value, they will bounce back.

However, while the market doesn’t always efficiently price stocks in the short term, in many cases the price label it slaps on a company is correct. The low stock price can at times reflect real trouble, such as unmanageable debt levels, poor management, a history of earnings disappointments, a lack of revenue growth catalysts, etc.

Thus, low valuations may point at a “diamond in the rough,” or, conversely, at a value trap – a situation when a stock’s price never recovers from its low level or even falls further. Falling into a value trap can happen to bargain-seeking investors who are attracted to stocks trading cheaply relative to their historical pricing or to the sector’s average while disregarding the company’s fundamentals, competitive dynamics, and other important factors.

To avoid value traps, an aspiring value investor needs to establish the company’s intrinsic value by determining the present value of a company’s future cash flows, but it doesn’t end there. In addition, research beyond the financial ratios, reviewing the company’s competitiveness, industry outlook, growth prospects and risks, and more, is essential. Alternatively, investors can leverage the existing analysis, utilizing research done by Wall Street’s leading analysts: