Conventional wisdom dictates that a US recession is imminent, either during the second half of this year or the first half of the next. But just how much should we credit that? While there are economic headwinds in play, we should also remember that the pace of inflation is easing, unemployment remains low, and the second quarter earnings season showed a high proportion of surprises to the upside.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

If it’s not a completely rosy picture, it’s far from doom and gloom. And in the eyes of Goldman Sachs equity strategist David Kostin, it’s a sign that the US may be ready for a rebound.

Laying out his case, Kostin writes, “Resilient US economic growth, which is the primary variable in our sales model, should support S&P 500 revenue growth in 2023. Goldman Sachs economists forecast 2.1% real US GDP growth in 2023 compared with the consensus estimate of 1.6% growth, which partly explains our above-consensus sales growth forecast. Our economists assign just a 20% probability that the US economy enters a recession during the next 12 months, compared to the median forecaster’s 54% probability.”

Riding on this positive sentiment of growth potential, the Goldman Sachs analysts have been upgrading the ratings for several stocks recently. Here are the details on two of their picks, drawn from the TipRanks platform, along with the analysts’ comments.

Teledyne Technologies (TDY)

The first company we’ll look at is Teledyne, an engineering firm involved in the creation and production of enabling technologies for industrial growth markets. The company produces a wide range of products, including digital imaging sensors, broad-spectrum camera systems, monitoring and control instrumentation, aircraft information management systems, and electronic and satellite communication systems.

The company operates in four divisions – instrumentation, digital imaging, engineered systems, and aerospace & defense electronics – and its product lines have found their way into a multitude of applications. Teledyne is based in California, but also has operations in Canada, the UK, and Western Europe and boasts a market cap of ~$19 billion.

The firm’s strong position as a leader in high-tech hardware has led to a solid revenue stream – for the past couple of years, Teledyne consistently brought in north of $1.3 billion in quarterly revenue. The company’s last report, for 2Q23, showed a top line of $1.42 billion, 5.1% better than the year-ago quarter and $11.43 million higher than the pre-release estimates. The company’s bottom line earnings figure, reported as a non-GAAP diluted EPS of $4.67, was 2 cents above expectations and compared favorably to the $4.43 reported the year before. Teledyne reiterated its full-year non-GAAP earnings outlook, predicting an EPS of $19 to $19.20 for 2023.

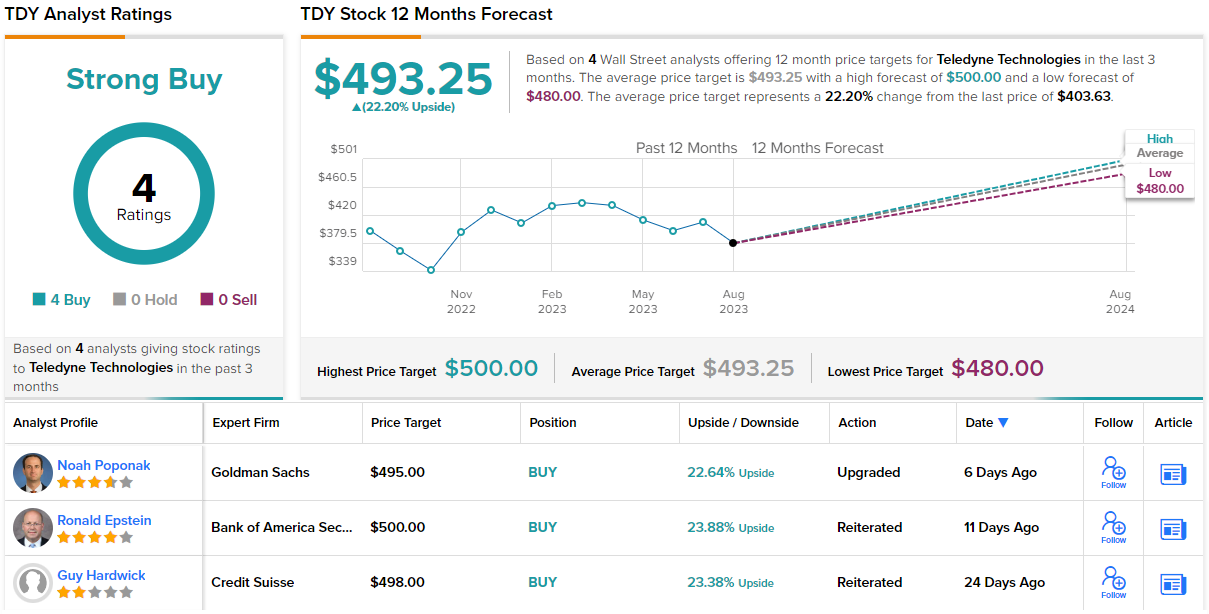

The last 6 months, however, have not been great for the stock, which has seen an 8% decline. Goldman analyst Noah Poponak puts the pullback down to “concerns about the long-term profit margin level” in the company’s Digital Imaging segment. However, pointing out the overall quality of the company and its strong fundamentals, alongside a relatively depressed share price, Poponak sees plenty to like here.

“TDY is one of the highest quality, most consistent, best managed companies we cover that compounds cash flow over time,” Poponak explained. “The stock has pulled back recently to relative valuation lows, just as the balance sheet is nearing full force again for further deployment post FLIR integration, while the core organic fundamental picture remains strong. We see upside to consensus earnings expectations and find current valuation attractive.”

Accordingly, Poponak has boosted his rating from Neutral to Buy and sets a $495 price target, implying a potential upside of 23% for the year ahead. (To watch Poponak’s track record, click here)

There’s a general agreement on Wall Street that Teledyne is a quality stock, as shown by the unanimity of the 4 recent analyst reviews – leading to a Strong Buy consensus rating. The stock’s $403.63 trading price and $493.25 average price target combine to indicate room for 22% share appreciation in the next 12 months. (See Teledyne stock forecast)

Okta, Inc. (OKTA)

Next up is Okta, a cloud-based software company focused on user authentication and identity control. Okta offers a product line based on its Identity Cloud, and the company’s platform can be used for both customer and workforce identity verification. The cloud products allow users to secure their systems, to ensure that customer information is kept secure and that system access by employees, contractors, and partners is in-line with security protocols.

Okta bills its platform as ‘extensible, easy-to-use, and neutral,’ and boasts that it can be easily integrated into customers’ existing solutions, so that users can choose the best technology for their needs. The company has seen more than 7,000 integrations of its software, and claims a customer base more than 18,000 strong.

The cybersecurity industry, where Okta dwells, was estimated at $202 billion last year, and is expected to reach $425 billion by 2030. This makes it a huge growth industry, with a massive addressable market and plenty of room for a savvy company to expand. Okta is showing that it is equal to the opportunity.

At the end of calendar year 2022, Okta switched from posting net losses to posting net gains. In its last financial results – for the first quarter of fiscal year 2024, released at the end of May – Okta showed a top line of $518 million in revenue, more than $7.4 million above the forecast and up 24% y/y. The company’s earnings, reported as a bottom line of 22 cents per share by non-GAAP measures, was 10 cents better than expected – and a strong turnaround from the 27-cent net EPS loss reported one year earlier. The solid results were supported by $503 million in subscription revenue, a forward-looking metric, that was up 26% y/y.

In anticipation of reaccelerated growth, Goldman Sachs analyst Gabriela Borges gives OKTA a rare double upgrade, from Sell to Buy, in her recent note on the company. Pointing out several reasons why Okta is likely to deliver strong growth ahead, Borges wrote, “We see a path to 12m outperformance driven by cRPO and ARR acceleration back to 15%-20% as 1) Okta anniversaries headwinds in its Customer IAM business tied to the merging of its organic and acquired product portfolios (supported by our bottom-up segment model); 2) The Workforce segment stabilizes post go to market changes and a headwind from macro; 3) Okta ramps on cross-sell tied to new product cycles such as IGA (Identity Governance and Administration) and PAM (Privileged Access Management).”

Borges also explains why Okta holds a good position to maintain growth in the face of larger competitors, saying of the company, “While we believe competition from Microsoft will remain an overhang on the stock, we reflect this in our bull case scenario by continuing to discount Okta’s multiple by ~30% relative to peers. Even with this discount, our updated scenario analysis suggests a 3:1 upside/downside skew based on our FY26 (CY25) estimates.”

Looking ahead, Borges complements her new Buy rating on this stock with a $91 price target suggesting a 27% upside potential on the one-year horizon. (To watch Borges’ track record, click here)

Overall, OKTA shares hold a Moderate Buy consensus rating from the Street, based on 24 recent reviews that include 16 Buys, 7 Holds, and 1 Sell. The stock’s average price target of $93.22 is slightly more bullish than the Goldman view, and implies a 30% upside from the current trading price of $71.73. (See OKTA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.