E-commerce platform MercadoLibre (NASDAQ:MELI) has been among the hottest tech stocks in the past decade, creating significant wealth for shareholders. Since its IPO in August 2007, MELI stock has returned a staggering 6,347%, valuing the company at $69.5 billion by market cap. While shares of MercadoLibre have surged 66% in 2023, the stock is still down 32% from all-time highs, providing a dip-buy opportunity, in my view.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

I remain bullish on MercadoLibre, as it is part of a rapidly expanding addressable market, allowing the company to increase revenue and earnings at an enviable pace in the next few years. Moreover, its widening portfolio of products and services should further diversify its revenue base, push profit margins higher, and act as a flywheel for MELI stock.

An Overview of MercadoLibre

MercadoLibre is an e-commerce marketplace operator based in Latin America. This includes the Mercado Libre Marketplace, which allows businesses and merchants to list merchandise online. There is also Mercado Pago, a financial services platform that facilitates online and offline transactions, providing a mechanism for users to facilitate digital payments.

Additionally, the company offers Mercado Fondo, where users can invest funds deposited in the Pago accounts, while it also has a vertical where MercadoLibre extends loans or credit lines to merchants and consumers.

How Did MercadoLibre Perform in Q3?

MercadoLibre is among Latin America’s fastest-growing companies and has increased its revenue from $2.29 billion in 2019 to $10.54 billion in 2022, indicating a compound annual growth rate of 66.3%. In Q3 2023, it reported revenue of $3.76 billion, higher than the consensus estimate of $3.57 billion. Plus, total payment volume surged 121.2% to $47.3 billion, while gross merchandise volume grew by 59.3% to $11.4 billion in the September quarter.

MercadoLibre has invested heavily over the years to develop its products, allowing it to benefit from accelerated growth and consistent operating margins.

Despite a challenging macro environment, MercadoLibre’s growth in items sold rose by 26% year-over-year in Q3, up from the 18% growth in the second quarter. These stellar growth rates meant MELI increased its revenue by 40% while operating income more than doubled for the fourth consecutive quarter to $685 million, indicating a healthy margin of 18.2%.

MercadoLibre is Latin America’s Amazon

MercadoLibre is quite similar to Amazon (NASDAQ:AMZN), serving millions of customers in Latin America. Like Amazon, MercadoLibre gained massive traction due to its online marketplace, which helped it enter new markets such as advertising, credit, and asset management.

These high-margin businesses allowed MercadoLibre to increase operating income by 131% year-over-year in Q3 while adjusted earnings also tripled to $7.16 per share, ahead of estimates, which stood at $5.86 per share.

Investors quickly noticed the resiliency of MELI’s Credit business, as loan originations grew to $3.64 billion in Q3, up from $2.5 billion in the year-ago period. MercadoLibre is offering more significant loan amounts to businesses while maintaining sustainable delinquency rates.

Its Ad sales also grew by 70% to $200 million in Q3 and may be a key revenue driver for MELI stock in the upcoming decade. For reference, Amazon is currently the third-largest digital ad platform in the world due to the high purchase intent of its user base.

Just like Amazon Prime, MercadoLibre offers Meli+, which includes free shipping of products and subscriptions to streaming platforms, including Disney+.

What Next for MELI Stock?

MercadoLibre ended Q3 with 119.8 million active users and has enough room to keep growing at a rapid clip. According to a Statista report, Latin America’s e-commerce market was forecast to grow by 15.5% annually through 2025 (with 2019 being the starting point) due to rising internet penetration rates and higher income levels.

MercadoLibre’s impressive growth rates have enabled it to consistently report profits, thanks to the benefits of economies of scale. An asset-light business model also suggests that its earnings will grow faster than revenue due to high operating leverage. For example, MELI’s massive scale and increasing brand value could allow the company to lower its marketing expenses over time.

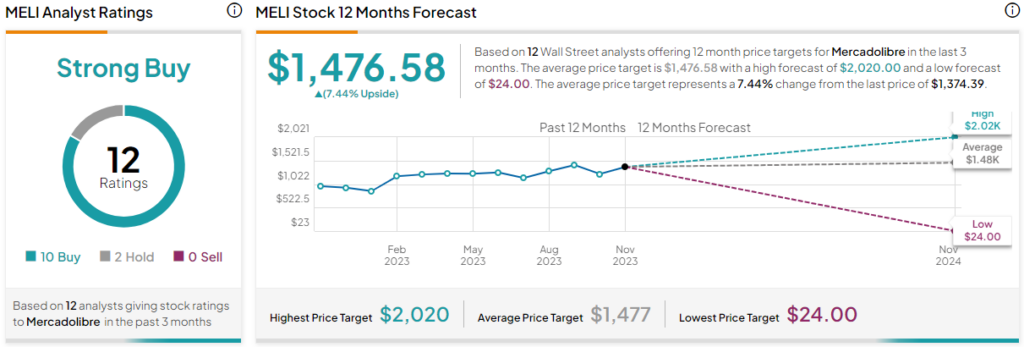

Is MELI Stock a Buy, According to Analysts?

Wall Street remains bullish on MELI stock, giving it a Strong Buy rating. Of the 12 analysts covering MELI stock, 10 recommend a Buy, two recommend a Hold, and none recommend a Sell. The average MELI stock price target is $1,476.58, indicating upside potential of almost 7.4% from current levels.

The Final Takeaway

MercadoLibre is now a global tech giant and is positioned to deliver market-beating returns to shareholders. I believe that its capability to achieve strong revenue growth, coupled with enhanced profit margins and the advantage of economies of scale, positions it as a prime investment option.