Ulta Beauty (ULTA) has sustained a 32% drop from its 52-week highs, presenting a rare investment opportunity. As the leading specialty beauty retailer in the U.S., Ulta continues to post strong results despite a slowdown in sales growth, which has spooked some investors. In fact, the company remains highly profitable, keeps expanding its footprint, and returns tons of cash to shareholders. With shares now trading at compelling valuations and Warren Buffett recently taking a stake in the company, I believe Ulta offers a notable upside potential for long-term investors. Hence, I am bullish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Investors Miss the Bigger Picture in Q2 Results

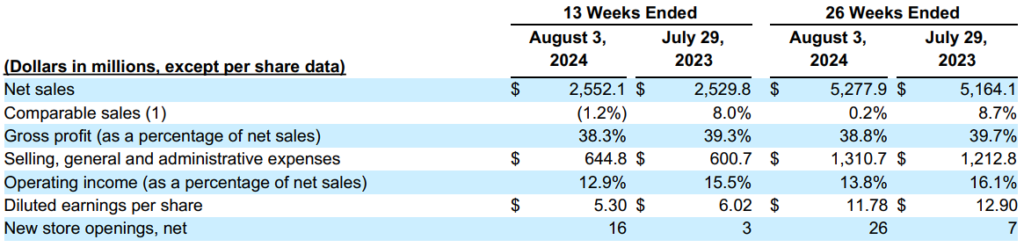

Ulta’s Q2 Fiscal 2024 results may have received a lukewarm response from the market, further fueling the cautious sentiment surrounding the stock. While net sales rose 0.9% year-over-year, reaching $2.55 billion, the market seems overly focused on the 1.2% dip in comparable sales, driven by a 1.8% decline in transactions. I understand why some might raise red flags over declining same-store sales, but I think this narrow focus misses the bigger picture. To me, the real story is Ulta’s ability to sustain its strength in a normalizing market, which only reinforces my bullish outlook on the stock.

In the Q2 earnings call, CEO Dave Kimbell emphasized that after experiencing an extended period of accelerated growth, the Beauty category is entering a normalization phase. Additionally, heightened competitive pressures in Prestige Beauty, particularly with the introduction of over 1,000 new distribution points by competitors in recent years, have challenged Ulta’s market share in key segments like Makeup and Hair Care. Despite these headwinds, the company’s overall positioning remains strong, especially as it expands its store count and digital capabilities.

Should Investors Be Worried About Revenue Deceleration?

Despite the 0.9% growth in Ulta’s net sales for Q2 marking a noticeable slowdown compared to previous quarters, I still remain bullish on the stock. In fact, Ulta’s top-line growth has recorded a sequential deceleration for 13 out of the last 14 quarters. However, I don’t find this deceleration overly concerning. According to Circana data, the beauty industry grew by just 3% in the first half of 2024, with mass beauty barely advancing. In this context, Ulta’s recent performance is relatively consistent with industry trends. It’s also critical to remember that the company is cycling against tough comps from 2022 and 2023, which saw quarterly growth rates from 20% to 65%.

In the meantime, Ulta has continued executing its expansion strategy, opening 17 new stores during the quarter (it also closed one, hence the 16 net) and ending the period with 1,411 stores. Along with strong digital sales and membership metrics, Ulta’s resilience as it traverses an evolving competitive landscape is quite evident. The company had 43.9 million active members at the end of the quarter, up 5% compared to last year, which should further support its top-line performance in the quarters ahead.

Profitability Remains Robust Despite Margin Pressures

Another important point to highlight, despite the current downturn in share prices, is that profitability remains a key factor for optimism. Although its gross margin fell to 38.3% from 39.3% a year earlier, the company remains highly profitable. The decrease was primarily driven by lower merchandise margins and higher store fixed costs, including payroll and benefits.

Yet, Ulta’s operating margin held a solid 12.9% despite these pressures. However, the company effectively demonstrated its ability to manage its cost structure, with its debt-free balance sheet providing additional support due to the absence of interest expenses and the contribution of interest income.

Valuation & Share Buybacks Signal a Buying Opportunity

Regarding its valuation, I view Ulta as one of the cheapest specialty retailers on the market. The company trades at a forward P/E of 17.4 times this year’s expected EPS, with earnings growth expected to rebound from next year. Given Ulta’s prolonged track record of revenue and earnings growth, as well as its clean balance sheet and aggressive capital return profile, I find today’s valuation multiple quite compelling.

Speaking of aggressive capital returns, Ulta repurchased $212.3 million worth of stock in Q2, pushing the total amount of repurchases over the past four quarters to $962.7 million. The company has now retired nearly 27% of its shares outstanding over the past decade, while $1.6 billion remains under its $2 billion repurchase authorization.

Warren Buffett Shows Confidence in Ulta

Warren Buffett’s Berkshire Hathaway ($BRK.A)($BRK.B) invested roughly $266 million in Ulta Beauty last month (now valued at around $269 million), which can naturally be seen as a strong endorsement of the company’s long-term potential. Known for identifying undervalued companies with solid fundamentals, I think Buffett’s investment shows trust in Ulta’s ability to endure near-term challenges while confirming the stock’s compelling valuation at today’s price levels.

Is ULTA Stock a Buy, According to Analysts?

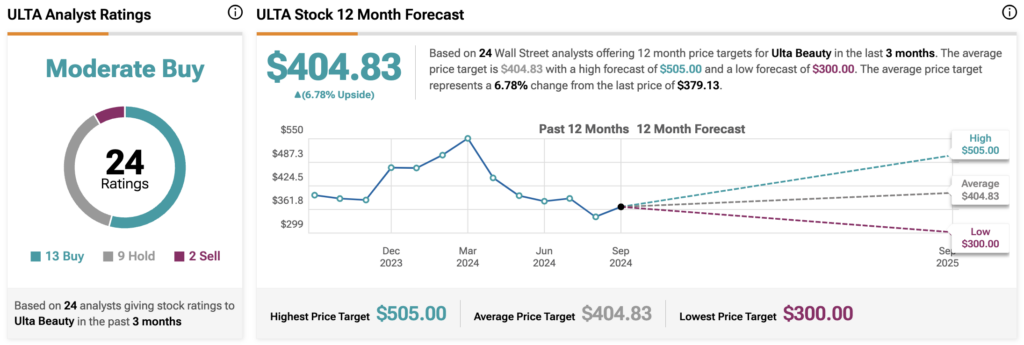

Looking at Wall Street’s view on the stock, Ulta Beauty maintains a Moderate Buy consensus rating based on 13 Buys, nine Holds, and two Sells assigned in the past three months. At $404.83, the average ULTA stock price target implies 4.22% upside potential.

If you’re unsure which analyst you can trust when you want to buy and sell ULTA stock, Christopher Horvers is the most accurate analyst covering the stock (on a one-year timeframe). He boasts an average return of 16.64% per rating and a 71% success rate. Click on the image below to learn more.

Key Takeaway

In conclusion, despite Ulta’s recent slowdown in sales growth and investor concerns over declining same-store sales, the company’s investment case remains compelling. Ulta keeps expanding its store footprint, maintaining solid profitability, and returning significant capital to shareholders through stock buybacks.

With Ulta’s valuations looking rather attractive at its current levels, a debt-free balance sheet, and Warren Buffett’s recent investment signaling confidence, I believe Ulta is well-positioned for noteworthy long-term returns.