“Summer’s going fast, night’s growing colder,” in the words of the late Neil Peart. According to Jason Draho, head of Americas asset allocation for UBS Global Wealth Management, this sentiment applies to the current market conditions as well. Draho perceives a current market heatwave, mirroring the weather, and anticipates the possibility of a cooler fall should the Fed show its intentions on paring back its anti-inflationary tight money policy.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

It’s a bit of a confusing picture. Inflation is lower now than it was a year ago but has been trending slightly upward in the last two months. The Federal Reserve has decided to pause its extended campaign against inflation, but its outlook suggests that interest rates will remain elevated over the next two years.

Draho explores these themes and come down to a bullish conclusion, writing, “We expect the economy to cool into year-end after this final blast of summer heat. Until there’s sufficient clarity for that happening, investors are likely to continue to toggle between ‘good is bad’ and ‘bad is good’ interpretations of the data, resulting in choppy, range-bound prices across asset classes. The prospect of the economy cooling enough for the Fed to end its hiking cycle by November creates the possibility that the markets could heat up as the weather starts to turn colder.”

Draho’s colleague, UBS analyst Vilas Abraham, is making a logical conclusion here and looking for attractively valued stocks with sound growth potential – and high dividend yields, rapidly approaching 15%. These are stocks that will bring investors a triple-play: an easy cost of entry, a good upside, and a strong dividend. Let’s take a closer look.

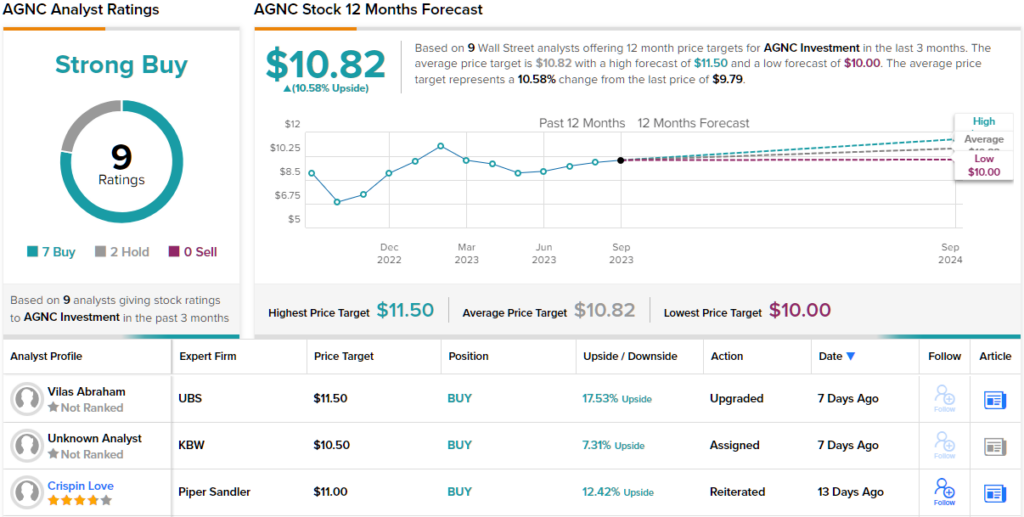

AGNC Investment (AGNC)

We’ll start with a REIT, a real estate investment trust. These stocks have long been popular with dividend investors; they have strong reputations for both reliable payments and high yields, exactly the combination that will appeal to investors seeking a ready passive income stream. AGNC has built a portfolio focused mainly on mortgage-backed security investments, valued at $58 billion at the end of 2Q23.

AGNC’s investments are heavily weighted toward the US real estate market’s most common product, the 30-year fixed mortgage. The securities make up $53.4 billion of AGNC’s portfolio, or 92% of the total value. The company’s remaining investments lean strongly toward 20-year fixed instruments, which are 2% of the total, and 15-year or less fixed, which make up 3% of AGNC’s investment activity.

The company realized a positive total net income in its last quarterly report, for 2Q23, of $286 million. This supported a non-GAAP earnings per share of 67 cents, which beat the forecast by 4 cents per share.

The company pays out a monthly dividend, rather than quarterly, and the most recent declaration, from September 13 for an October 11 payout, was for 12 cents per common share. The dividend has been held steady at this level since the April 2020 declaration, and the $1.44 annualized payment is currently yielding ~15%.

In his coverage for UBS, analyst Vilas Abraham sees a normalization of interest rate policy – or even an approach to that – as a long-term net-positive for AGNC. Of particular importance, Abraham notes the Fed’s hints that the end is in sight for the current tight-money cycle – but even more important, he points out that the central bank is backing out from the MBS market.

Getting into specifics, Abraham writes, “As a pure-play Agency MBS REIT, AGNC should benefit from favorable market dynamics for the asset class over the medium to long term. Specifically, as the Fed approaches the end of its tightening cycle, rate volatility subsides, and supply/demand dynamics gradually improve, we believe AGNC’s performance should be able to drive ~30% total return. This includes a significant div yield of ~15%. Through this cycle AGNC protected its dividend through effective hedging and should generate strong enough returns to maintain its payout. We also forecast book value appreciation of ~11% book value accretion (ahead of cons. at ~6%) as well as modest multiple expansion. Furthermore, to the extent that recession risk (and therefore credit risk) grows again at some point, we think AGNC should benefit from a flight to quality as the purest play public Agency MBS REIT.”

To this end, Abraham rates AGNC shares a Buy, and his $11.50 price target points toward a 17.5% one-year upside potential. Based on the current dividend yield and the expected price appreciation, the stock has ~32% potential total return profile.

Overall, it’s clear from the Street’s consensus on AGNC that Abraham is no outlier; the stock has a Strong Buy rating, based on 9 recent analyst reviews that include 7 Buys against 2 Holds. (See AGNC stock forecast)

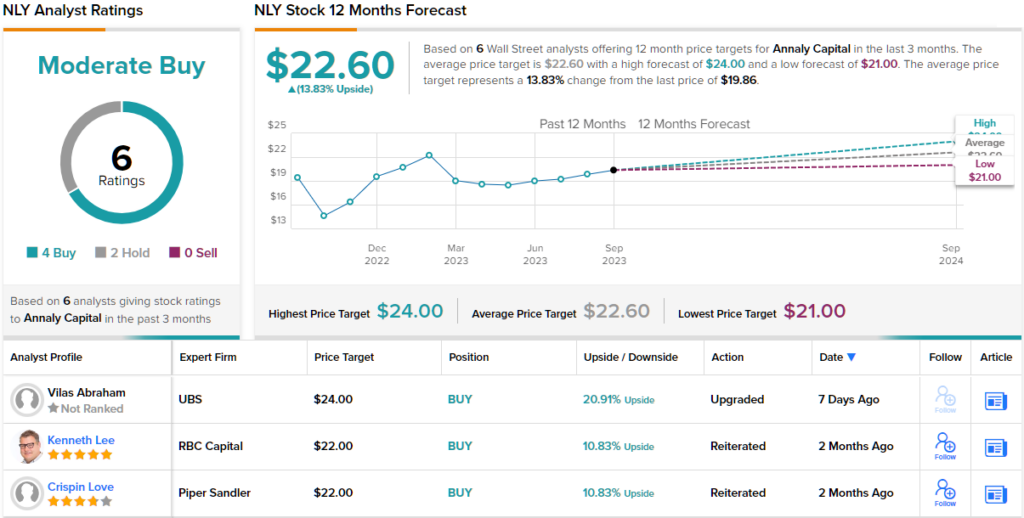

Annaly Capital Management (NLY)

Next up is Annaly Capital Management, another REIT with a focus on mortgage-backed securities. This company, with a market cap exceeding $9 billion, is one of the real estate market’s largest mREITs. Annaly’s portfolio includes total assets worth nearly $79 billion, and the company also lists some $12 billion in permanent capital. The portfolio rests on a diversified set of assets, including securities, loans, and equities, all targeted in the mortgage finance market.

Some interesting statistics will give a fuller picture of Annaly’s portfolio. 98% of the assets are in fixed-rate mortgages. The company’s mortgage services rights investments grew by 19% from the previous quarter to reach $2.2 billion, while the company’s investment in residential credit declined slightly, to $4.9 billion. The company has $6 billion in unencumbered assets.

The monthly dividend payout was declared on September 7 for a September 28 payout, at a rate of 65 cents per common share – fully covered by the EAD. The dividend annualizes to $2.60 and gives a forward yield of ~13%.

Once again, UBS’s Abraham is looking at the Fed’s actions as a key point for this REIT. He writes of the stock, “As the largest Agency MBS focused mREIT, [NLY] should benefit as market dynamics for the asset class improve over the coming quarters. Specifically, as the Fed approaches the end of tightening, rate volatility subsides, and supply / demand dynamics gradually improve, NLY’s performance should be able drive ~30% total return. This would be composed mainly of a ~13% div yield but book value appreciation (~9% vs ~4% cons) and multiple expansion (~5%) should also contribute… NLY is our preferred pick in the sector.”

An upbeat stance like that should naturally come with an upbeat forecast, and Abraham rates these shares a Buy, with a $24 price target implying an upside of 21% for the coming year. With the 13% dividend yield taken into account, the potential 12-month return here is 34%.

All in all, NLY stock gets a Moderate Buy from the Street’s analyst consensus, based on 6 analyst reviews that include 4 Buys and 2 Holds. (See NLY stock forecast)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.