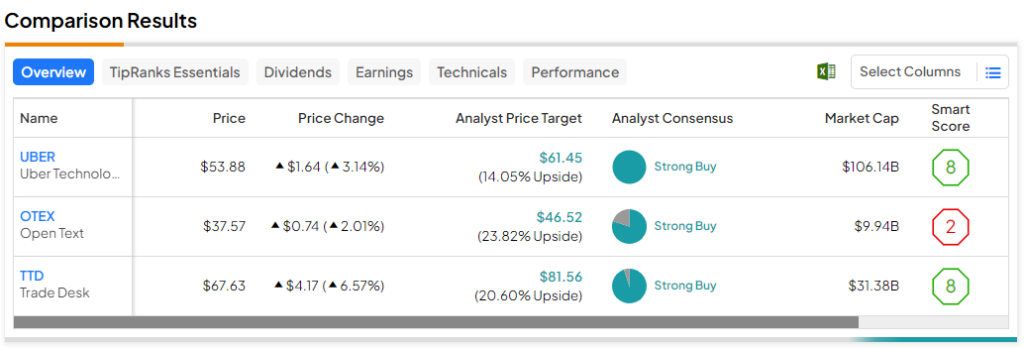

Stocks have heated up in a hurry this month, recovering a big chunk of the ground lost during the September-October market correction. With rates on the retreat and stocks on the mend, Strong-Buy-rated tech stocks outside of the red-hot Magnificent Seven group — such as UBER, TTD, and OTEX — may finally be in a spot to lead the markets higher into the new year.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

As the so-called Magnificent Seven continue flexing their muscles, the real question is whether the rest of tech can catch up or even match the magnificence of the Magnificent Seven. Therefore, in this piece, we’ll check out three Wall Street-favored tech plays using TipRanks’ Comparison Tool.

Uber (NASDAQ:UBER)

Investors who hailed a ride on Uber stock since shares bottomed in the summer of 2022 have been richly rewarded. The stock is up more than 150% since its late-July lows and is now in striking distance of its early-2021 all-time highs, just north of $64 per share. Undoubtedly, management deserves a round of applause for delivering (pardon the pun) its first and second quarters of positive GAAP profits. The company talked the talk and is now walking the walk. This makes me very bullish.

As management continues its profitability push, the stock may still prove severely undervalued in a few years as earnings growth looks to compress the stock’s price-to-earnings (P/E) multiple. Uber stock may have been a somewhat tricky stock to evaluate before it clocked in its first operating profit. However, if you’ve been following the analyst community, you’d know how highly Wall Street has viewed the firm, even as it sunk to ominous depths just over a year ago.

Indeed, Wall Street was right on the money about Uber. And with the pathway to profitability and growth as clear as it’s ever been, I’d argue that now’s not a good time to take profits as the company proves that it can grow profitably.

Looking ahead, Uber appears ready to move on to higher ground as the firm finds the optimal balance of sales growth and margin enhancement. The company, which used to be a “black hole” for cash, could find itself flush with free cash flow going into the new year. Wedbush analyst Scott Devitt thinks the firm may wish to start buying back some of its own stock. If shares are, in fact, still cheap, a buyback seems like a wise move as the company continues its evolution.

What is the Price Target for Uber Stock?

Uber stock’s a Strong Buy, according to analysts, with 29 unanimous Buy ratings assigned in the past three months. The average UBER stock price target of $61.45 implies 14.1% upside.

The Trade Desk (NASDAQ:TTD)

The Trade Desk is an ad-tech firm whose shares came to a plunging halt this summer. After another rough quarter (with a side of some ugly outlook) that sent shares tumbling by double-digit percentage points, shares are now finding themselves down 26% from 52-week highs and 37% off all-time highs. Undoubtedly, ad headwinds have been quite prevalent throughout the year. Given ongoing macro uncertainties, it seems smart for management to err on the side of caution by forecasting a modest (and disappointing) Q4 revenue figure of $580 million on the low end.

Jason Helstein, an analyst over at Oppenheimer, views ad headwinds as a “temporary” phenomenon and recommends buying the dip in the stock. I think Helstein’s contrarian call is the correct one to make. For those looking to play the long game, ad headwinds are really nothing to hit the panic button over. Further, it may not take much for the ad market to turn a corner, especially if the economy manages to steer clear of a recession in 2024. For the turnaround potential, I’m staying bullish on the stock.

At writing, TTD stock looks expensive at 55.9 times forward price-to-earnings (P/E), well above the application software industry average of 32.7 times. Even Mad Money host Jim Cramer acknowledged that the stock still looks expensive. That said, The Trade Desk stands out as one of the tech stocks that could easily grow into its high multiple once the economic tides turn. Perhaps falling rates and the avoidance of a recession may be enough to power TTD stock back to new heights.

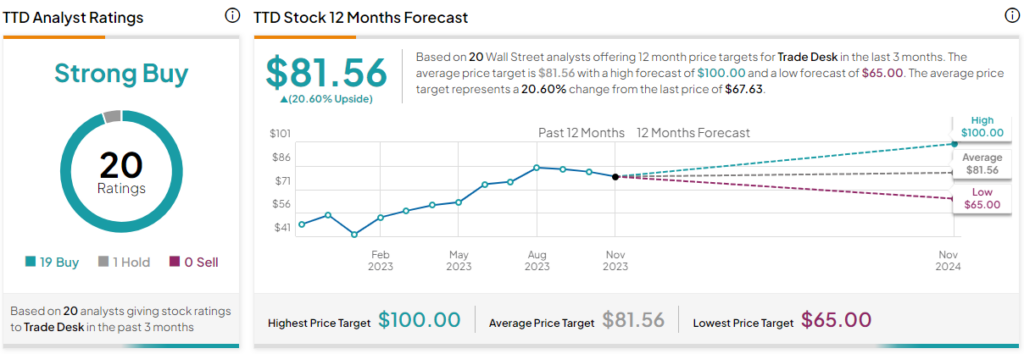

What is the Price Target for The Trade Desk Stock?

The Trade Desk stock is a Strong Buy, according to analysts, based on 19 Buys and one Hold rating. The average TTD stock price target of $81.56 implies 20.6% upside.

Open Text (NASDAQ:OTEX)

Open Text is a Canadian IT software developer whose shares are down around 32% from their all-time high hit back in mid-2021. The stock stands out as one of the market’s more “GARPy” (growth at a reasonable price) plays, with a modest 29.1 times trailing P/E multiple (miles below the application software industry average of 86.75 times) alongside a solid 2.7% dividend yield.

Over the last 10 years, the company has averaged revenue growth of 12.7%. That’s not bad growth for a mid-cap (around $10 billion market cap) firm that’s found a way to thrive in a vast market. Though shares could stay choppy in this rocky economic environment, I’m inclined to side with analysts with a bullish stance.

It’s no mystery that enterprises have been pulling back on their IT spending to trim away costs. Sales cycles have slowed notably of late. However, enterprise spending could return to baseline, perhaps faster than expected, if the Fed can orchestrate a soft landing for the economy in 2024.

At the end of the day, Open Text has an innovative product in a massive market $4.7 trillion global IT market that’s for the taking.

What is the Price Target for Open Text Stock?

Open Text is a Strong Buy, according to analysts, with four Buys and one Hold assigned in the past three months. The average OTEX stock price target of $46.52 implies 23.8% upside.

Conclusion

There are plenty of magnificent tech stocks out there that can flex their muscles as impressively as the Magnificent Seven as we move into the next leg of the tech market rally. Wall Street views each of the three aforementioned names favorably but sees the most upside potential from Canadian IT play Open Text.