Targeted advertising is increasingly being favored by advertisers, as it allows them to monetize user data effectively. However, in some cases, it is also giving rise to data privacy concerns leading to companies coming up with innovative solutions to monetize user data without compromising on privacy concerns.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

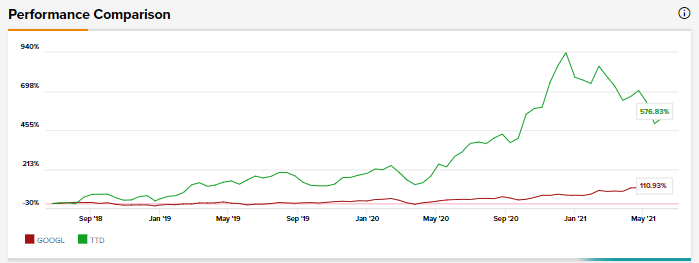

Using the TipRanks Stock Comparison tool, we will compare two companies that provide targeted advertising services, theTradeDesk and Alphabet, and see how Wall Street analysts feel about these stocks.

TradeDesk operates a self-service cloud-based advertising platform where ad buyers can manage, create and optimize data-driven digital advertising campaigns across different advertising formats and channels.

TTD generates revenues by charging its clients a platform fee that is based on a percentage of the client’s total advertising spend. The company also earns revenues through providing data and other valued-added services (VAS) and platform features.

In Q1, TTD posted revenues of $219.8 million, a jump of 37% year-over-year and non-GAAP diluted earnings of $1.41 per share versus $0.9 in the same quarter last year.

For Q2, the company expects revenues to vary between $259 million to $262 million and adjusted EBITDA of $84 million. TTD also said that demand for its advertising platform had been significantly impacted by the COVID-19 pandemic. As a result, the company is facing uncertainty when it comes to its business outlook.

Needham analyst Laura Martin is bullish on TTD with a Buy rating and a price target of $100 (63.2% upside) on the stock. According to Martin, the company’s management is focusing on four key areas of revenue growth. These include shopper marketing, expanding in international markets, Solimar and programmatic advertising upfronts for connected TV (CTV).

TTD said at its earnings call that the total addressable market (TAM) for shopper marketing exceeds $100 billion, and retailers are increasingly looking at monetizing their data about shoppers.

As a result, in Q1, TradeDesk partnered with Walmart (WMT) to launch a demand-side platform (DSP) that will provide advertisers access to WMT’s shopper data and sales measurement data.

Martin views this as a positive move and said, “Shopper marketing budgets almost always sit outside the traditional brand advertising spending that TTD’s platform handles today, so all of this revenue represents potential new dollars to be spent on TTD’s platform by its existing CPG (consumer packaged goods) brand advertising clients.”

TTD’s focus on CTV continues and in Q1, advertising spend from international advertisers grew more rapidly than in North America. The company is also seeing traction in terms of revenues from its investment in CTV in Europe. The company also launched its platform in India last week.

The company is giving its advertising platform a major upgrade with Solimar, which is expected to be launched later this year. Solimar is anticipated to provide better-targeted advertising for advertisers with an easy-to-use user interface. It will also provide earlier ramp-up for TTD’s customers’ first-party data and better tracking of return on investment (ROI) for every dollar spent by advertisers. (See TradeDesk stock chart on TipRanks)

According to Martin, “The last time TTD did a platform upgrade, we estimate that it drove an incremental 10% rev upside over the first 12 months, because TTD upgrades/changes things requested by its clients. By implication, clients use these features more, once TTD adds them to its platform.”

The analyst added that while TTD’s clients have asked TTD to get involved in the upfronts market to add data to their CTV and linear television ad purchases, the company is just starting and “any product here is a long way away and will take several years to create and introduce.”

Consensus among analysts on Wall Street is a Strong Buy based on 10 Buys and 3 Holds. The average TradeDesk analyst price target of $75.15 implies approximately 22.7% upside potential to current levels.

Alphabet reports its businesses under two segments: Google Services and Google Cloud. Google Services has core products and platforms, including Android, Chrome, Gmail, Google Drive, Google Maps, Google Photos, Google Play, Search, and YouTube.

Google Services generates revenues through targeted advertising that users are likely to click on. Advertisers pay GOOGL when a Google user engages with such ads. Google also earns revenues through brand advertising, by engaging users through videos, text, images, and other interactive ads that run across its platforms.

The company’s Google Cloud offers enterprises cloud services, including Google Cloud Platform and Google Workspace.

In Q1, GOOGL had total revenues of $55.3 billion, up 34% year-over-year. The company reported diluted EPS of $26.29 per share versus $9.87 per share in the same quarter last year.

GOOGL had advertising revenues of $44.7 billion in Q1, a jump of 32.3% year-over-year. The company stated on its earnings call that when it comes to advertising on YouTube, it believes that “there is significant opportunity for innovation that will improve the user experience and provide better ROI [return on investment] for advertisers.” (See Alphabet stock chart on TipRanks)

In Q1, the company’s Google Services business benefitted from an increase in online activity and higher advertising spend from advertisers. The company expects that “…it is too early to say how durable this consumer behavior will be as economies recover and restrictions on mobility are lifted.”

GOOGL further added that currently, 2 billion users log in to YouTube and watch billions of hours’ worth of videos every day. Considering this data, YouTube offers advertisers an efficient platform to reach their audiences.

Around 10 days back, Tigress Financial Partners analyst Ivan Feinseth reiterated a Buy with a target price of $3,185 on the stock. Feinseth stated that the company’s “accelerating growth in online advertising and spending, along with increasing cloud growth and margin expansion, will continue to drive further share price gains.”

“GOOGL is consolidating its ability to advertise across all of its advertising platforms, including YouTube, display, Search, Gmail, and maps through its Performance Max advertising campaign builder, ” Feinseth added.

The analyst believes that the rise in Google’s digital advertising, its gain in market share and the company’s innovation “should provide upside to our current expectations and continue to drive GOOGL’s long-term shareholder value creation.”

Consensus among analysts on Wall Street is a Strong Buy, based on 28 Buys and 2 Holds. The average Alphabet analyst price target of $2,785.97 implies approximately 14.5% upside potential to current levels.

Bottom Line

It is important to note that while Google owns most of the platforms that offer targeted advertising to advertisers, TradeDesk earns a majority of its revenues through a platform fee from advertisers using its platform. TTD is currently focusing on CTV advertising and rapid expansion in international markets, and is considering adding new features or upgrading its advertising platform.

Additionally, while Google is doing away with third-party cookies when it comes to advertising, TradeDesk has come up with Unified ID (UID), an open-source application that provides marketers with data for targeted advertising while customers remain anonymous, providing a solution to data privacy concerns.

While analysts are bullish about both stocks, based on the upside potential over the next 12 months, TTD seems a better Buy.

Disclaimer: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities.