Tractor Supply Company (NASDAQ:TSCO) isn’t your average home improvement stock. It has distinguished itself from other stocks in the industry by catering to a more rural customer base and offering products that cover all things house, farm, and animal related. The stock has performed very well over the past few years, as the company has exhibited great growth attributes, and despite its excellent returns, it still presents an attractive investment opportunity. Therefore, I am bullish on TSCO.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

A Different Home-Improvement Destination

Tractor Supply combines the attributes and product offerings of a large general store and a home improvement destination. The company prides itself in being the largest rural lifestyle retailer in the United States. Its target clientele includes recreational farmers, ranchers, home, pet, and livestock owners, as well as anyone who lives and enjoys a more rural lifestyle.

The company operates on a retail basis, marketing its products through both physical stores and online marketplaces. TSCO operates under the names “Tractor Supply Company,” “Petsense by Tractor Supply,” and “Orscheln Farm and Home” (acquired in late 2022). Tractor Supply currently maintains more than 2,000 stores in 49 U.S States.

Pet and Animal Product Sales Lead the Way

According to the company’s 2022 10-K report, 50% of sales currently originate from the Livestock & Pet segment. The pet products market is increasing in size and presents a major growth driver for Tractor Supply. It is also an area where Tractor Supply holds a significant market share.

To be more specific, household penetration rates for pet ownership have increased to 70% in the past couple of years. Further, total pet industry expenditures have increased significantly over the past few years to over $120 billion. The COVID-19 pandemic led many households to explore pet ownership for the first time, while for the next few years, industry trends appear positive.

Capitalizing on the pet industry’s growth, Tractor Supply aims to become a one-stop-shop destination for home improvement, landscaping, and farming/ranching as well. People leaving big cities to embrace a more rural lifestyle has become a trend in the U.S. after the COVID-19 pandemic, especially as remote work is now widely used in many industries.

Orscheln Farm and Home Acquisition Supports Midwest Expansion Plans

On October 12, 2022, Tractor Supply completed its acquisition of Orscheln Farm and Home. Approximately 166 stores of Orscheln were acquired for around $320 million (before working capital adjustments). The majority of stores are to be divested into Tractor Supply stores by the end of Fiscal 2023. The deal is part of the company’s renewed growth strategy and is expected to help in its Midwest expansion. In its press release following the acquisition, management claimed that the deal is expected to add at least $300 million in sales for the company in 2023.

Continuous Revenue and Profit Growth

Tractor Supply has manifested a rather impressive growth story over the past few years. Since 2018, revenue has grown from $7.9 billion to $14.2 billion in 2022 — a compound annual growth rate (CAGR) of 14.4%. On a longer-term basis, sales have grown at an 11.8% CAGR for the past decade, showing longevity and consistency. Notably, over the next couple of years, analysts expect high-single-digit revenue growth.

Management’s forecast for the 2023 fiscal year looks for $15.0 billion – $15.3 billion in sales. Comparable store sales growth is anticipated within the range of 3.5% to 5.5%.

Earnings have followed sales on the path upward as well. For instance, net income has increased at a 20.8% CAGR over the past five years and 14.7% over the last decade. EPS has increased a bit more, aided by share repurchases. Over the next couple of years, analysts see EPS growing at around 10% annually.

High Profitability

Tractor Supply displays relatively strong profitability metrics. A gross margin of 35% stands very close to the sector average, while EBIT and net margins of 10.1% and 7.7% indicate efficient operations.

TSCO also offers some impressive numbers when it comes to returns on equity. While most investors generally view companies with an ROE over 10% favorably, TSCO has historically maintained an ROE of around or over 30%. Over the past couple of years, ROE has increased significantly, climbing above 50% recently.

High Dividend Growth Potential Plus Share Buybacks

Tractor Supply currently offers a 1.8% forward dividend yield, close to the market average. While larger peers in the industry offer higher yields (over 2%), it could be argued that they lack the growth potential of TSCO. Over the past five years, Tractor Supply has grown its dividend at an impressive 28.5% CAGR, significantly exceeding sector averages. During the Q4 earnings call, management reiterated their commitment to increasing distributions to shareholders.

Management’s strategy to increase shareholder returns also entails share repurchases. TSCO’s diluted share count has decreased from 123 million in 2018 to 112 million in 2022. For 2023, the company anticipates buybacks of $575 million to $675 million, looking to reduce the company’s weighted average shares outstanding by approximately 2% (net reduction).

A Premium, Justified Valuation

After a large run-up in stock price over the past five years, it should be expected that TSCO’s valuation would be a bit stretched. Since 2018, the stock price has increased by 270% while diluted EPS has increased by 125%. The valuation multiple expansion reflects the market’s high expectations of the company. Currently, TSCO trades at a 22x forward P/E ratio and a 1.7x forward P/S ratio, both higher than sector averages. However, this could be justified since TSCO is a top company in its sector.

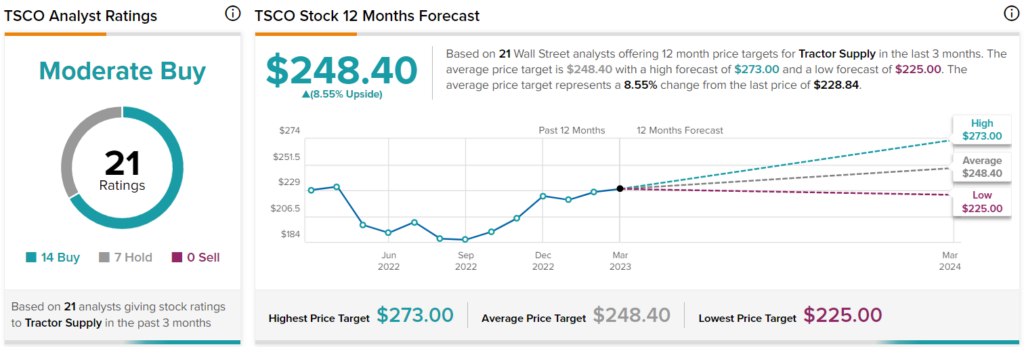

Is TSCO Stock a Buy, According to Analysts?

Turning to Wall Street, TSCO has a Moderate Buy consensus rating based on 15 Buys and seven Hold ratings assigned over the past three months. The average TSCO stock price forecast of $248.95 represents a 8.55% upside potential.

The Takeaway

When all things are considered, Tractor Supply represents a rather attractive investment opportunity that displays strong business and financial attributes. I believe TSCO stock is likely to outperform the market.