Cathie Wood has built her career on holding contrarian views and her Ark Invest firm has been known to go against the grain. As such, 2022’s bear market has done little to change her stance. In fact, recently, Wood has been arguing that the Fed’s aggressive monetary stance in its ongoing efforts to curb soaring inflation is misguided. Highlighting deflationary signals, Wood says that unless it changes tack, the Fed’s actions could result in a repeat of the the Great Depression.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

“If the Fed does not pivot, the set-up will be more like 1929,” Wood opined. “The Fed raised rates in 1929 to squelch financial speculation and then, in 1930, Congress passed Smoot-Hawley, putting 50%+ tariffs on more than 20,000 goods and pushing the global economy into the Great Depression.”

Meanwhile, back in the here and now, the Fed’s policies and interest rate hikes have played havoc with the markets and have sent shares across the board tumbling, leaving many stocks looking rather cheap.

So, Wood has gone shopping and we used TipRanks’ database to find out what the analyst community has to say about two small stocks, under $5, that her firm snapped up recently. As it turns out, each ticker has received only Buy ratings. Not to mention substantial upside potential is also on the table.

ATAI Life Sciences (ATAI)

Wood has been known to favor cutting-edge companies and the first pick certainly reflects that. ATAI is at the forefront of what could be a new paradigm in treating mental health disorders – it is testing the use of psychedelics for medicinal purposes.

The company’s business model is differentiated; it operates via a decentralized platform that purchases and runs clinical programs with small affiliate companies formed around the pipeline candidates. All can access shared funds, with the capital allocated per needs.

After discarding some of its early programs deemed superfluous, the company’s pipeline has been toned down to 8 candidates aimed at treating depression, anxiety, schizophrenia and substance abuse.

Leading the way is PCN-101/R-ketamine, indicated as a therapy for treatment resistant depression (TRD). Then there is RL-007, which targets cognitive impairment associated with schizophrenia. Both of these drugs are currently in phase 2 studies.

Further back in development, the pipeline includes GRX-917 (deuterated etifoxine), which is being developed for generalized anxiety disorder (GAD), and for which the company recently announced positive preliminary pharmacokinetics and pharmacodynamics results from a Phase 1 study. Positive preliminary results of the single ascending dose (SAD) portion of the Phase 1 testing of KUR-101 (deuterated mitragynine) indicated to treat opioid use disorder (OUD) were also recently announced.

With the shares down by 64% year-to-date, Wood has been in a buying mood. In Q3, Ark Invest splashed out on 6,133,914 ATAI shares, increasing its position by 280%. At the current share price, these are now worth $17.61 million.

With top-line data for PCN-101’s Phase 2a proof-of-concept trial anticipated before the year’s end, Canaccord analyst Sumant Kulkarni thinks the upcoming readout could dictate near-term sentiment, although the analyst also thinks those taking the long-term view will be rewarded eventually.

Kulkarni writes, “We believe it is important for the stock that PCN-101 hits the objectives. As with any neuropsychiatry trial, we are mindful of the risks, but at current levels we view the absolute dollar downside as less than the potential upside.”

“Our bigger picture thesis on the stock remains the same,” the analyst went on to add, “i.e., we continue to believe ATAI presents a potentially solid opportunity for investors (especially those who have patience and/or a longer-term focus) to participate in the underserved mental health space. Along these lines, we point to ATAI’s relatively diverse mental health-focused pipeline (with a good mix of non-psychedelic and psychedelic compounds), and cash runway into 2025E that covers some potentially meaningful catalysts.”

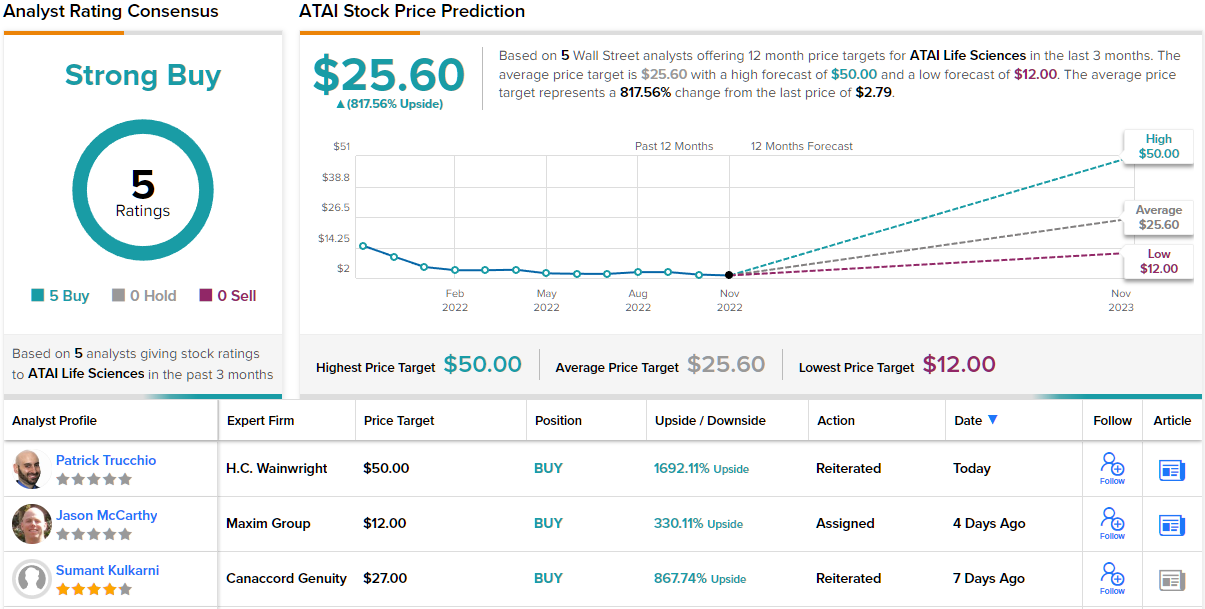

Kulkarni is evidently extremely bullish; along with a Buy rating, the analyst’s $27 price target makes room for one-year gains of an extraordinary 868%. (To watch Kulkarni’s track record, click here)

Kulkarni’s take is no anomaly; all current reviews – 5, in total – are positive, providing the stock with a Strong Buy consensus rating. Moreover, the average target stands at $25.60, suggesting they will climb ~818% higher over the 12-month timeframe. (See ATAI stock forecast on TipRanks)

SomaLogic (SLGC)

The next Wood pick we’ll look at is a protein biomarker discovery and clinical diagnostics company. SomaLogic operates in what is known as the proteomics space. This is an emerging segment with the global proteomics market anticipated to expand by 15% a year and reach $64 billion in 2024.

SomaLogic is eyeing a big chunk of this market and might have the tools to do so. Its SomaScan Discovery Platform can examine 7000 proteins in just 55 microL of blood sample, well beyond the abilities of any competitors. It has also built up a strong client list which includes Bristol-Myers Squibb, Novartis, Amgen, University of Cambridge, and Stanford, amongst others. Furthermore, both FDA and NIH labs use its proteomics platform.

The company is relatively new to the public markets, and IPOd in September 2021 through a SPAC merger. The timing is unfortunate, as SPACS have been seriously out of favor in 2022’s bear market. To wit, the shares are down by 77% since the turn of the year.

With the stock on the backfoot, Wood evidently thinks it offers good value. Ark Invest opened a new position in SomaLogic in Q3 and snapped up 11,017,672 shares. These are currently worth over $29.6 million.

Also taking the bullish view is Stifel analyst Daniel Arias, who within the emerging proteomics space, sees Somalogic as “best-in-class in several ways.”

“The company has a first-mover advantage in the market, thanks to an established portfolio that has been in the market for several years and has formed the basis for solid relationships with key commercial (i.e. Novartis and Amgen) and academic research institutions,” Arias explained.

“Quarterly ups and downs for SLGC have made modelling visibility tough this year, but 4Q could hold some upside potential, ’23 should still be a solid growth year for the company – and we continue to see SLGC as one of the companies that is well-positioned to capitalize on an expanding proteomics market. With shares trading near cash, we think they screen as attractive within the smid cap space,” the analyst added.

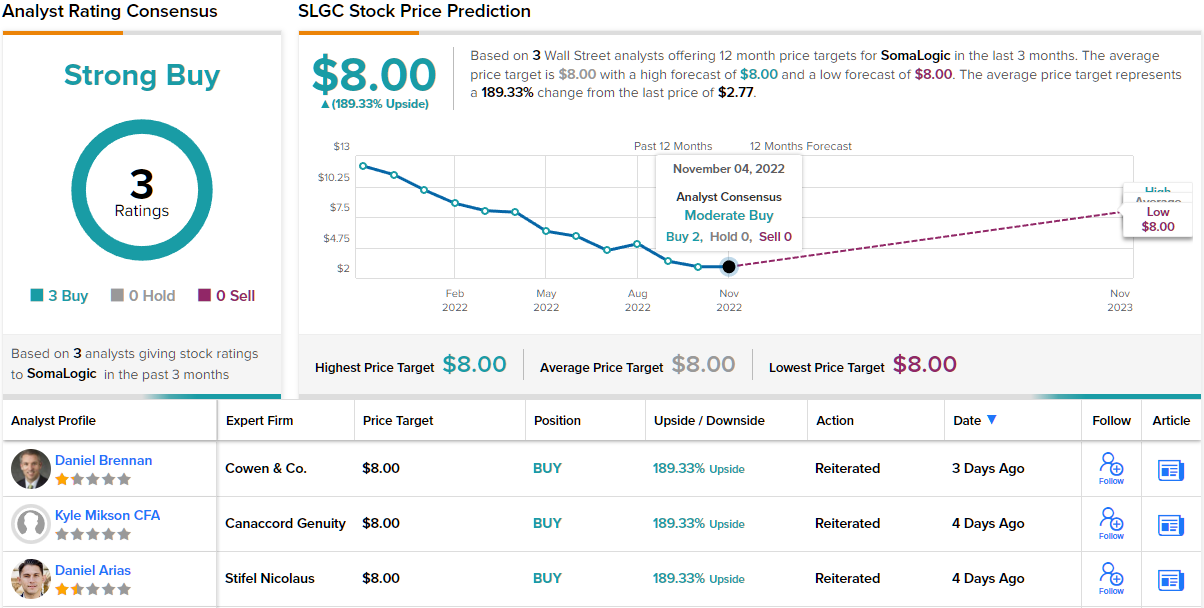

To this end, Arias rates SLGC shares a Buy, while his $8 price target suggests the stock’s value could soar ~189% in the year ahead. (To watch Arias’ track record, click here)

Do other analysts agree with Arias? They do. Only Buy ratings, 3, in fact, have been issued in the last three months, so the consensus rating is a Strong Buy. At $8, the average price target is the same as Arias’. (See SLGC stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.