Sentiment shifts periodically on Wall Street, and you could argue Cathie Wood might be the prime example of fortune reversal. Once an investor favorite and hailed as a pioneer with a portfolio jam-packed with the novel and cutting-edge, Wood’s reputation has been tarnished over the past year and a half as her growth-oriented investing style went out of fashion in the post-pandemic climate.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Does that mean Wood is ready to desert her strategy of backing innovative yet risky and often unprofitable names in search of safer havens? No, is the short answer.

Recently, the ARK Invest CEO has been loading up on two stocks that fit a certain profile; they offer game-changing potential and which might just be too cheap to ignore – both are currently changing hands for under $10. According to Wall Street analysts, both also feature robust triple-digit upside potential, indicating the possibility to double or more going forward.

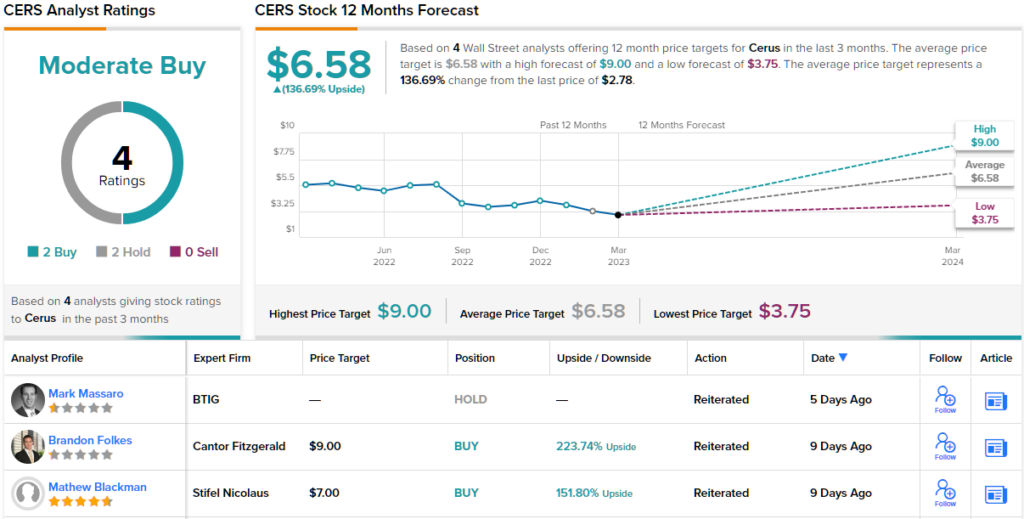

Cerus Corporation (CERS)

It’s well-known that Cathie Wood has a penchant for disruptors and those are often found at the junction where health and tech meet. This is where you can find medical device company Cerus, whose goal is to be the standard of care in blood transfusion medicine.

The Intercept Blood System, which the company makes and sells, is intended to destroy blood-borne infections in platelets and plasma – components of donated blood. For these two blood components, the product is the sole pathogen reduction system boasting both a CE mark and FDA approval.

Shares, however, took a bit of a beating earlier this year after the company released disappointing revenue guidance for 2023. The company’s outlook for the full-year called for product revenue between $165 million– $170 million. Analysts were expecting the company to generate revenues of $193.3 million. The company’s Q4 results, released at the end of February, were also a mixed bag; product revenue reached $44.03 million, amounting to a 10.4% year-over-year increase and just edging ahead of the Street’s forecast. However, EPS of -$0.08 fell short of the -$0.06 expected on Wall Street.

The result is a stock down by 24% since the turn of the year – and 50% over the past 12 months.

Cathie Wood must see plenty to like here. Via her ARKK (Ark Innovation) and ARKG (ARK Genomic Revolution) funds, she has purchased 4,048,858 shares so far this year. Overall, she holds 12,150,378 shares via ARKK, and 5,970,211 shares via ARKG. Combined these are currently worth more than $50 million.

Mirroring Wood’s confidence, Cantor analyst Brandon Folkes sees more growth coming Cerus’ way.

“We believe adoption of the company’s Pathogen inactivation platelets is driving sustainable double-digit kit growth in the U.S.,” Folkes said. “For the long term, Cerus is developing Intercept-treated red blood cells, targeting a $2B market opportunity in North America and EMEA. In our view, near-term execution, as well as long-term development plans, which are well-in-motion, position CERS for potential significant upside. We expect the U.S. to drive near-to-medium-term growth, with the ex-U.S. opportunity to drive medium-to-long-term growth, and thus we remain confident about the sustained, long-term growth potential for CERS.”

To this end, Folkes rates the shares an Overweight (i.e., Buy), while his $9 price target makes room for 12-month gains of ~224%. (To watch Folkes’ track record, click here)

Turning now to the rest of the Street, opinions are split evenly. 2 Buys and 2 Holds add up to a Moderate Buy consensus rating. The shares are priced at $2.78, and the $6.58 average price target suggests it has ~137% upside ahead of it. (See Cerus stock forecast)

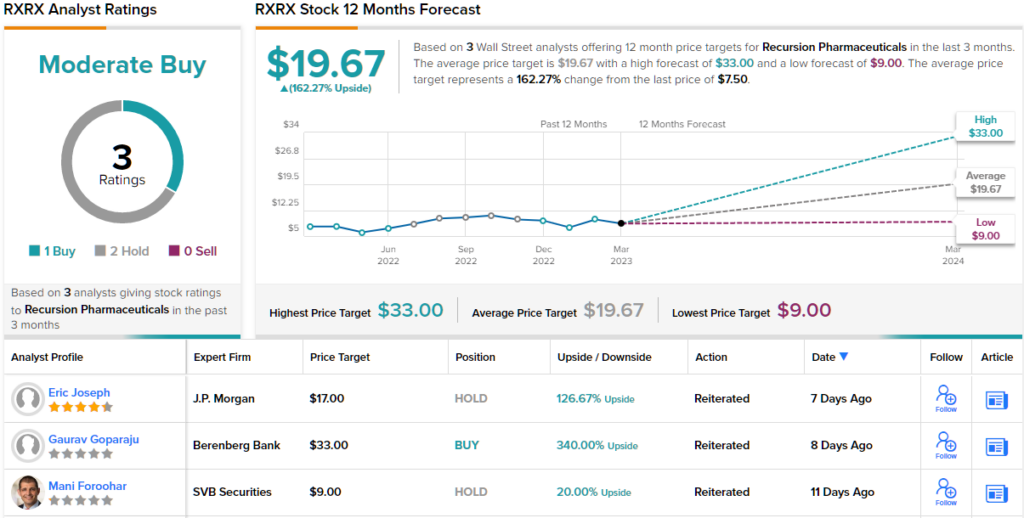

Recursion Pharmaceuticals (RXRX)

AI has been a big headline maker this year and is also used by our next Wood-backed stock. Recursion Pharmaceuticals aims to revolutionize drug discovery with the use of AI. This it intends to do by developing a pipeline based on its Recursion Operating System (OS) technology.

The company uses advanced machine learning methods to extract from its dataset a set of trillions of searchable connections in biology and chemistry that are unrestricted by human bias. This technology has the ability to address diseases in hitherto unexplored ways. Also, it is used to target rare disorders for which there are currently no therapies.

Recursion has nabbed collaborations with pharma giants Bayer and Roche, and has a clinical pipeline that includes three Phase 2 programs.

The Phase 2/3 POPLAR clinical trial (REC-2282) evaluates ~90 participants with progressive NF2-mutated meningiomas. The company is currently enrolling participants and expects to have a Phase 2 interim safety analysis in 2024.

Enrollment is also ongoing for the Phase 2 SYCAMORE clinical trial of REC-994, a study of 60 participants with cerebral cavernous malformation (CCM). Top-line data for this study is anticipated in 2H24. Additionally, the Phase 2 TUPELO clinical trial (REC-4881) is assessing the efficacy, safety, and pharmacokinetics of this drug candidate in patients with Familial Adenomatous Polyposis (FAP).

This promising biotech stock has piqued the interest of Cathie Wood, who bought 416,895 shares in 2023 via the ARKG fund. Overall, she holds 3,458,041 shares, which at the current market price are presently worth ~$26 million.

Also taking the bullish view is Berenberg analyst Gaurav Goparaju, who highlights several reasons why investors should get on board.

“Through its full-stack technology platform, Recursion OS, RXRX has continued to build one of the largest proprietary in vitro biological and chemical datasets in the space… The Bayer and Roche-Genentech deals represent some of the largest and most sophisticated discovery collaborations in the space (~$13bn in combined potential milestones, plus royalties) and provide early validation of RXRX’s platform, in our view,” Goparaju opined.

As such, on the back of “continued platform development, internal pipeline advancement into the clinic, material collaboration progression, and a strong balance sheet,” Goparaju rates RXRX shares a Buy. He backs the rating up with a $7.95 price target, implying upside of a hefty 340% from current levels. (To watch Goparaju’s track record, click here)

Looking at the consensus breakdown, based on 1 Buys and 2 Holds, the analysts view this stock as a Moderate Buy. The shares are currently trading for $7.5 and their $19.67 average price target implies an upside of 162% from that level. (See RXRX stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.