A rising-rates environment can be scary. After years of lasting euphoria in the markets, the time many investors had feared coming (and many hadn’t even fathomed was possible in the first place) has already become the norm. Who would have thought that near-zero rates wouldn’t be sustainable forever, right?

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

In any case, over the past few months, we have all experienced firsthand the result of rising rates. When rates go up, equities go down. Why is that? In the simplest format possible, think about it this way:

Government bonds are typically considered risk-free securities. If the risk-free rate (return) in the market environment goes up, investors require a higher return from risk-bearing securities (e.g., stocks) than before (i.e., they price these securities lower). If I can get 4% from a government bond, I may no longer require, say, an 8% expected return from a stock like I previously did, but 12% in order to compensate me for the extra risk I am taking. It makes total sense, and there’s nothing wrong with it.

Nevertheless, while many investors are focused on the negative impact of interest rates on stocks, certainly fewer are considering how rising rates can actually benefit their portfolios. In this piece, I am suggesting that investors consider BDCs (Business Development Companies) in the current environment, whose lending operations can actually generate improving results as interest rates rise.

How Do BDCs Actually Benefit from Rising Rates?

The way BDCs generate income is by lending funds to, and investing in, private companies through equity, debt, and other mixed financial tools. A significant portion of the loans BDCs issue is attached to floating rates. This means that the interest on these securities is decided by underlying interest rates in the economy.

In fact, you will be surprised to hear that more than 80% of loans in BDC portfolios are linked to a floating rate, which directly means that BDCs are well-positioned to record rising interest income during a rising-rates landscape like the one we are currently undergoing.

However, there is a catch. BDCs have to borrow money to invest their money as well. If a BDC’s interest income increases due to its floating loans issued, but the interest paid on its own borrowings advances by an equally high amount, that’s no good. In other words, the desired effect of rising rates is not just increasing interest income but actually an expansion in the BDC’s net income margin.

Let’s consider two different examples.

This is Sixth Street Specialty Lending’s (NYSE: TSLX) net interest margin analysis from its latest Q3 presentation. As you can see, backed by rising interest rates, the company’s total yield on its debt investments has risen for three consecutive quarters. It now stands at a substantial 12.2%. However, as the graph illustrates, the company’s own cost of debt has been rising in the meantime at a swifter pace than the yield on its investments. The result? Sixth Street’s average income spread has failed to advance and even declined between Q2 and Q3 from 8.7% to 8.5%.

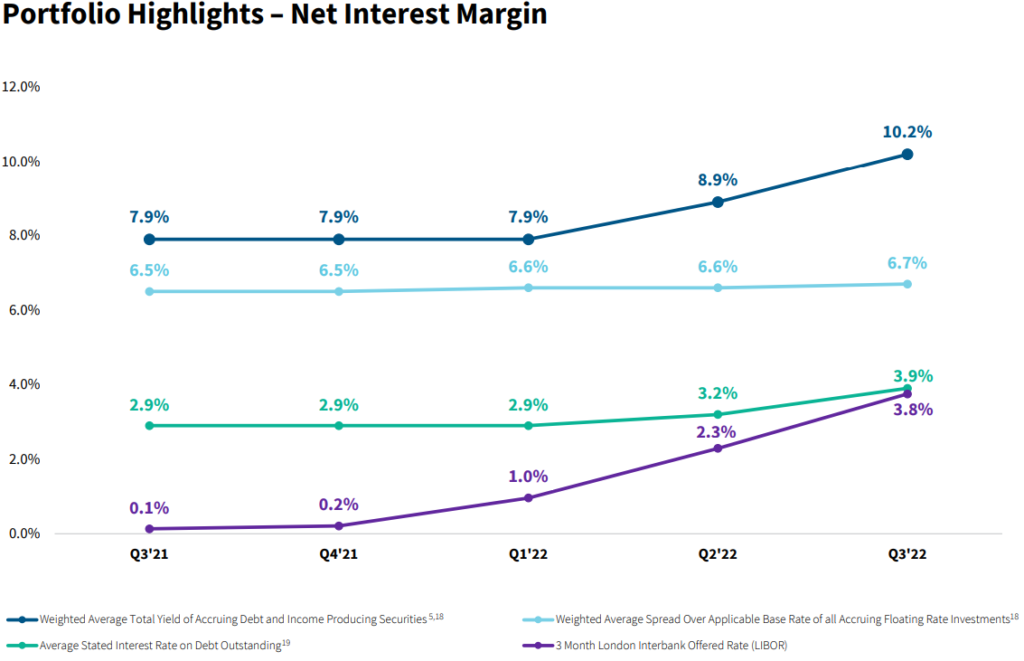

Then, here are Owl Rock Capital Corporation’s (NYSE: ORCC) equivalent metrics, taken from its Q3 earnings presentation. Similarly, with rising rates boosting the company’s earnings power, Owl Rock’s weighted average yield on its debt rose substantially. However, with Owl Rock’s own borrowing not rolling over to higher rates as fast, the company’s income spread has been actually going up. The year-over-year increase from 6.5% to 6.7% may seem insignificant, but a few basis points change can have a big impact on a BDC’s bottom line.

So what is the takeaway from this? You want to own BDCs that have borrowed at fixed, low rates and have issued loans at variable rates in order for them to profit from the expanding net interest margin resulting from rising rates.

BDCs Come With High Yields but be Mindful

BDCs are highly regulated. Due to their legal status, they are required to distribute over 90% of their profits to shareholders. They do this because, in return, they don’t pay corporate income tax on profits before distributing them to stockholders. The outcome of this is that most BDCs come with massive yields that usually hover in the high-single to low-double digits.

For illustration purposes, I have compiled a list including the majority of BDCs out there, along with their respective yields.

| Security name | Ticker | Dividend Yield |

| Ares Capital Corporation | ARCC | 9.02% |

| Barings BDC Inc | BBDC | 10.16% |

| Bain Capital Specialty Finance Inc | BCSF | 10.21% |

| Blackrock Capital Investment Corp | BKCC | 9.87% |

| Carlyle Secured Lending Inc | CGBD | 9.94% |

| Capital Southwest Corporation | CSWC | 10.73% |

| First Eagle Alternative Capital BDC Inc | FCRD | 9.80% |

| Fidus Investment Corp | FDUS | 7.06% |

| FS KKR Capital Corp | FSK | 12.68% |

| Gladstone Investment Corporation | GAIN | 6.37% |

| Golub Capital BDC Inc | GBDC | 9.22% |

| Great Elm Capital Corp | GECC | 19.38% |

| Gladstone Capital Corporation | GLAD | 8.25% |

| Goldman Sachs BDC Inc | GSBD | 11.49% |

| Horizon Technology Finance Corp | HRZN | 10.07% |

| Hercules Capital Inc | HTGC | 9.49% |

| Investcorp Credit Management Bdc Inc | ICMB | 16.74% |

| Main Street Capital Corp | MAIN | 6.76% |

| Monroe Capital Corp | MRCC | 12.21% |

| Metrovacesa SA | MVC | 5.45% |

| NEWTEK Business Services Corp | NEWT | 16.13% |

| New Mountain Finance Corp. | NMFC | 9.66% |

| Oaktree Specialty Lending Corp | OCSL | 9.33% |

| OFS Capital Corp | OFS | 10.28% |

| Owl Rock Capital Corp | ORCC | 10.26% |

| Oxford Square Capital Corp | OXSQ | 13.42% |

| Pennantpark Floating Rate Capital Ltd | PFLT | 9.97% |

| PennantPark Investment Corp. | PNNT | 4.84% |

| Prospect Capital Corporation | PSEC | 9.81% |

| Portman Ridge Finance Corp | PTMN | 11.35% |

| Rand Capital Corp | RAND | 3.05% |

| Saratoga Investment Corp | SAR | 9.13% |

| Stellus Capital Investment Corp | SCM | 8.05% |

| SLR Investment Corp | SLRC | 11.99% |

| BlackRock TCP Capital Corp | TCPC | 8.72% |

| Triplepoint Venture Growth BDC Corp | TPVG | 11.64% |

| Trinity Capital Inc | TRIN | 19.21% |

| Sixth Street Specialty Lending Inc | TSLX | 9.77% |

| WhiteHorse Finance Inc | WHF | 10.48% |

High yields can be quite attractive in the current environment, as they provide a margin of safety. Further, you have greater visibility in terms of what your future returns may look like. However, make sure that each respective dividend is well-covered.

Many companies in the space have been prudent, resulting in a lack of dividend cuts and even dividend hikes over time. Go check TriplePoint Venture Growth BDC Corp. (NYSE: TPVG); it’s a good example. Others have been overdistributing, resulting in a deterioration of their net asset value.

Thus, don’t be blinded by the limelight of ultra-high yields. It’s not always true, but chances are, the higher the yield, the riskier it is. Thus, try to find the sweet spot between high total-return prospects and the actual risk you undertake. Happy BDC hunting!