Recognizing the right stocks is a skill that every investor needs to learn, and the sheer volume of market data, on the main indexes, on individual stocks, on and from stock analysts, can present an intimidating barrier. Fortunately, there are tools to help. The Smart Score is a data collection and collation tool from TipRanks, using an AI-powered algorithm to sort the data on every stock according to a series of factors, 8 in all, that are known for their strong correlation with future share outperformance.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

That all sounds like a mouthful, but it boils down to this: a sophisticated data tool that gives you a simple score, on a 1 to 10 scale, to judge the prospects of any given stock. It puts the complex world of stock market data at your fingertips.

The Perfect 10, of course, should be a brilliant neon sign post guiding investors in for a closer look – and sometimes, it guides investors toward stocks that have never lacked for headline or notice. These are some of the market’s giants, stocks that are household names, feature trillion-dollar market caps, and boast Strong Buy consensus ratings from the Street’s best professional analysts. So, let’s give two of them a closer look.

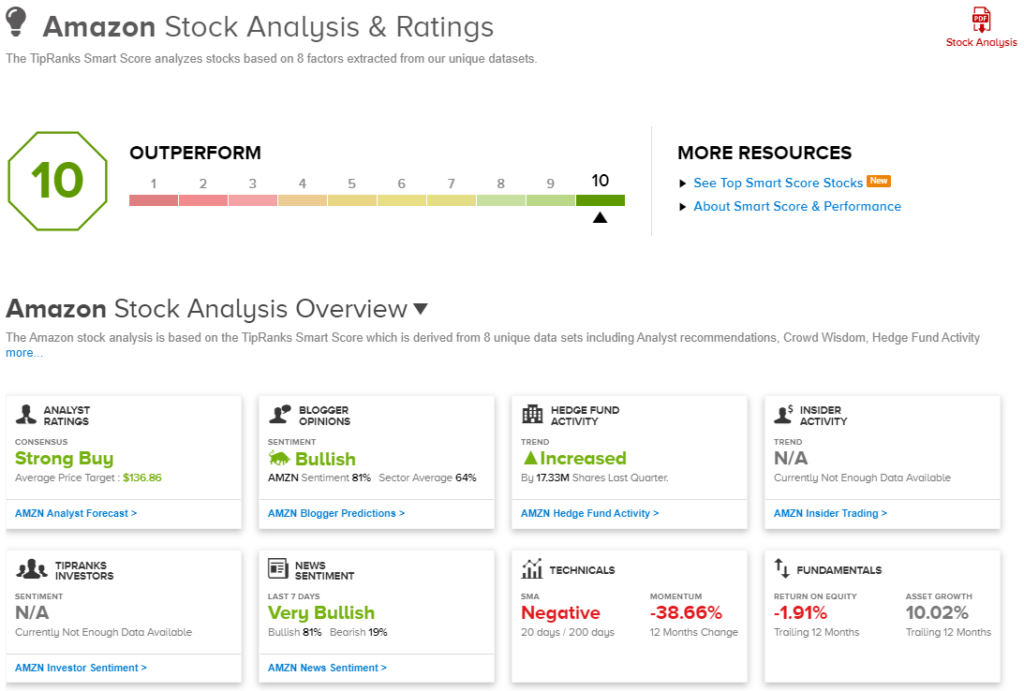

Amazon (AMZN)

First up on our list is Amazon, a name that doesn’t need much introduction. Chances are, we’ve all bought something from Amazon recently; the company is a giant among the world’s retailers – the second largest in the world – with a leading position in the e-commerce sector. In addition, Amazon’s cloud computing service (AWS) also holds a market-leading position.

Amazon’s gigantism in retail is complemented by its position among Wall Street’s publicly traded companies. It’s one of just four trillion-dollar-plus companies, when measured by market cap. Amazon’s $1.03 trillion in market cap puts it fourth place, behind #1 Apple, Microsoft, and Google-parent Alphabet.

As the leading e-commerce firm, Amazon benefited heavily during the pandemic/lockdown period – but it saw drastic losses last year, as the pandemic receded and business and social activities returned to more normal patterns. In 2022, Amazon’s share price fell by 51%, shedding well over $800 million in market cap.

More recently, Amazon has showed a tick up in sales. Total revenues for 4Q22 came to $149.2 billion, up 8.6% and above the $145.4 billion that had been expected. The company’s bottom line, however, missed the forecasts. On earnings, the company showed an EPS of 3 cents, comparing unfavorably to the expected 17 cents.

The revenue guidance for Q1 was set in the range of $121 billion to $126 billion, which would represent growth of 4% to 8% year-over-year; analysts had been predicted Q1 guidance of $125.1 billion.

Eric Sheridan, one of Goldman Sachs’ 5-star analysts, sees Amazon in a good position for further gains, with a series of catalysts providing support: “For AMZN shares, we still see the forward catalyst path dominated by a mixture of 1) bottoming of revenue deceleration dynamic for AWS; 2) continued proof points of a return to pre-pandemic levels of operating margins for its North America eCommerce operations and/or 3) stability vs. volatility in the consumption habits of the Amazon Prime household consumer in the coming quarters…. Longer term, we are unchanged in our long-term view of the potential for cloud computing (as evidenced by Amazon’s $110bn revenue backlog that grew +37% YoY.”

In Sheridan’s view, Amazon is worth a Buy rating – and his price target, of $145 implies that a one-year gain of 40% is coming up for AMZN shares. (To watch Sheridan’s track record, click here)

The big tech names typically gather plenty of Wall Street attention, and Amazon has 38 recent analyst reviews – breaking down 37 to 1 in favor of Buys over Holds for a Strong Buy analyst consensus rating. The stock’s average price target, $136.86, and trading price, $103.29, add up to 32.5% potential share appreciation in the next 12 months. (See Amazon stock analysis)

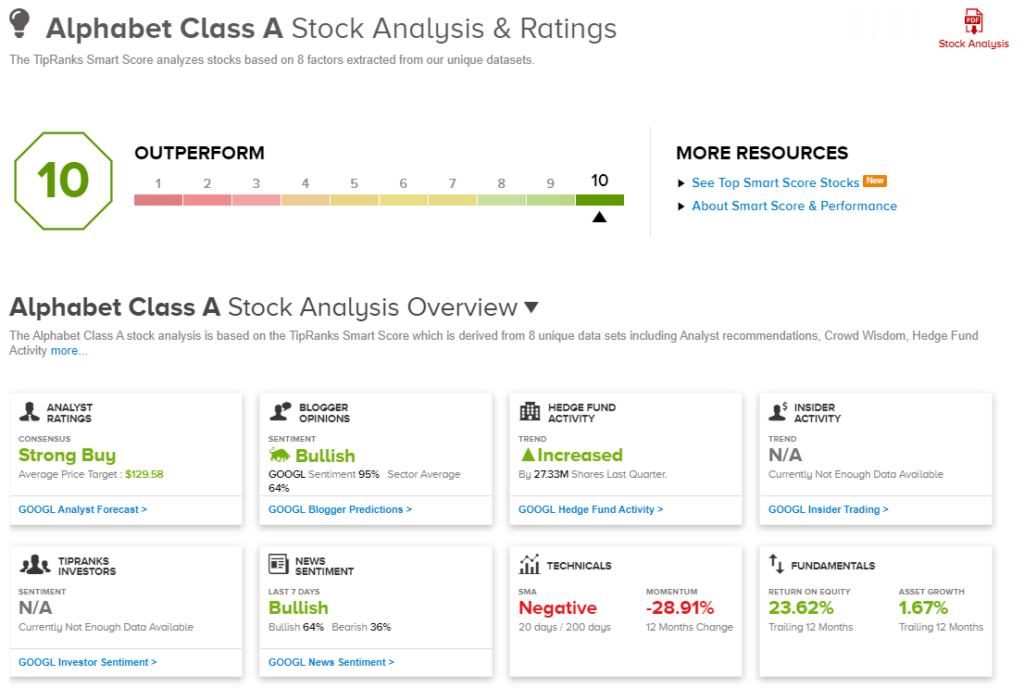

Alphabet, Inc. (GOOGL)

Next up is Alphabet, the parent company of Google. Alphabet holds the next rung up among public firms; its $1.3 trillion in market cap makes it the third-largest company on Wall Street. Alphabet is best known for its Google subsidiary, which has an iron grip on the lion’s share of the internet search business, and almost as large a share in online advertising.

Google may be the largest revenue driver for Alphabet, but the company has a slew of additional subsidiaries, giving it footholds in a variety of tech-oriented fields. The more high-profile of these include its ownership of DeepMind, in the AI field; Wing, the drone-based freight delivery service, and Waymo, an autonomous vehicle development enterprise.

Alphabet has felt some pressure recently, as its recently launched Bard AI has been perceived as inferior to its competition, primarily Microsoft’s Bing and the new ChatGPT. Long-term, however, the Google offering in AI has some important advantages. Based on the size and breadth of Alphabet’s subsidiary holdings, the company can draw on a deep well of data to feed the machine learning aspects of its AI.

On the financial side, Alphabet can rely on strong revenue performance and cash holdings. The company saw $76 billion at the top line in 4Q22, the last reported quarter, and finished 2022 with $21.8 billion in cash and cash equivalents. While the total revenue was in line with forecasts, the company’s Q4 EPS of $1.05 missed the expectations by 11%, or 13 cents. Even with those whiffs, Alphabet still pulled in a quarterly free cash flow of $16 billion.

Looking forward, BNP Paribas analyst Stefan Slowinski believes the company’s AI is the key to future performance, writing: “On the AI front, we expect Google to fight back and launch a string of generative AI supported services, while also turbo charging existing offerings… Google is best positioned given it has developed its own large language models since it acquired DeepMind 9 years ago (and is not dependent on a third party like OpenAI), has the best Search tool and data set, its own proprietary silicon since 2015, and user experience DNA.”

To this end, Slowinski gives GOOGL shares an Outperform (i.e. Buy) rating, while setting his price target at $123 for ~19% upside potential over the coming year. (To watch Slowinski’s track record, click here)

Overall, the Strong Buy consensus rating here is based on a unanimous 32 positive analyst reviews. Alphabet’s stock is priced at $103.73 and carries a $129.58 average price target, suggesting a gain of ~25% in the next 12 months. (See Alphabet stock analysis)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.