In just a few days, we’ll celebrate a new year, with a short break to watch the Old Year out and the New Year in, ending a marathon run of holidays that started with Thanksgiving. It’s a time to gather with family, catch our breath, and get ready to plunge back into the day-to-day business of ordinary life. And for stock traders, that means finding the best stocks to add to a profitable investment portfolio.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The markets put up a massive wall of raw data, all the information generated by thousands of traders dealing in thousands of stocks, conducting tens of millions of transactions every day – and that wall of data presents a powerful obstacle to the casual investor. It can take a lifetime to sort through it, to find the clues that highlight where to invest.

Fortunately, the data experts at TipRanks have created the Smart Score, an AI-based algorithm that uses a combination of machine learning and natural language processing to curate the volumes of data that the markets produce – and to present it in a form that investors can readily use. The Smart Score rates every stock against a set of factors known to predict future outperformance. The highest score, the Perfect 10, indicates shares that are strong, and ready to grow stronger.

So let’s use the Smart Score to pick out some stocks poised to perform in 2024. These Perfect 10s come with Strong Buy ratings from Wall Street’s analysts, who are also predicting double-digit upside for the coming year. Here are the details.

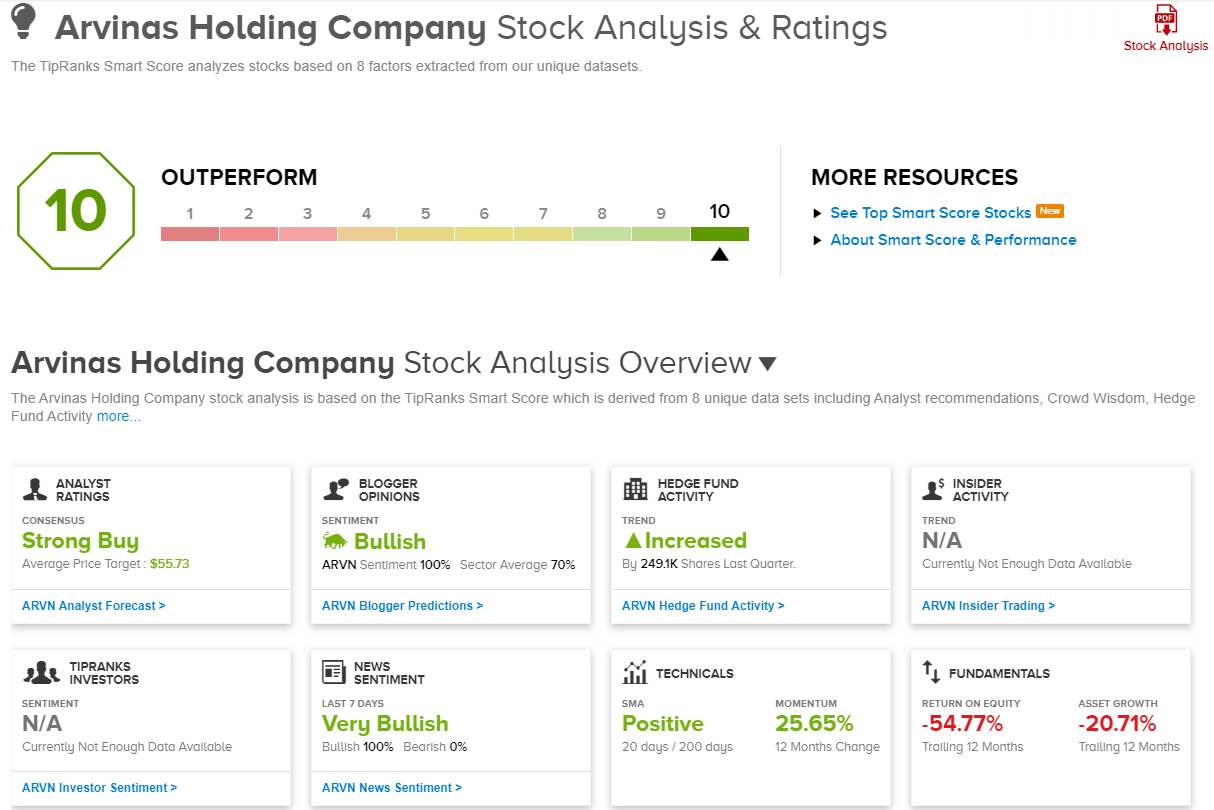

Arvinas (ARVN)

First up today is a biotech firm, Arvinas, a medical research company that is focused on the new field of protein degradation. Protein degradation is the process by which proteins are broken down at the molecular level and cleared out of living cells. Disruptions in this essential biological function have known links to multiple disease conditions, and recent work in the field is opening up novel opportunities for the discovery of therapeutic agents.

Arvinas is at the forefront of this new clinical research. The company has developed a proprietary line of proteolysis targeting chimeras – dubbed PROTAC – as protein degraders, designed to work with the body’s natural systems to efficiently target disease-causing proteins for degradation and removal at the cellular level. Working from this, Arvinas now has a pipeline of 12 projects, ranging from pre-clinical to late-clinical stages, of new drug candidates. The pipeline focuses mainly on oncology, but also has a neuroscience branch.

The leading program is vepdegestrant (ARV-471), an oncology drug under investigation in the treatment of ER+/HER2 breast cancer. This is an orally dosed PROTAC protein degrader, designed to target the estrogen receptor (ER) that has been validated as a driver of ER+ breast cancers. Vepdegestrant is currently the subject of two Phase 3 studies, as a monotherapy in the second-line setting in the VERITAC-2 trial, and in the first-line setting as a combo therapy with palbociclib in the VERITCAC-3 trial. A top-line data readout for VERITAC-2 is slated for 2H 2024.

The drug has already shown promise and the shares got a big boost earlier this month after the company announced positive data from a Phase 1b trial of the drug, as a combo therapy with palbociclib (ibrance), in the treatment of ER+/HER2 breast cancer.

Looking ahead, Wells Fargo’s Derek Archila is confident in the upcoming data readout for vepdegestrant. The 5-star analyst writes, “After a fairly quiet 2023 and with some less than ideal updates on execution, we are now within 12 months of a material potential catalyst for the company’s lead asset vepdegestrant. We believe the Phase 3 data for vepdegestrant monotherapy in ER+ breast cancer has a high POS of being positive and with shares trading at near cash, we think the risk/reward is highly favorable… Our $63 PT, represents a $2.5B enterprise value which we don’t think is unreasonable.”

These comments back up the analyst’s Overweight (Buy) rating on the shares, and that $63 price target points toward a one-year upside of nearly 53%. (To watch Archila’s track record, click here.)

The Strong Buy consensus rating on ARVN shares is based on 16 recent analyst reviews, with a 15 to 1 breakdown favoring the Buys over the Holds. The shares are trading for $41.09 and the $55.73 average target price suggests a 35.5% increase by the end of 2024. (See Arvinas’s stock forecast.)

Humana, Inc. (HUM)

Next on the list is Humana, one of the major health insurance providers operating in the US markets. This almost $56 billion company is consistently ranked in the top 5 of US health insurers, and has approximately 825,000 individual Medicare Advantage members enrolled in its policies. The company’s Medicare Advantage growth, of some 50,000 members over the course of 2023, was described as ‘meaningfully higher’ than the industry average.

Medicare Advantage is only part of the company’s business, although an important one. Plan offerings for seniors also include coverage for vision, dental, and hearing specialists. Humana offers comprehensive plans for dental and vision coverage in the individual markets, and customers can shop for these specialized policies in bundle packages as well. The company works with Medicaid as well, and is a major provider under the program. Medicaid services include determining eligibility and enrollment in appropriate programs.

In recent months, Humana has been in the news as the subject of a merger approach from the larger insurance company Cigna. The proposed merger would have created a $140 billion industry giant – but earlier this month, the talks collapsed. The companies were talking about a combination deal involving both cash and stock, but were unable to reach an agreement.

Turning to the financials, we should note here that Humana has posted sound revenue and earnings growth recently, and its last reported quarter – 3Q23 – beat the forecasts at the top and bottom lines. The company’s total revenue for Q3, over $26 billion, was up more than 16% year-over-year and beat expectations by $840 million. The bottom-line earnings, reported as a non-GAAP EPS of $7.78, came in 61 cents per share over the estimates. The company outperformed in its Medicaid and Primary Care business segments, driving the gains.

This health insurance stock has caught the eye of analyst Kevin Fischbeck, from Bank of America, who sees plenty of potential for Humana to keep growing: “We view HUM as the most dislocated name in our coverage. We see multiple ways for the company to get to $37 in EPS in 2025, despite market concerns that the ramp may be too steep. The reported M&A discussions between CI and HUM, have raised questions about whether HUM itself is concerned about its own growth outlook (or if CI walked away due to its own concerns), but given HUM is up 2.5x (and grown EPS at an 18% CAGR) since unsuccessfully agreeing to sell 8 years ago, it is difficult to argue that this management team only discusses a deal when its growth has peaked.”

Fischbeck goes on to explain that the falling-through of the Cigna deal reflects strength for Humana, writing, “We see HUM walking away from a deal as validation of the core growth story ahead of it, driven by continuing MA growth, a growing provider business and enterprise margin expansion. We see asymmetric risk/reward…”

Putting this together into a quantifiable stance, the analyst describes the stock as a ‘top pick’ and rates HUM shares as a Buy. His price target, a robust $640, implies a gain of 41% on the one-year horizon. (To watch Fischbeck’s track record, click here.)

Overall, Wall Street is willing to go bullish on this stock. There are 15 recent analyst reviews here, including 12 to Buy against 3 to Hold, for a Strong Buy consensus rating. Shares are trading for $452.80, and the $583.20 average price target indicates potential for a 29% gain in the coming year. (See Humana’s stock forecast.)

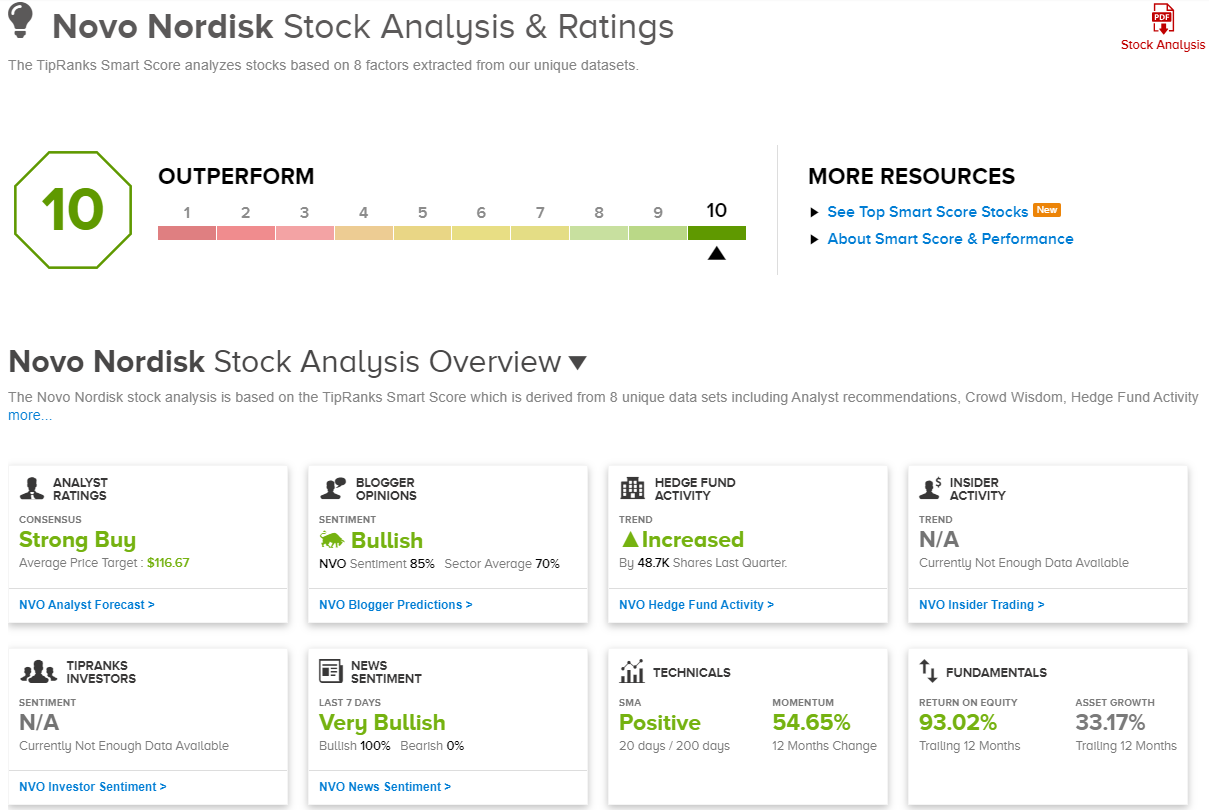

Novo Nordisk (NVO)

Last on our list today is another biopharmaceutical firm. This company, headquartered in Denmark, is primarily a commercial-stage operation, benefiting from a large portfolio of approved and marketable medications. Novo Nordisk is well-known for its involvement in developing treatments for diabetes, and in recent years the company has made strides in the obesity industry.

Obesity is a major health issue, contributing to conditions ranging from heart disease to high blood pressure to diabetes. According to the CDC data, approximately 42% of the US public is obese to some degree, and the prevalence of severe obesity is increasing at the fastest pace. More than 1 in 5 children, and 1 in 3 adults, are struggling with obesity-related problems, and the condition costs the US economy over $170 billion annually.

Novo Nordisk has two well-received weight loss drugs on the market, Saxenda and Wegovy, and with the company’s diabetes portfolio, these drugs led the firm’s sales through the first three quarters of 2023. Together, these portfolios saw a 36% y/y increase in sales, to 153.8 billion Danish kroner, (out of a total of 166.4 billion) or $23.07 billion in US currency. Within those gains, obesity care was up an impressive 167%, to 30.4 billion kroner for the 9-month period, or US$4.56 billion. The company’s strongest region was its North American Operations, which showed 46% y/y growth.

The strong performance of its weight loss and diabetes drugs led the company to raise it outlook for the full year. Previously, management had expected 27% to 33% y/y sales growth for 2023; the new guidance now is 32% to 38%.

All of this – but especially the obesity portfolio gains – has prompted Cantor Fitzgerald analyst Louise Chen to take an upbeat stand on NVO. She says of the stock, “We see the runway for obesity remaining attractive for years to come. It is already annualizing sales at >$10B, and we estimate this could grow to $100B over the next 5-7 years (~40%-60% CAGR). NVO should be an outsized beneficiary of this trend, given its leadership in what is currently a duopoly with LLY. Although there are many potential new competitors coming, NVO has much more data, established commercial infrastructure, and manufacturing capacity, making it hard for new players to catch up.”

To this end, Chen rates NVO as Overweight (Buy), and her price target, at $120, suggests the stock will appreciate by 17% in the next 12 months. (To watch Chen’s track record, click here.)

The Strong Buy consensus rating on this stock is unanimous, based on 4 positive analyst reviews on file. The stock is selling for $102.68 and its $116.67 average target price implies a one-year upside potential of 13.5%. (See Novo Nordisk’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.