Investors are always looking for a way to cut through the noise and get a clear view of any one stock’s main chance going forward. And that’s where a solid data parsing tool will come in handy.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

For that, there’s the Smart Score. This unique data collection and collation tool by TipRanks uses AI-powered algorithms to gather all of the information on thousands of publicly traded stocks – and then measure those stocks against a set of 8 factors, all known to line up with future outperformance. These 8 factors are then distilled together, giving each stock a simple, single-digit score on a scale of 1 to 10, with a ‘Perfect 10’ indicating a stock that deserves a closer look.

We’re going to give some Perfect 10 stocks just that closer look. Pulling up data from the TipRanks platform, we’ve three such stocks that are ticking plenty of boxes – and are getting plenty of love from the Wall Street analysts. Here are the details, along with relevant analyst commentary.

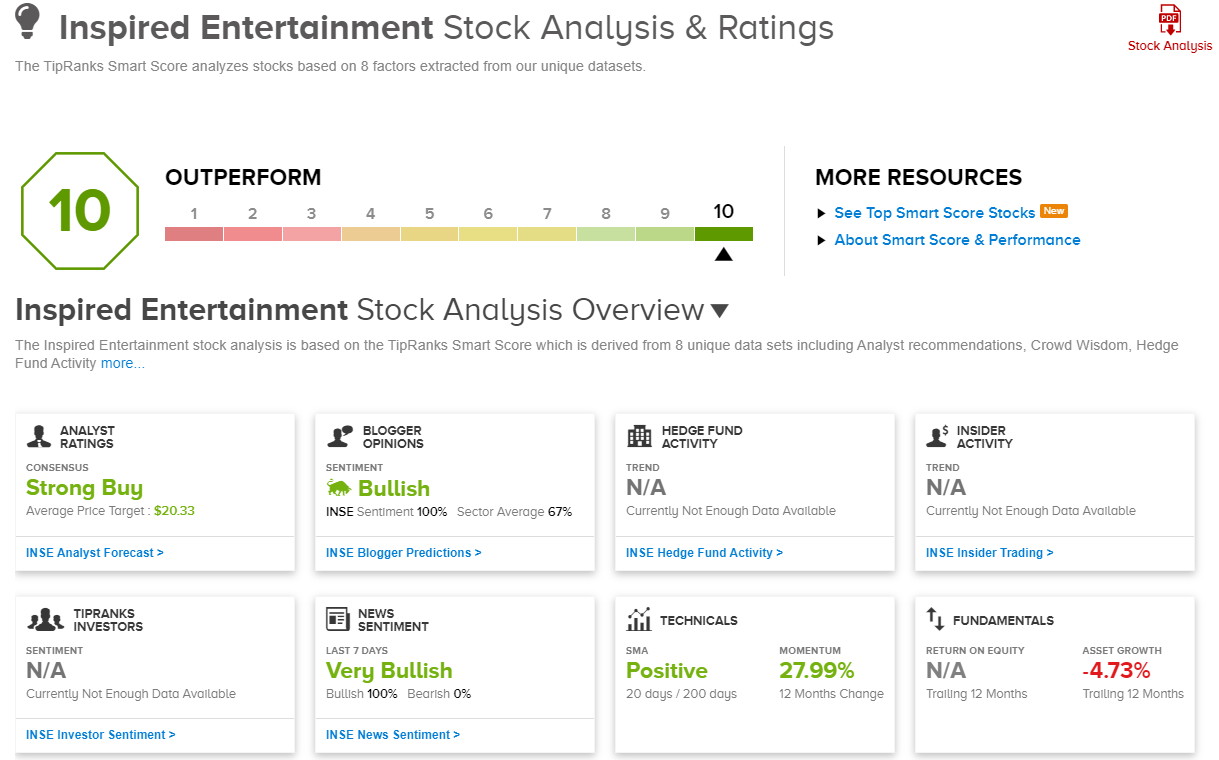

Inspired Entertainment, Inc. (INSE)

We’ll start with Inspired Entertainment. This global gaming tech firm offers a full portfolio of gaming technology products, including the content, platform, hardware, and services necessary for enterprise clients to bring gaming to their customers. Inspired works with land-based and mobile operators in the gaming, betting, lottery, social, and leisure sectors, offering cabinet games, virtual sports, and interactive games.

The company has an active presence in 35 jurisdictions around the world, and supplies the terminals and content for more than 50,000 gaming machines installed in pubs, betting shops, and gaming halls. More than 32,000 retail venues offer the company’s virtual sports, and Inspired’s digital games are available through more than 170 websites. In short, Inspired Entertainment has built itself into a major B2B creative and marketing force in the gaming industry.

Inspired Entertainment works diligently to maintain and expand its position. In just the last two months, since the end of Q1, the company has announced several expansionary moves. The first, in early April, was an agreement to launch premium iGaming content with Caesar’s Sportsbook & Casino in Pennsylvania. The second announcement, also in April, was a partnership with FanDuel to launch similar high-end iGaming content in Michigan. The most recent announcement, in May, was for a long-term contract extension as the Virtual Sports provider to Paddy Power, the owner of more than 600 betting shops in the British Isles.

These agreements all came after the end of 1Q23, and bode well for Inspired Entertainment’s future – not the recent past lacked success. Looking back to the quarter, we see that the company reported $66 million at the top line in 1Q23, beating the forecast by more than $2 million and growing 9% year-over-year. Likewise, adj. EPS of $0.13 beat the $0.08 expected by the analysts.

Turing to the Smart Score, INSE shows strong technicals, with a positive simple moving average (SMA) and solid 12-months-change momentum. The ‘Perfect 10’ score gets bigger support from two important sentiment measures. The financial bloggers – who are normally pretty fickle about their calls – are 100% positive on these shares, and the news sentiment also is 100% positive.

Watching this stock for Craig-Hallum, 5-star analyst Ryan Sigdahl sees plenty to like about Inspired. He writes, “INSE has a growing business and fundamental momentum, with strong demand for retail gaming in the UK, higher-margin online businesses with accelerating growth now represent 2/3 of EBITDA, and Leisure has visibility to improving trends going forward… INSE valuation implies a slow/no growth company with challenges, but to the contrary, there is growth, margin expansion, FCF and a lot of exciting new products launching.”’

In line with this position, Sigdahl rates the stock as a Buy, with a $20 price target that implies a 34% upside for the year ahead. (To watch Sigdahl’s track record, click here.)

There are only 3 recent analyst reviews on this stock, but all are positive – giving INSE a unanimous Strong Buy consensus rating. Shares are priced at $14.95 and the $20.33 average target suggests a 36% upside on the one-year timeline. (See Inspired Entertainment’s stock forecast.)

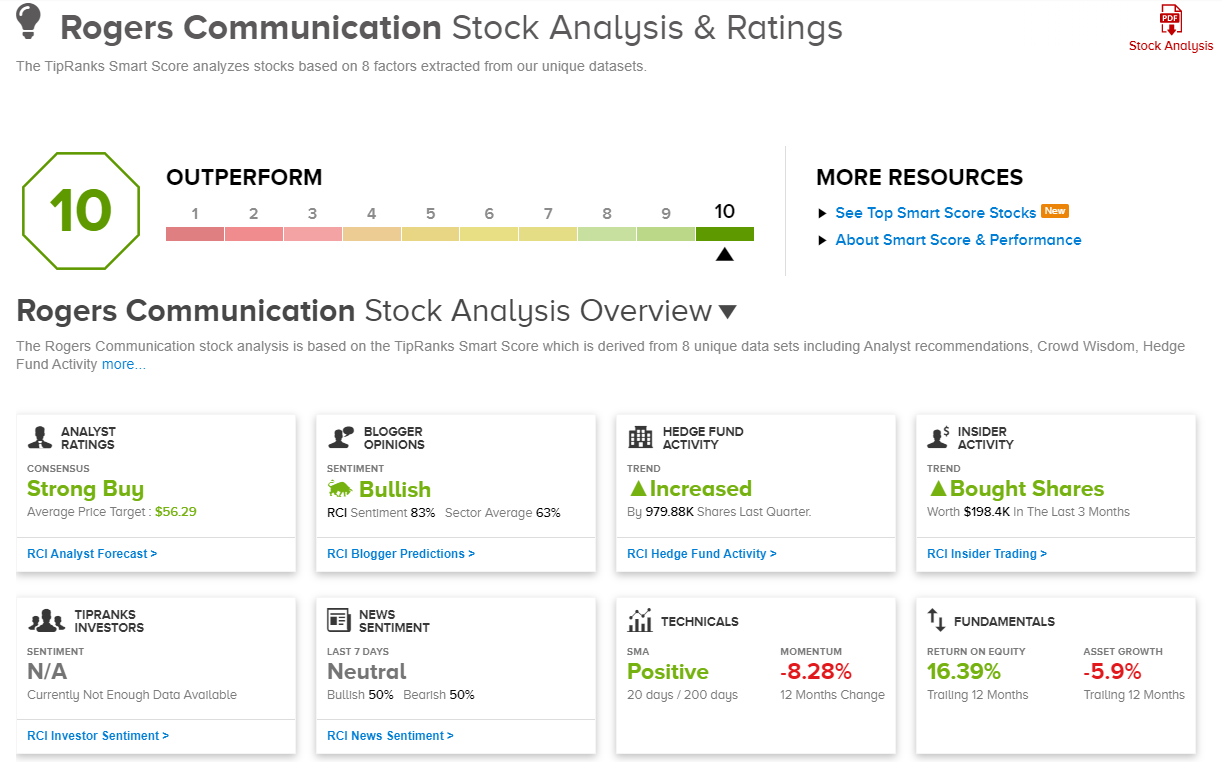

Rogers Communication (RCI)

For the second stock on our list, we’ll go north of the border to look at Toronto-based Rogers Communications. This Canadian telecom company provides wireless communications, cable TV, internet, and telephone services across Canada, and traces its origin to Ted Rogers’ first radio station purchase in 1960.

Today, Rogers Communications is a multi-billion enterprise with three main business segments. The company brought in $15.4 billion in Canadian currency last year, of which the majority, 59%, came from wireless operations. Another 26% of revenue came from cable operations, and 15% from the media segment. Rogers’ 2022 revenue was up 4.1% year-over-year.

Two months ago, at the beginning of April this year, Rogers announced a major development, the completion of its agreement to acquire Shaw communications. The agreement was first announced in March of 2021. Rogers purchased all of the outstanding Class A and B shares of Shaw at a price of C$40.50 per share, for a total of C$20 billion, and also took on C$6 billion of Shaw’s debt. The agreement will allow Rogers to expand 5G networks into Western Canada through a C$6.5 billion investment, and to create several thousand jobs in the Western Provinces.

In 1Q23, the last quarter before the Shaw agreement was completed, Rogers reported C$3.8 billion at the top line, amounting to a 5.8 y/y increase and beating the forecast by C$40 million. The non-GAAP EPS figure of C$1.09, also came in better than expected – by 13 cents.

The Smart Score finds support from the financial bloggers, who are 83% positive (as opposed to the 63% sector average), from the hedge funds, which are trending positive with purchases of 979,900 shares last quarter, and from the Crowd Wisdom, which is very positive and showed 11.5% increases in private portfolio holdings over the past 30 days.

This stock has caught the eye of Barclays analyst Kannan Venkateshwar, who points out the prospective benefits from the Shaw acquisition. “Post the Shaw deal, Rogers has the potential to expand its industry leading margins and invest it to grow wireless further while stabilizing its broadband business,” Venkateshwar explained. “Rogers has not been shy of disturbing the competitive equilibrium in the past. Therefore, we suspect industry concentration may not really change its competitive approach and it may choose to invest at least part of its deal synergies into a more aggressive go-to market positioning.”

Looking ahead, Venkateshwar gives the stock an Overweight (Buy) rating and a C$74 (US$55) price target, suggesting a 27.5% one-year upside potential. (To watch Venkateshwar’s track record, click here.)

Overall, RCI shares get a Strong Buy consensus rating from Wall Street’s stock analysts, based on 10 reviews that include 8 to Buy and 2 to Hold. Shares are currently trading for $43.11 and the $56.29 average price target implies a gain of 30.5% in the next 12 months. (See Rogers’ stock forecast.)

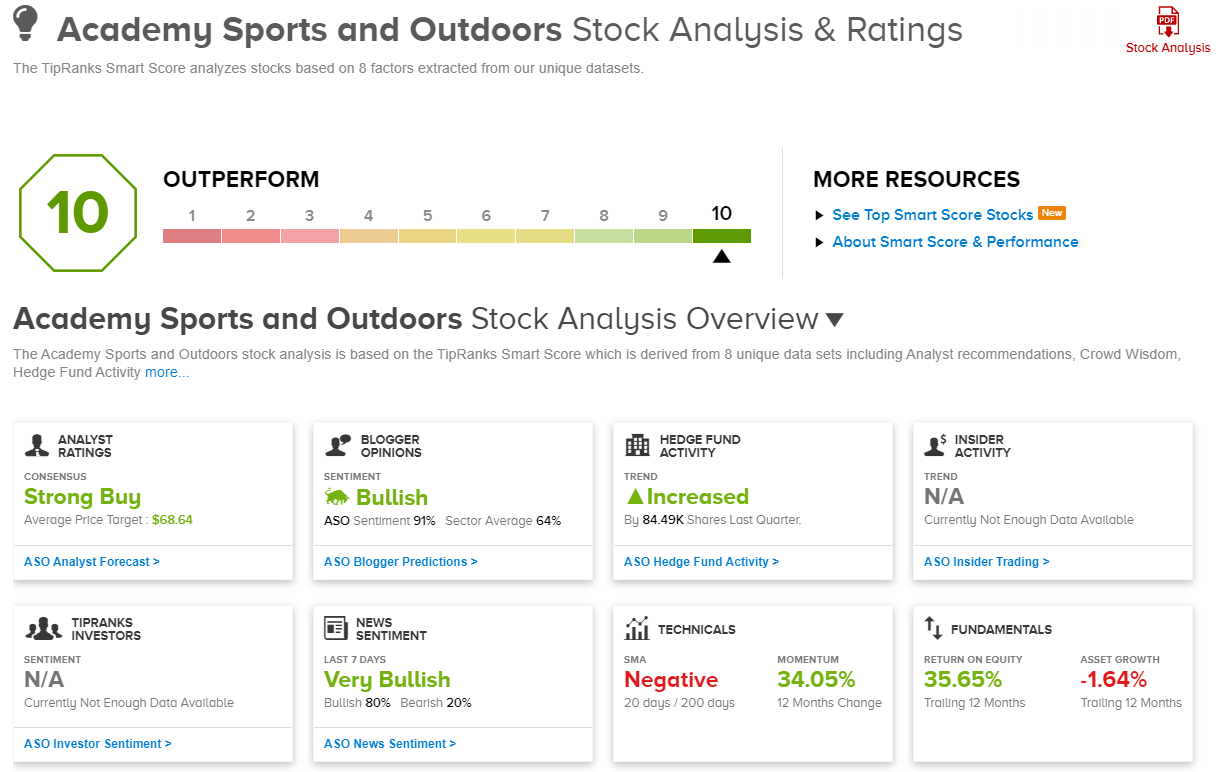

Academy Sports and Outdoors (ASO)

We’ll wrap up with Academy Sports, a chain-store operator in the sports and outdoor supply sector. Academy has been in business since 1938, currently operates 269 stores in 18 states, and describes itself as a provider of ‘fun for all.’ The company offers a wide range of products, in a wide range of categories, including apparel, footwear, outdoor, and sports & recreation. Academy’s shelves are stocked with both leading national brand-name products and private label items.

Academy saw strong sales in 2021, in the immediate aftermath of the COVID lockdowns, when people were looking for leisure activities that could fit with the social distancing strictures still in place. The company’s revenue that year hit $6.77 billion – but it slipped by 5.5% to $6.4 billion in 2022, as the economy reopened and the COVID restrictions were lifted.

Revenue slipped again in the recently reported quarter, for Q1 of fiscal year 2023. The figure came in at $1.38 billion, down 5.7% y/y, and missing the forecast by $60 million. The company’s bottom line, a non-GAAP EPS of $1.30, was 34 cents below expectations and was down 23% y/y.

Earnings misses from ASO, however, are a rare occurrence, and despite the lackluster results, the stock still holds a Perfect 10 from the Smart Score. The Score is backed up by strong purchases from the hedge funds, which bought over 84,000 shares last quarter, and by solid sentiment metrics: blogger sentiment is at 91% bullish, news sentiment is 80% positive, and the crowd wisdom shows a 6.4% increase in holdings for the last 30 days.

We can also look to 5-star analyst Brian Nagel, of Oppenheimer, who sees the stock’s current level as a buying opportunity. Nagel writes, “As we consider carefully recent, weaker-than-expected trends at Academy, we come away with the view that a disrupted, more-challenged, post-pandemic demand backdrop is masking meaningfully improved underlying sales and profit potential of a now stronger, more streamlined ASO business model. We recommend clients remain focused upon a still very depressed ASO share valuation and prospects for solidifying trends at the chain, over the next several quarters, as cyclical challenges abate.”

Nagel’s comments back up his Outperform (Buy) rating, and his $85 price target points toward a 68% upside in the coming year. (To watch Nagel’s track record, click here.)

The rest of the Street is backing ASO’s chances, too. There are 14 recent analyst reviews on the stock, with a 13 to 1 breakdown favoring Buy over Hold – for a Strong Buy consensus rating. The stock has a $68.64 average price target and a $50.42 trading price, implying a 36% one-year upside potential. (See Academy’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.