There’s no doubt, the bears have been in control of the market so far this year and the overall trend has been down. That said, last week, stocks were on the comeback trail in what amounted to the best performance across the board since November 2020.

Whether that turnaround can be sustained remains to be seen. Even if the bear market resumes, investors will be keen to find stocks that are primed for gains even as the broader markets retreat. That’s the key to success, but turning it will be no easy feat.

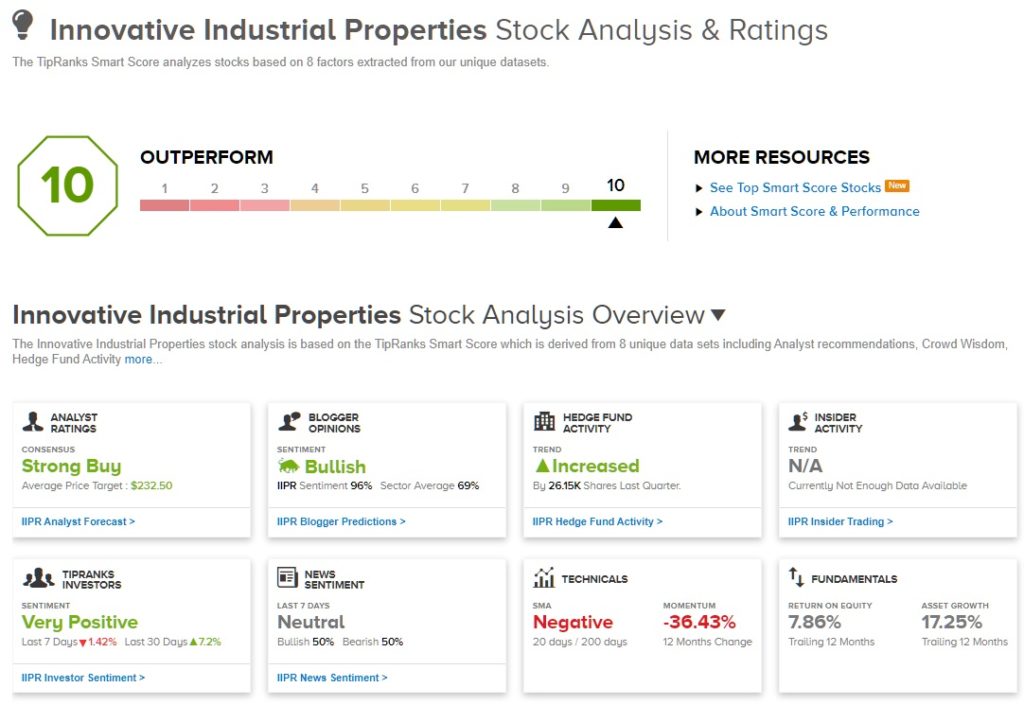

The Smart Score tool at TipRanks makes this search for the ‘right’ stock easy, by gathering and collating all the data on each publicly traded stock and running through a series of algorithms, to sort it according to 8 separate factors each of which is known to correlate with future overperformance. The result is a single number, a score, on a scale of 1 to 10, that indicates the likelihood of the stock’s near- to mid-term trajectory – and it’s easily spotted at a glance.

So let’s take that glance. Using the general TipRanks database in conjunction with the Smart Score tool, we’ve pulled up the details on 2 stocks that hit all the right notes – and that earn a ‘Perfect 10’ Smart Score. We’ll also look ‘under the hood’ on these stocks, to see just which of the 8 factors are informing their Smart Scores. Let’s get to it.

Innovative Industrial Properties, Inc. (IIPR)

We’ll start with a unique REIT – a real estate investment trust. Innovative Industrial Properties operates in US states that have legalized cannabis for medical and/or recreational use, and have established the regulatory apparatus to oversee this new business sector. As a REIT, Innovative owns, operates, leases, and manages a portfolio of cannabis-related properties, mainly industrial-grade greenhouses used as growing facilities in the medical cannabis sector. The company has a total of 64 properties across 19 states.

Innovative’s stock peaked in November of last year, and the shares have been slipping since. Year-to-date, IIPR is down by 55%.

Even as the stock has fallen, however, the company’s revenues have been rising. While sales fell off from 2020 going into 2021, the company has since posted 5 consecutive sequential quarterly gains. The most recent quarter, 1Q22, showed $64.5 million in total revenue. This was up 50% year-over-year and brought with it $1.32 in diluted EPS, although the bottom-line figure missed the analysts’ expectations of $1.36. Funds from operations, a key metric in the REIT field, came in at $1.86 per share.

That was all enough to support a solid dividend, paid out at $1.75 per common share in the first quarter and recently declared at the same amount for the second quarter. Innovative has raised the dividend 8 times in the past 12 quarters, to keep up with the mostly rising earnings and FFO figures.

And now we turn to the Smart Score, where Innovative boasts a Perfect 10. A look at the 8 factors shows that a stock can achieve the highest score even if some of the backing data is less than perfect. The technical factors, for example, are negative here. But that is outweighed by 96% bullish sentiment from the financial bloggers and from a significant increase in hedge fund holdings of IIPR in the last quarter.

Craig-Hallum analyst Eric Des Lauriers points out the basic fact that makes Innovative truly unique: that cannabis is still illegal at the Federal level, and that makes it difficult, even in states with legal regimes, for cannabis companies to secure capital funding for building projects. This puts Innovative, which can fund, or simply build, those projects at an advantage. Des Lauriers writes, “With no disruption to any rent payments, low tenant replacement risk, and with these facilities being absolutely ‘mission-critical’ to IIPR’s tenants, we come away from Q1 earnings more confident in the strength of the portfolio. We expect IIPR to maintain a brisk pace of capital deployment ($500-600MM/yr) and growth in AFFO, and with impressive lease terms likely to persist even beyond federal banking reform, we expect IIPR to return to a premium versus peers.”

The analyst’s unabashedly upbeat outlook supports his Buy rating on the stock, as does his $175 price target, which implies a 12-month upside potential of 47%. (To watch Des Lauriers’ track record, click here.)

Des Lauriers’ colleagues are in full agreement here; all 4 other reviews are positive, making the consensus view a Strong Buy. There are plenty of gains projected too; going by the $232.5 average target, the shares are anticipated to climb 95% higher in the year ahead. (See IIPR stock forecast on TipRanks)

Ciena (CIEN)

Now we’ll turn to the telecom sector. The second stock on our list, Ciena, is a provider of networking systems, services, and software to more than 1,700 customers around the world. In particular, the company boasts over 2,000 patents, an important asset in a field that depends on intellectual property. The company’s offerings include domain control and management, routing and switching, and intelligent automation.

Like many, this company’s stock has been hit hard this year, having lost 39% year-to-date, underperforming the main indexes’ sharp pullback.

The stock saw a particularly bad day earlier this month, when Ciena released its fiscal 2Q22 results. These results, for a fiscal quarter ending on April 30, showed $949.2 million at the top line, as compared to $833.9 in the year-ago quarter. This represents year-over-year growth of 13% but the figure came in just below the consensus estimate. Non-GAAP EPS fell in fiscal Q2, dropping from 62 cents per diluted common share to just 50 cents in the current report. In addition to falling y/y, EPS also missed the 54-cent forecast.

Even though Ciena’s recent performance was considered a disappointment, the company retains a ’10’ on its Smart Score. This is based on strong hedge fund purchases of CIEN in the past few months, along with 100% bullish sentiment from both the financial bloggers and the news media.

Mike Genovese, from Rosenblatt Securities, has delved into the workings of this stock, and comes out running with the bulls. He writes of Ciena, “For us, the bottom line is Ciena leads in an industry with very strong and sustainable demand drivers in a post-Covid world. The company has TAM expansion opportunities in Switching & Routing and Converged Metro and market share gain opportunities versus Huawei in EMEA and India. Ciena is taking an appropriately cautious, low 40s GMs view for the rest of FY22, but has margin expansion drivers in FY23 including price increases. The CFO says FY23 should be ‘very strong’ with revenue growth…”

Genovese also provides a Buy rating for these shares, and his price target of $70, indicates his belief in a one-year upside of 49%. (To watch Genovese’s track record, click here.)

Turning now to the Wall Street analyst consensus, Ciena holds a Strong Buy rating, based on a lopsided 13 to 2 split between the Buy and Hold reviews. Shares in Ciena are selling for $46.94, while their $69.67 average price target suggests that the stock might jump some 48% before the end of this year. (See Ciena’s stock forecast at TipRanks.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.