Recognizing the right stocks is a skill that every investor needs to learn, and the sheer volume of market data, on the main indexes, on individual stocks, on and from stock analysts, can present an intimidating barrier. Fortunately, there are tools to help. The Smart Score is a data collection and collation tool from TipRanks, using an AI-powered algorithm to sort the data on every stock according to a series of factors, 8 in all, that are known for their strong correlation with future share outperformance.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

That all sounds like a mouthful, but it boils down to this: a sophisticated data tool that gives you a simple score, on a 1 to 10 scale, to judge the prospects of any given stock. It puts the complex world of stock market data at your fingertips.

The Perfect 10, of course, should be a brilliant neon sign post guiding investors in for a closer look – and sometimes, it guides investors toward stocks that have never lacked for headline or notice. These are some of the market’s giants, stocks that are household names, feature trillion-dollar market caps, and boast Strong Buy consensus ratings from the Street’s best professional analysts. So, let’s give two of them a closer look.

Microsoft Corporation (MSFT)

First up on our list is Microsoft, one of the best-known brand names in the world – and also the second-largest publicly traded company in the world, with a market cap of $1.78 trillion. Microsoft got its start back in the mid-70s, and was part of the initial expansion of the personal computer tech revolution. The company rose to prominence when its Windows operating system became the industry standard, still used today, for the majority of all personal computing.

Today, the company is adapting successfully to the growing cloud computing environment, offering products such as Office 365, which brings the Office applications for home, school, and small business use onto the cloud; Dynamics 365, which does the same for business applications; and the Azure platform to support cloud computing operations. At the same time, the company maintains service and support for its more modern Windows operating systems.

In the last reported quarter, Q1 of fiscal year 2023 (September quarter), Microsoft reported $50.1 billion at the top line. This translated to a 10% increase year-over-year, and beat the $49.6 billion forecast. The solid result came on the back of a 24% reported increase in cloud revenue, to $25.7 billion, or slightly more than half of the total.

On the negative side, the company reported a y/y drop in net income, by 14% to $17.6 billion, with the diluted EPS falling 13% to $2.35 per share. The real hit for investors came from the company’s fiscal Q2 guidance, which was set at $52.35 billion to $53.35 billion, or up 2% at the midpoint. This was, however, below the $56.05 billion analysts had wanted to see – and the stock fell after the earnings release.

Morgan Stanley’s Keith Weiss, however, remains bullish on the company’s prospects. The 5-star analyst writes, “While investors worry forward numbers have not been de-risked, we see a strong (and durable) demand signal in the commercial businesses, which should lead to improving revenue and EPS growth in 2H23…. The strength of Microsoft’s positioning across key secular growth segments remains unchanged. Mix shift toward faster growing Azure and Dynamics 365 and relatively durable Office 365 growth (in constant currency) help support management’s goal of 20% constant currency growth across its Commercial businesses.”

In Weiss’s view, Microsoft’s potential fully merits its Overweight (Buy) rating, and his $307 price target implies a one-year upside potential of 29%. (To watch Weiss’s track record, click here)

Overall, Microsoft stock has picked up 27 recent ratings from Wall Street’s analysts, a total that includes 25 Buys against just 2 Holds – for a Strong Buy consensus rating. The shares are priced at $238.73, and their average target of $291.34 suggests a 22% gain on the one-year time horizon. (See MSFT stock analysis on TipRanks)

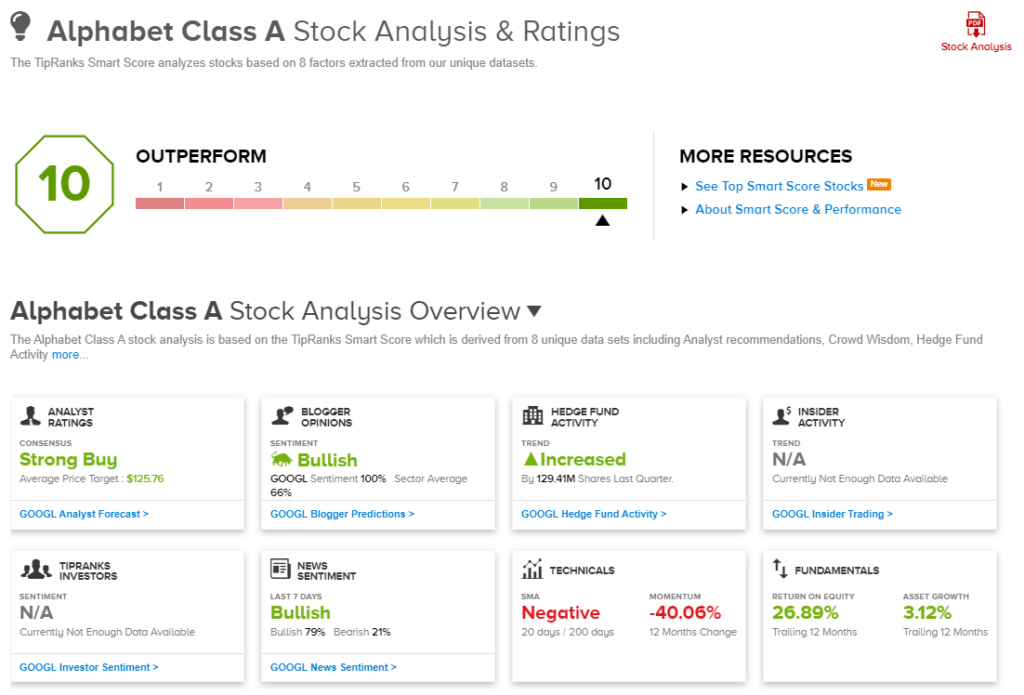

Alphabet, Inc. (GOOGL)

Next up is Alphabet, the parent company of Google, that everyone knows. The world’s largest search engine is part of an overall firm that boasts a $1.16 trillion market cap, making it the third largest publicly traded firm, after Microsoft and Apple. Alphabet isn’t just Google; the company also owns the Android OS, the popular YouTube website, and is even moving into the autonomous vehicle niche through its Waymo subsidiary.

While Alphabet remains near the top of the global tech industry, the recent 3Q22 showed some cracks that will need to be addressed. For the most part, these are related to general economic conditions, particularly shrinking advertising budgets in the online industry. The company’s Q3 results showed total revenues of $69.09 billion, up 6% year-over-year – but that modest growth represents a distinct deceleration from the prior year’s 41% growth rate, and it missed the $70.5 billion forecast. Operating margins also fell, from 32% one year ago to 25% in the last quarter; operating income was down 18% to $17.13 billion.

The miss in revenue was exacerbated by a large miss in YouTube’s top line. Advertising revenue on the video site came in at $7.07 billion, missing the $7.42 billion forecast by a 4.7% margin.

While there are serious headwinds facing Alphabet/Google, we should not underestimate the company’s clear strengths. Google remains the internet’s premier search engine, and Google Search accounted for more than $39.5 billion of the total revenue. And, despite the pullback in overall online advertising, Google Ads saw revenue’s absolute numbers grow by $1.3 billion y/y, to $54.4 billion (a total that includes Google Search’s gain, as well as the pullback in YouTube advertising). Finally, the company boasts deep pockets, with over $21.9 billion in cash assets on hand. In short, Alphabet has both the market position and the resources to weather a storm.

Mark Mahaney, 5-star analyst with Evercore ISI, is cognizant of GOOGL’s difficulties in the online ad segment going forward. Yet, while he predicts short term pain he also sees longer term gain: “For now, we estimate GOOGL’s organic revenue growth deteriorating further to 6% Y/Y in Q4, before beginning to recover sometime in ‘23. But after the Macro and the FX and the Comps, we strongly believe GOOGL will re-emerge as the broadest, strongest global ad revenue platform, with a dramatically profitable business model, notable diversification into Cloud Computing, and substantial long-term option value with Waymo.”

Quantifying his stance on GOOGL, Mahaney rates it as Outperform (a Buy) for the year ahead and backed by a $120 price target that implies a 34% upside potential from current levels. (To watch Mahaney’s track record, click here)

All of Mahaney’s colleagues agree with his thesis. GOOGL shares score a unanimous Strong Buy consensus rating, based on 29 recent positive analyst reviews. The stock’s average price target, $125.76, indicates potential for 41% growth from the current trading price of $89.23 over the coming year. (See GOOGL stock analysis on TipRanks)

Stay abreast of the best that TipRanks’ Smart Score has to offer.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.