Making the right decision in the investment market is no easy task. What investors need here is a way to cut through the noise, take the raw flood of stock data, and reduce it to a pattern, a usable information point that can indicate potential winners in the markets. This is where the TipRanks Smart Score comes in, a data tool that fills exactly this niche.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The Smart Score takes the gathered data from the stock market, and puts it to work, collating it into categories and rating every stock by a series of 8 factors. Each factor is known to correlate with positive performance. Through the Smart Score algorithm, all 8 factors are taken together and distilled into a single score, on a scale of 1 to 10, that gives a clear signal for investors.

Now combine that with the classic defensive posture for a time of market instability, the dividend stock. High-yield dividends offer a measure of protection from market downturns and inflationary economic environments, making them a popular choice for defensive minded investors.

We’ve opened up the platform to locate stocks that offer the best of both worlds – a ‘Perfect 10’ from the Smart Score, and a dividend yielding over 7%. Are these the right stocks to go all-in? A look at the data and the analyst commentary will point us toward an answer.

Chord Energy (CHRD)

The first ‘perfect 10’ stock we’ll look at is Chord Energy, a mid-cap company in the hydrocarbon exploration sector. This company operates in the Williston Basin of North Dakota and Montana where it focuses on organic drilling activity and horizontal fracking to release crude oil reserves. Chord is a top producer in the Williston, and in 3Q22 generated 172,500 barrels of oil equivalent daily.

Strong production has led to rising revenues. Chord brought in a total of $1.19 billion at the top line in Q3, up some 50% sequentially and an impressive 196% year-over-year. On the bottom-line, at $7.20 per diluted share, the figure more than doubled the $3.16 diluted EPS reported in 3Q21. However, it came in below the $8.35 forecast.

In cash assets, Chord reported a net income from continuing ops of $941.6 million, and $783.6 million in net cash from operations. The company’s cash balance, as of September 30, was $658.9 million; this exceeded the company’s $400 million debt.

The solid balance sheet allows Chord to engage in a strong capital return program for investors. The company bought back 1.2 million shares in the third quarter, for a total of $125 million, and declared a base-plus-variable dividend to common shareholders. The declared dividend, of $3.67 per share, includes a $1.25 base and a $2.42 variable. The base dividend annualizes to $5 and yields 3%; with the variable, it annualizes to $14.68 and yields a more robust 9.3%.

This stock has caught the attention of 5-star analyst Neal Dingmann, from Truist, who writes, “We forecast Chord to continue to be the mid-cap E&P shareholder leader with total percent payout rivaling any of the largest producers…. CHRD’s FCF deployment strategy has levers to return cash flow back to its shareholders resulting in the recently declared variable dividend of $3.67/sh. We believe there is additional room for CHRD to continue with a sustained share buyback plan consisting of a base dividend of at least $1.25/sh and potentially higher than the above-mentioned variable dividend. Further, while the company’s $125MM in 3Q22 buybacks was opportunistic, we fully anticipate this program to continue well through 2023.”

Dingmann’s comments back up his Buy rating on the stock, while his $214 price target implies a 38% upside in the next 12 months. (To watch Dingmann’s track record, click here)

Chord Energy has 5 recent analyst reviews on file, and they are unanimously positive for a Strong Buy analyst consensus rating on the stock. The average price target here is $197.60, suggesting a 27% upside from the current trading price of $155.05. (See CHRD stock analysis on TipRanks)

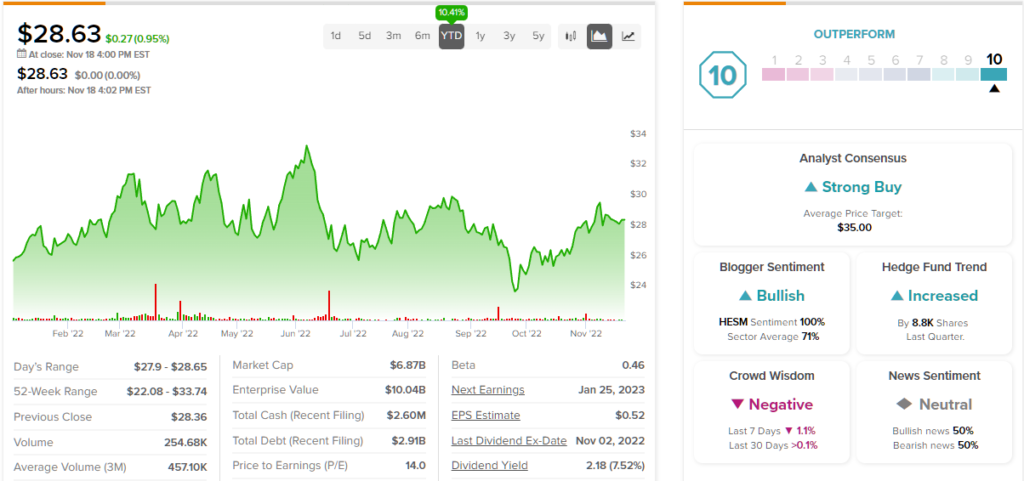

Hess Midstream Operations (HESM)

Next up is a midstream company, Hess, another operator in the Williston Basin. Where Chord, above, is a production company, however, Hess works in the transport of hydrocarbon products from wellhead to distribution points – the midstream sector. Hess’s assets include gathering pipelines for crude oil, natural gas, and water, along with a variety of natural gas and crude oil plants processing and storage, and terminal facilities for export.

Hess saw a jump in volume during 3Q22, and that was reflected in the company’s financial results. Top line revenues came to $334.8 million, up 10% year-over-year, and drove a net income of $159.4 million, while net cash from operations reached $234.7 million. At the bottom line, the net income attributable to Hess Midstream Partners LP came to $23.2 million, or 53 cents per share. The EPS value was up 39% y/y.

In October, the company declared its dividend at $0.5627 per common share for Q3. This was up a modest 1.2% from Q2, and up 5% from the year-ago period. On an annualized basis, the dividend pays $2.25 per common share and yields 7.9%. The dividend was last paid out on November 14.

In coverage of Hess Midstream for JPMorgan, analyst Jeremy Tonet finds the company in a solid position to bring returns to investors. He writes, “HESM possesses solid long-term, fee-based contracts underpinned by MVCs and built-in fee recalculation mechanisms to offset any volume deficiencies. Producer sponsor HES holds an extensive position in the core of the Bakken with a deep drilling inventory and plans to grow production to ~200 mboed (and stabilize thereafter). HESM has shown consistent dedication to returning cash to shareholders via both sponsor unit repurchases and a commitment to ~5% per annum distribution increases through at least 2024.”

Going forward from this stance, Tonet rates the shares as Overweight (a Buy), and sets a price target of $34 to indicate a 19% upside potential going into next year. (To watch Tonet’s track record, click here)

This mid-cap midstreamer has picked up 3 reviews from the Street’s analysts and they are all positive, supporting a Strong Buy consensus rating on the stock. HESM has a current price of $28.63 and an average price target of $35, for a 22% upside potential in the next 12 months. (See HESM stock forecast on TipRanks)

Stay abreast of the best that TipRanks’ Smart Score has to offer.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.