It’s safe to say that tech has been on the up recently. The spread of artificial intelligence (AI) has lit a fire under investors, and tech stocks have rallied some $4 trillion this year. The NASDAQ index, which is tech-heavy to begin with, gained 2.5% last week, and is up almost 25% since the onset of 2023, marking a turnaround from 2022’s bear market. By comparison, the S&P 500 is only up 9%, and the Dow has slipped slightly.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The biggest winner in the tech rally so far is Nvidia. The company is seen as one that stands to benefit immensely from AI’s rise, and it has gained accordingly. The shares are up by more than 165% year-to-date, putting the semiconductor giant on track to become the first trillion-dollar chip company.

But Nvidia, for all its dominance, is hardly the only tech game in town. Investors can find plenty of other stocks that are ready to ride this tech rebound to success. We’ve used the TipRanks Smart Score to locate two such stocks – equities that have earned the ‘Perfect 10’ rating from the data sorting tool. A Perfect 10 from the Smart Score shows that a stock rates high in a set of 8 factors known to correlate with future outperformance; these Perfect 10 tech firms are shares that truly stand out in a field of rising stocks. So, let’s check the details.

monday.com (MNDY)

First up is monday.com, a software company offering cloud-based products to enterprise customers, for use in work management, office system optimization, CRM, marketing, sales ops, and project management. The company’s products, offered on a subscription model, streamline office workflows by connecting people and systems, allowing for more efficient processes. Monday can boast some big names in its customer base, including Uber, Coca-Cola and Canva.

By the numbers, we can see just how quickly Monday has grown. The company was founded in 2012, and held its IPO in June of 2021; today, the firm employs more than 1,500 people, has over 186,000 customers using the products, and can claim nearly 1,700 customers generating more than $50,000 each in annual recurring revenue. The company has a market cap of $7.98 billion.

In an important move that offers promise to expand monday.com’s customer base, the company announced on May 24 a new partnership with Microsoft. The joint effort will make monday.com’s CRM sales tools available on Microsoft Teams.

In addition, this past April, monday.com announced a new ‘work operating system’ that will allow users to build new process tools with generative AI incorporated from the ground up. The new tools will include email composition and rephrasing, automated task generation, and task summarizing.

Even on its own, monday.com has built up a significant business, bringing in some $519 million in total revenue last year. Since the IPO, monday.com has seen constant sequential revenue growth. In its last reported quarter, 1Q23, the company had a top line of $162.26 million, up 49.6% year-over-year and beating the forecast by just over $7 million. At the bottom line, monday.com had a non-GAAP EPS of 15 cents, 43 cents better than had been expected.

Even better, for investors, was the company’s Q2 guidance. Monday.com expects to see total revenue for the second quarter of this year in the range of $168 million to $170 million, well ahead of the consensus forecast of $165.3 million.

Turning to the Smart Score, we find that monday.com scores high on measures of sentiment. The blogger sentiment, which is 66% positive for peer firms, is 91% positive for MNDY; the crowd wisdom is ‘very positive,’ with individual investors increasing their holdings in MNDY by 7.5% in the last 30 days; and the hedges tracked by TipRanks bought up over 90,000 shares last quarter. Finally, the company shows solid positive momentum, and a positive simple moving average. That all adds up to a Perfect 10.

This stock has caught the eye of Goldman Sachs analyst Kash Rangan, who likes the company’s growth prospects. The 5-star analyst writes, “As gross churn remains stable and the macro pressure is concentrated in slower expansion rates, Monday.com is well positioned to see healthy re-acceleration in an economic recovery, in our view. New product rollouts and enhancements, such as that of MondayDB, CRM sales and generative AI further improve Monday’s position as a viable strategic, enterprise-grade software company. We view MNDY as posed to reach $2bn in revenue, rivaling the scale of Atlassian’s Cloud business. Given this commands the majority of their ~$37bn market value, we see a compelling risk/reward for MNDY.”

Rangan goes on to give MNDY shares a Buy rating, with a $240 price target to imply a 43% upside for the coming year. (To watch Rangan’s track record, click here)

Overall, monday.com’s Strong Buy consensus rating is supported by 13 recent analyst reviews, including 11 to Buy and 2 Hold. The shares are selling for $167.20 and the average price target of $188.92 suggests a gain of 13% on the one-year horizon. (See MNDY stock forecast)

Allegro MicroSystems (ALGM)

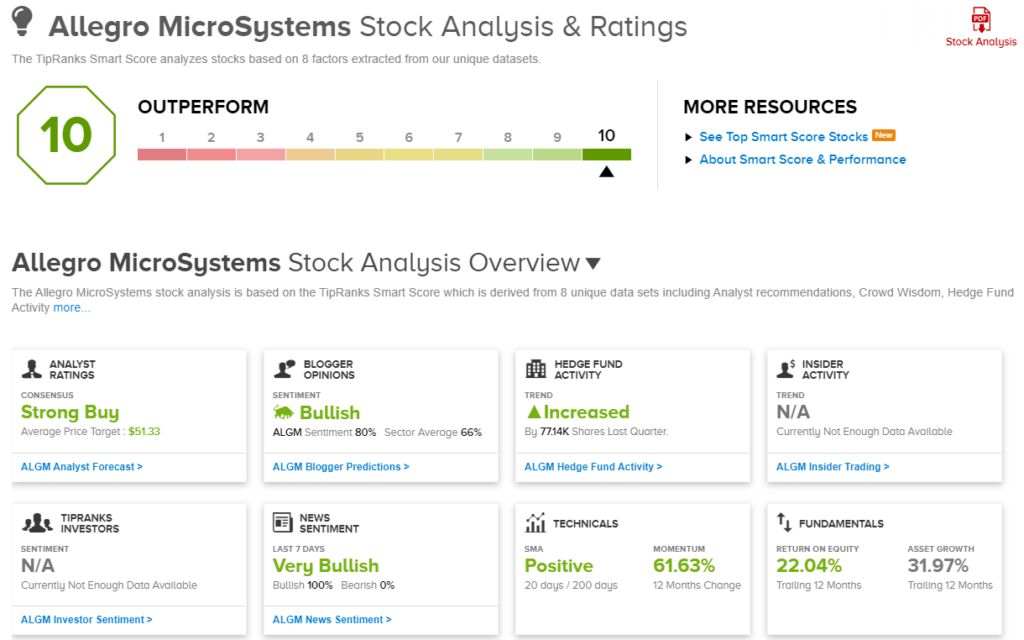

Next up on our Perfect 10 list, a semiconductor chip company, Allegro MicroSystems. Allegro is a fabless chip firm, meaning it designs and markets its chips, while outsourcing the manufacturing to third-party chip foundries. Allegro’s chips are used in a variety of applications, including the automotive and industrial tooling sectors, data centers, and green energy products. In these applications, Allegro’s products act as regulators, sensors, and motor drivers, and are popular in the electric car segment, where they are frequently found in AV control systems.

Allegro gets even more impressive when we look into some numbers. The average automobile typically contains 9 of the company’s devices, and Allegro has more than 650 active US patents protecting its intellectual property. Overall, Allegro has shipped more than 11 billion sensors in its lifetime.

Allegro’s revenues have been sequentially rising for the past year and a half and that was the case again in the company’s last quarterly report, for Q4 of fiscal year 2023 (March quarter). Allegro reported a 34% y/y increase in total revenue, from $200.29 million to $269.44 million, in turn beat the forecast by $4.43 million. For the full fiscal year 2023, the company saw a 26% y/y gain, and reported a record $974 million at the top line.

Drilling down to the bottom line, Allegro reported a Q4 non-GAAP EPS of 37 cents. This compared favorably to the 21 cents reported in the year-ago quarter, and came out 1 cent ahead of the estimates.

Looking ahead, Allegro published fiscal Q1 revenue guidance in the range of $270 million to $280 million, well above the consensus outlook of $257 million.

On the Smart Score front, Allegro shows a 22% return on equity for the last 12 months, and positive technical factors. The news sentiment is 100% positive, and the blogger sentiment is 80% positive. The crowd wisdom is very positive, based on holding increases of 14.6% in the last 30 days. The hedges are also bullish, and increased their holdings here by 77,100 shares last quarter.

Wells Fargo analyst Gary Mobley sees several reasons to back this stock. He writes, “ALGM’s strong growth in rev, relative to the rest of the chip sector, is being driven by: 1) the company’s relatively high (@ ~70%) exposure to automotive & the resilience in this end market; 2) share gains in power IC (e.g. motor control and PMICs); 3) share gains in Industrial (for both power ICs and magnetic sensors); and 4) improved manufacturing availability with fab partners like UMC, TSMC & Polar.”

“ALGM is one of the purest ways to invest in automotive themes, in our view,” the 5-star analyst goes on to add. “Additionally, we think ALGM offers a good trade-off between cyclical growth, secular growth (e.g., EV/ADAS), and valuation.”

In-line with these comments, Mobley rates the shares as Overweight (a Buy) and sets his price target at $52, indicating confidence in a 31% one-year upside potential. (To watch Mobley’s track record, click here.)

The analyst consensus view on Allegro shows that the bulls are running here; the stock gets a unanimous Strong Buy, based on 6 positive reviews. The shares have an average price target of $51.33 and a current trading price of $39.73, giving a one-year upside of 29%. (See ALGM stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.