Finding the right stocks is the real challenge for investors, but mastering that challenge is the path to success. The sheer amount of data generated by the markets – from thousands of traders, dealing in thousands of stocks, with millions of shares changing hands every day – makes a steep wall to climb. But getting through that wall of data is essential to building a profitable portfolio.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

That’s where the TipRanks Smart Score comes in, a data collection tool powered by an AI-driven algorithm. Smart Score gathers the market data and collates it according to a set of factors, eight in all, that are known to match well with strong share performance. Each stock is given a score, distilled from its comparison to the various factors and shown as a single number on a scale of 1 to 10. The ‘Perfect 10’ indicates a stock that deserves a closer look.

The Smart Score is a solid guide, and when it lines up with analyst ratings on the stock, it’s a clear signal for investors not to overlook it. We’ve gotten a start on this, looking up the data on 2 top-rated stocks that have also earned the Smart Score’s Perfect 10. Here are the details, from the TipRanks databanks, along with comments from some of the Wall Street analysts.

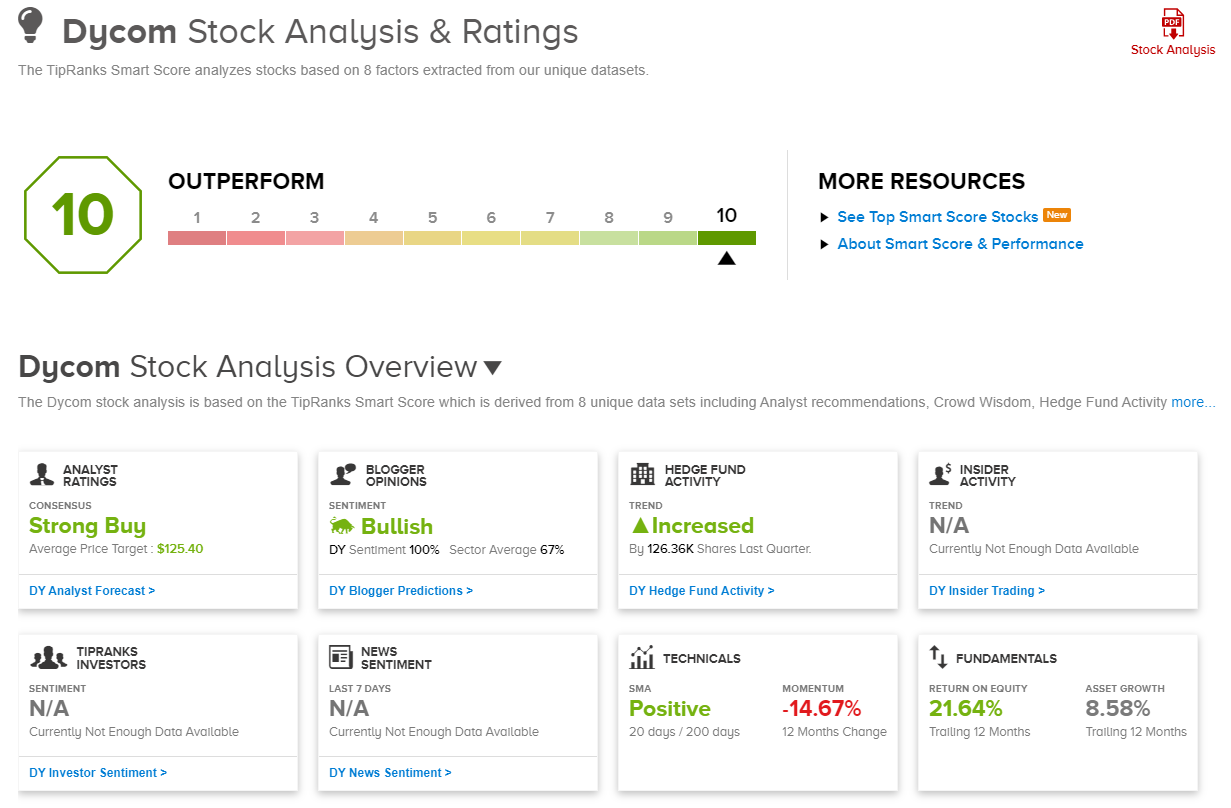

Dycom Industries (DY)

The most urgent need in any business, even more important than the right equipment or a proper facility, is people. Every business, in every field, needs skilled people, doing the work. That’s the role that Dycom fills in the telecommunications industry. Dycom is a contract service provider, with a workforce 15,000 strong made available for a wide range of jobs – planning, engineering, maintenance, wireless construction. If the telecom industry needs it done, Dycom can supply the right workers.

Dycom is a holding company, conducting its operations through a network of 37 subsidiaries. The firm operates out of 556 locations across 49 states and has the scale to meet the needs of both urban and rural regions.

There are plenty of growth opportunities in the telecom field, from the continuing 5G rollout to the expansion of fiber networks worldwide to the development of new technologies, and Dycom has leveraged its ability to staff those positions into strong financial performance. The company saw revenues of $1.04 billion in its last quarterly report, for fiscal 2Q24, a total that was up 7% year-over-year and beat the forecast by $10 million. This revenue translated to earnings of $2.03 per share, or 35 cents per share ahead of expectations.

On the balance sheet, the company finished the quarter with $1.555 billion in total current assets, compared to $1.492 billion six months earlier. The Q2 assets included $83.38 million in cash.

For Craig-Hallum’s 5-star analyst Christian Schwab, the key point to Dycom is the company’s ability to take part in expansions of the national telecom network, fiber buildouts especially. Schwab writes, “Management expects spending from AT&T to normalize heading into next year and we continue to believe that beyond near-term customer spending fluctuations Dycom remains positioned well for longer term growth. Secular trends for expanding fiber deployments to support gigabit-plus broadband connectivity speeds, wireless backhaul, and wireline/wireless converged networks remain intact, along with significant rural fiber deployment opportunities with support from federal and state initiatives for unserved or underserved areas across the country.”

These comments back up the analyst’s Buy rating on the stock, and his $124 price target indicates his confidence in a 29% one-year upside. (To watch Schwab’s track record, click here)

The Strong Buy consensus rating on DY is based on 5 recent analyst reviews, that include 4 to Buy against 1 to Hold. The shares are selling for $95.79 and the average price target, $125.40, is slightly more bullish than Schwab’s, suggesting a 31% gain in the next 12 months. (See Dycom stock forecast)

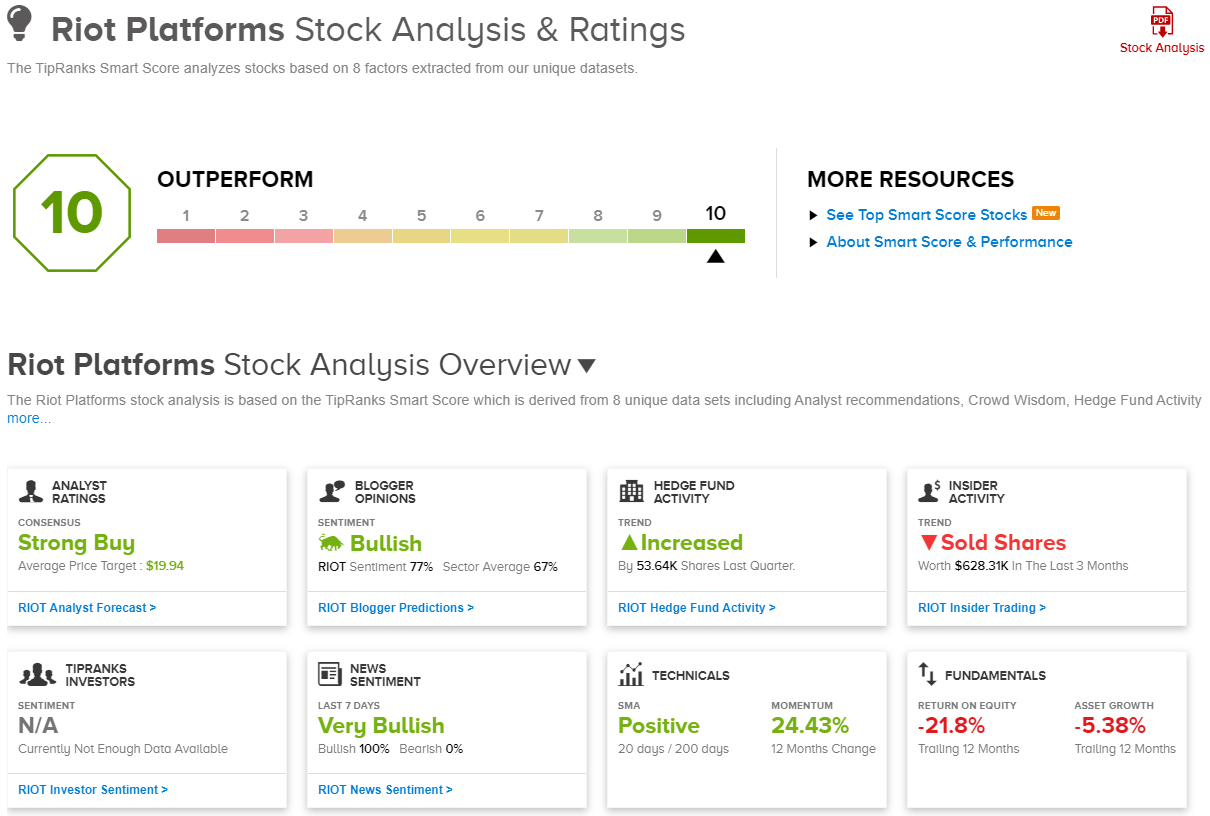

Riot Platforms (RIOT)

Next up, Riot, is a bitcoin miner, with its data center mining ops located in Texas and its ancillary supporting operations based in Denver, Colorado. The company’s chief mining data center is the Rockdale Facility, which is North America’s largest single bitcoin mining facility and boasts 700 megawatts in developed capacity. Overall, Riot’s bitcoin mining operates with a deployed hashrate of 10.7 EH/s.

That hashrate is based on the company’s total deployment of 95,904 mining rigs. Riot, which already has one of the largest fleets of bitcoin miners installed and deployed, has plans to continue its expansion and to reach a deployed hashrate of 12.5 EH/s by the end of this year.

Bitcoin miners make their living by validating and recording transactions on the network and being rewarded for the work with coins, i.e., they mine bitcoins. It takes enormous computing power to do this, so the companies have high overheads – but they can sell off some of the bitcoins produced to fund current operations.

In the company’s last quarter, 2Q23, Riot reported a top line of $76.7 million, up 5% year-over-year but missing the forecast by $8.76 million. The bottom line, while showing a loss of 17 cents per share, was 3 cents better than had been anticipated.

Since those figures were released, the company has published monthly results for August. In the August report, Riot showed that it generated 333 bitcoins for the month. This was down 11% from August of last year and down 19% from July of this year. The company’s bitcoin holdings, however, have been increasing, as its production still far exceeds its liquidity needs; Riot has 7,309 bitcoins on hand as of August 31, for a 9% year-over-year increase. Riot’s bitcoin sales in August netted $8.6 million, up 12% year-over-year.

The data shows potential here, and Cantor Fitzgerald analyst Josh Siegler sees it, too. He takes a bullish view of Riot, writing of the stock, “We continue to believe that RIOT represents the best-in-class Bitcoin miner with significant scale, low energy costs, and no long-term debt. Heading into the halving, we believe Riot is in a unique position to continue to gain share in the Bitcoin mining industry. As a result, Riot remains our top pick in our Bitcoin mining coverage.”

For Siegler, this adds up to an Overweight (Buy) rating, and his $23 price target implies a one-year upside potential of 124%. (To watch Siegler’s track record, click here)

This bitcoin miner’s Strong Buy consensus rating is based on 8 recent analyst reviews, unanimously positive. The stock’s average price target, of $19.94, suggests it will gain 94% this year from the share price of $10.28. (See RIOT stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.