The markets’ professional stock analysts make picking the right equities look easy. But the analysts spend day in and day out with stock data and have built their careers on their stock picks. Retail investors don’t have that advantage when it comes to deciphering the volume of data put up by the markets every day. A tool is necessary to make sense of it and to indicate potentially winning stocks.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

That’s where the Smart Score comes in. The Smart Score is a data tool designed by TipRanks to gather, sort, and collate the mountain of stock data that makes stock picking so difficult. The Smart Score uses a sophisticated AI algorithm to sift through the data and compare every stock to a set of factors known to match up with future share outperformance. The end result is a single score attached to every stock, a simple digit on a scale of 1 to 10, indicating the stock’s likely path forward.

That simple score gives investors a one-second thumbnail sketch for any given stock, a reference that’s easy to use and easy to understand. And the ‘Perfect 10s,’ the stocks with the highest possible Smart Score, are the stocks worth a second look.

The Street’s analysts frequently agree, putting Buy ratings on top-scoring stocks. So let’s take a look at two ‘Perfect 10’ stocks which the analysts like; according to the TipRanks data, these shares have Strong Buy ratings to go along with their high Smart Scores.

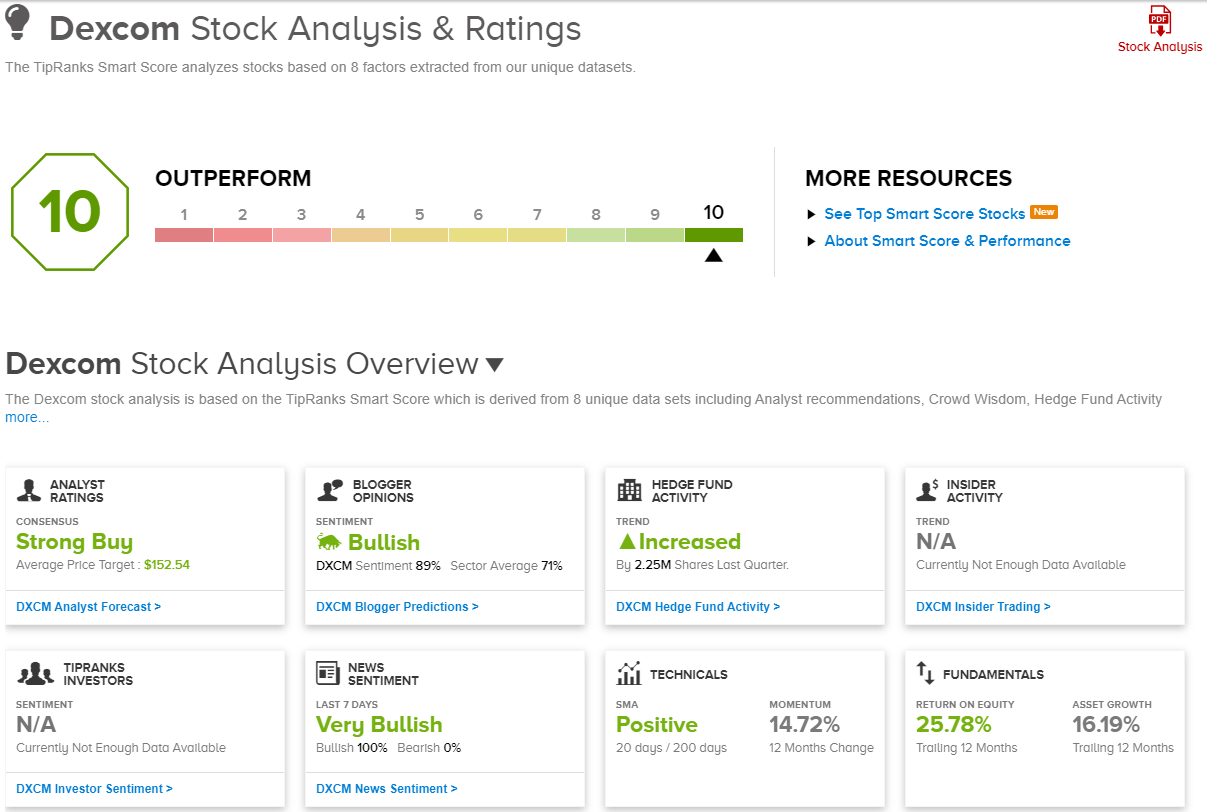

DexCom (DXCM)

For the first Perfect 10 stock on our list, we’ll look to the world of medical devices – specifically, we’ll look at DexCom, a company involved in the design, manufacture, and distribution of continuous glucose monitoring systems (CGMs). These devices frequently hold a vital role in diabetes management, especially for patients with insulin-dependent diabetes using self-administered insulin.

DexCom, from its San Diego base, has become a leader in the use of technology for the treatment of diabetes. The company has developed a line of fully-integrated CGMs; its latest line, the G6, includes a standard automatic applicator, a sensor and transmitter, and a display device, compatible with Apple iOS or Android. Using the system, patients can monitor their glucose levels without finger pricks, and can monitor their sugar levels on their own smart devices.

The system also gives users a wide range of available data, accessible through the linked smart device. Patients can receive high and low blood sugar level alerts, and even alerts that sugar levels are likely to drop dangerously low. In addition, the system can notify patients when to administer insulin doses, and these notifications can be customized, based on meal or work schedules, or even the day of the week.

All of this makes DexCom’s product one of the most flexible CGMs on the market. And even more importantly, DexCom’s Stelo glucose biosensor was recently cleared by the FDA to become the first glucose biosensor for use in the US without a prescription. Stelo is a simple, wearable device strapped to the back of the upper arm, can link to a user’s smartphone, putting the company’s glucose monitoring right at the user’s fingertips. The device is expected to become commercially available in the summer of this year.

Turning to DexCom’s recent financial results reveals revenue from 4Q23, the last period reported, of $1.03 billion, a figure that was up 27% year-over-year and beat the forecast by $10 million. The company’s bottom line came to 50 cents per share by non-GAAP measures, 7 cents per share better than had been anticipated.

All of this adds up to a medical device company that deserves closer scrutiny, and RBC analyst Shagun Singh Chadha has done just that. She is impressed by DexCom’s quality offering in a growing medical market, and especially by the company’s upcoming product launches.

“Diabetes is approaching an endemic state, and we see substantial opportunity for CGM TAM expansion aided by innovation, indication/ geographic expansion, and measurements beyond glucose. DexCom has a multi-year runway ahead. It is poised to be among the fastest-growing large-cap MedTech companies with immediate catalysts in Stelo (first no-prescription CGM) and GLP-1 adoption while driving meaningful OM expansion to industry highs over time. We see room for higher estimate revisions and multiple expansion,” Chadha opined.

These comments back up Chadha’s Outperform (i.e. Buy) rating on DXCM, and her $165 price target implies a one-year upside potential of ~26.5%. (To watch Chadha’s track record, click here)

Overall, the Strong Buy consensus rating on DexCom stock is based on 13 recent analyst reviews, with a lopsided split of 12 Buys to 1 Hold. The shares are selling for $130.46, and their $152 average target price points toward a 17% gain on the one-year horizon. (See DexCom stock forecast)

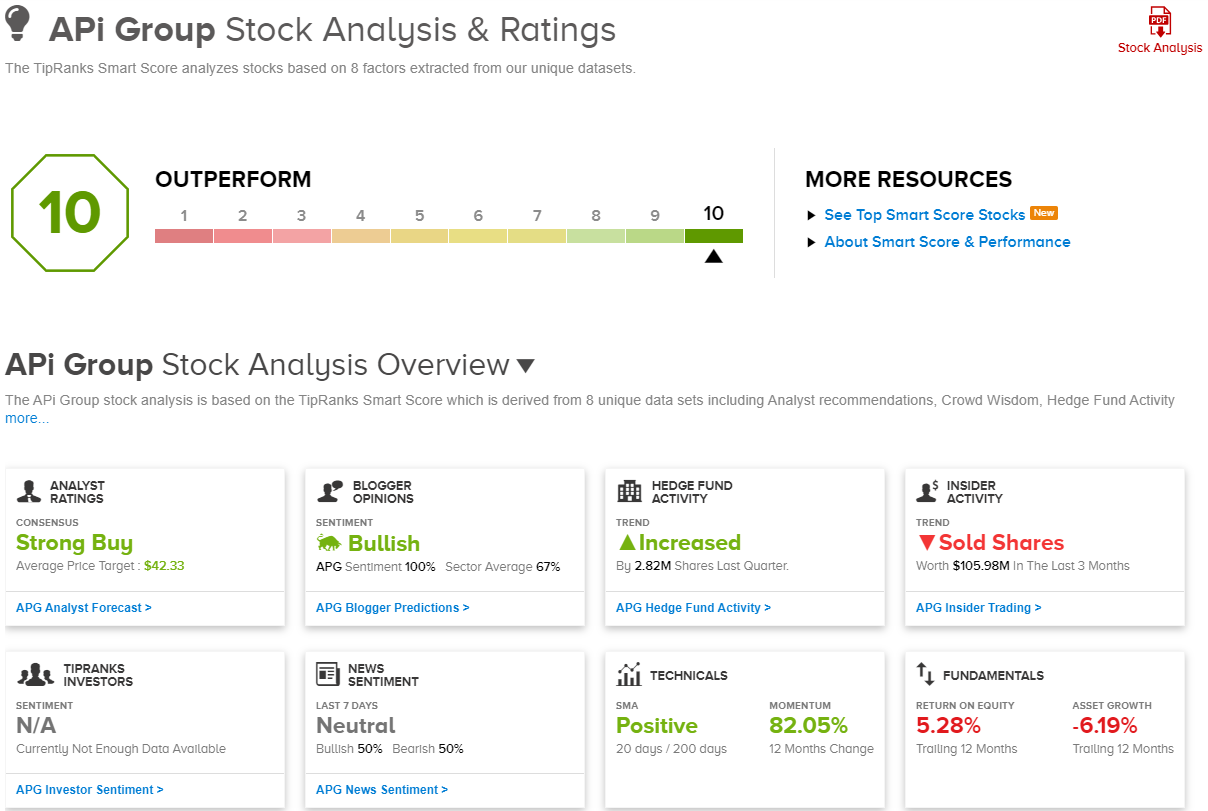

APi Group Corporation (APG)

Next up is APi Group, a professional services company that holds a market-leading position as a provider of specialty services, security, and life safety services across a wide range of industries and a global base. The company acts through a network of subsidiary brands and firms, in more than 500 locations around the world. From its Minnesota base, APi Group tends to a base of client companies working in sectors from transportation, education, healthcare, energy, oil and gas, mining, and industry.

At brass tacks, APi Group’s services include fire protection, alarm monitoring, access control, pipeline integrity, pipe insulation, oil terminal construction, equipment maintenance – it’s a long list. Additional services include facility design, installation, inspections, restorations, repairs, and upgrades. The company describes is mission as proactive risk management, and a business world with zero safety incidents.

This company’s world will never stop needing safety services – and APi Group has leveraged that fact to achieve success. The firm registered $1.76 billion at the top line for 4Q23, the last reported, in-line with the forecast and up 3.5% from the prior year. On earnings, APi Group’s non-GAAP 44-cent EPS was up from 36 cents one year prior, and was a penny better than the expectations.

For Jefferies analyst Stephanie Moore, the bottom line here is simple: this company deserves investor attention. She writes, “We’re bullish on APG’s strategy to expand its recurring and regulatory-mandated inspection/ maintenance services biz, both organically and through tuck-in M&A. We see MSD%+ organic growth and ~200bps of margin expansion in the next 2 years, as APG drives higher-margin recurring revenues, remains selective on project contracts, and realizes ~$80mm (100bps to margin) of prior M&A value capture.”

The 5-star analyst goes on to put a Buy rating on APG shares, along with a $48 price target that shows her confidence in a 26% share gain over the next 12 months. (To watch Moore’s track record, click here)

There are 6 recent analyst reviews here, and the 5 to 1 split in favor of Buy over Hold gives the shares their Strong Buy consensus rating. The stock’s current trading price of $38.05 and average target price of $42.33 together imply a potential one-year upside of 8.3%. (See APG stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.