There’s no doubt the bulls have been charging ahead in 2023. The S&P 500 is up more than 18% year-to-date, while the tech-heavy NASDAQ has been puffing out its chest with a 34% return. Right now, the gains are narrow, resting mainly on a handful of deep-pocketed, big-name tech firms, but there’s a likelihood investor money will start spreading around more widely.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

If the bull market does widen out, it will raise the question of which stocks to buy, and that’s where the Smart Score can narrow the field. The Smart Score’s data collection and collation algorithms gather up the latest information on thousands of publicly traded stocks – and then rates each stock according to a set of factors that have been shown to match up well with future outperformance. Each stock gets a score, based on a 1 to 10 scale, showing how it measures up in the Smart Score’s calculations.

A high rating from the Smart Score indicates stocks with high potential – and the highest rating, the ‘Perfect 10,’ shows a stock that truly deserves a closer look from investors. Several recent picks from the Wall Street analysts bear this out; they are pounding the table on Strong Buy stocks boasting ‘Perfect 10’ Smart Scores. Here are the details.

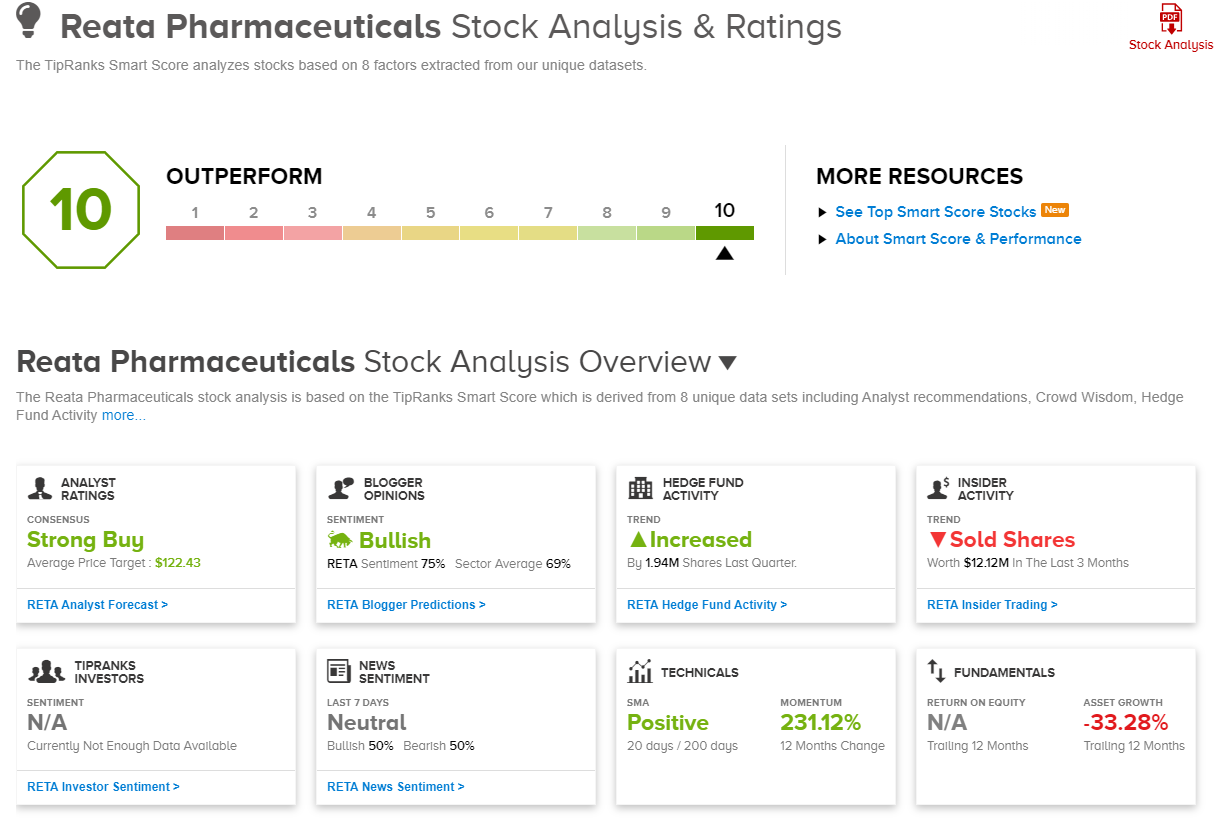

Reata Pharmaceuticals (RETA)

First on our list is Reata Pharmaceuticals, a biotech working on new therapeutic agents for patients with serious and/or life-threatening diseases. The company’s research tracks focus on cell metabolism and inflammation, specifically on the molecular pathways involved in these biological processes. Reata has drug candidates at the pre-clinical, clinical, and commercialization stages.

The company’s leading product is the recently approved drug omaveloxolone, now branded as Skyclarys. This drug is a treatment for the neurological disorder Friedreich’s ataxia, which is a progressive, genetically-based movement disorder that typically strikes patients in late childhood or early adolescence. Skyclarys is the only approved treatment on the market for this condition, and is likely to remain so at least for the near future. It is an oral, once-daily medication, with FDA approval for use in patients aged 16 or older.

The early commercialization stages of Skyclarys are at the heart of Reata’s current story. The company has already received some 500 patient start forms, indicating a strong level of demand. Reata had been holding out on the commercial launch, due to resubmission of the prior approval supplement (PAS) to the NDA; that approval was announced in the last week of June, and drug is now available for use in the US.

In addition, Reata has submitted the marketing authorization application (MAA) for omaveloxolone in Europe, and is in process of responding to the Day 120 list of questions and requests from the European Medicines Agency. The company expects to complete its response to the EMA during 3Q23.

On the research and clinical side, Reata is studying cemdomespib, an HSP90 modulator, as a treatment for diabetic peripheral neuropathic pain (DPNP). The drug candidate is currently undergoing early-stage clinical trials. Reata also has two related drug candidates, RTA 415 and RTA 417, at the pre-clinical. Both are Nrf2 activators, focused on mitochondrial dysfunction.

When we check in with the analysts, we find Tyler Van Buren of TD Cowen taking an upbeat stance on Reata. He sees plenty of potential for the company in having the only Friedreich’s ataxia drug available, and writes, “As the first and only approved FA therapy on the market for the foreseeable future, we believe that Skyclarys will enjoy a robust launch with strong initial uptake that is well maintained over time… KOLs expect to prescribe Skyclarys to all their adult FA patients and to recommend prolonged use over multiple years… Reata’s pipeline could also offer substantial upside with cemdomespib (HSP90 modulator) and RTA 415/417 (next-gen Nrf2 activators.)”

Van Buren goes on to give these shares an Outperform (Buy) rating, and a price target of $140, implying a one-year upside potential of 27%. (To watch Van Buren’s track record, click here)

Wall Street generally is impressed by this biotech and the 8 recent analyst reviews include 7 Buys against a single Hold, for a Strong Buy consensus rating. The shares are trading for $110.86 and have an average price target of $122.43, suggesting an 10.5% gain in the coming year. (See RETA stock forecast)

LifeMD (LFMD)

LifeMD, the second stock we’ll look at, is a telehealth company, offering users and patients a smart device-based platform that eases connections with primary care, diagnostics, and specialized treatment. The company’s platform allows patients to book appointments, meet their doctor online, and even handle chronic and urgent care issues. Patients can receive prescriptions online, and when face-to-face time is needed – for example, to collect blood for lab tests – the company can send a nurse to the patient’s home or direct the patient to a nearby clinic.

While this is not a replacement for regular health insurance coverage, LifeMD does make it easier to access the ordinary, everyday needs and services of the healthcare system. In the long run, this is a service that can benefit both patients and providers, by easing access to the time-consuming run-of-the-mill healthcare activities and maintenance.

The US healthcare sector is enormous, valued at more than $800 billion annually. While telehealth makes up only a small slice of that large pie, the telehealth industry’s total revenue came to $29 billion last year.

That’s a solid foundation to support LifeMD, and the company has leveraged it to its own results. In its last quarterly report, for 1Q23, LifeMD showed a top line of $33.1 million. This was up 14% year-over-year and beat the forecasts by $2.32 million. While the firm is running a quarterly net loss – not uncommon for tech-oriented companies – its EPS loss in Q1, ($0.15 per share), was a penny better than had been expected. In non-GAAP measures, the company did post a profit; consolidated adjusted earnings came to $2 million, or 6 cents per share.

In a point that investors should note, LifeMD made important steps in Q1 toward reducing its cash burn. The firm went through $4.2 million in 4Q22, but its 1Q23 cash burn only came to $678,000, representing a sequential improvement of 84%. The company expects to report a positive free cash flow (FCF) from the middle of this year.

For H.C. Wainwright analyst Yi Chen, all of this adds up to a stock that investors need to consider, particularly the revenue gains and the march toward positive FCF. Chen says of the stock, “Though the company is operating at a lower revenue level compared to the competing players in the direct-to-patient telehealth market, its robust top-line growth, solid gross margin, and near-term potential to achieve positive free cash flow (by mid-2023) compare favorably to competing players in the sector, in our view. We note that LFMD shares trade at a lower EV/Revenue multiple (1.2x) compared to the average of comparable companies’ multiples. Therefore, we believe LFMD is undervalued given its strong commercial performance.”

These comments back up Chen’s Buy rating, and his $9 price target indicates confidence in a robust gain of 117% over the next 12 months. (To watch Chen’s track record, click here)

There are 4 recent analyst reviews here, and they are unanimously positive for a Strong Buy consensus rating. Shares are priced at $4.14, and the $7.50 average price target implies 81% share gains over the one-year time frame. (See LifeMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.