The last two weeks have seen the markets take a rollercoaster ride, that’s for sure. The sudden insolvency and failure of Silicon Valley Bank, and the Federal closures of Signature and Silvergate banks, have triggered worries of an old-fashioned bank run. An announcement by Credit Suisse, that it was having difficulty accessing capital, fed fears that even the major banking names would not be immune to contagion.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

President Biden and Treasury Secretary Yellen have made it clear that account holders of SVB and Signature ‘would be made whole,’ but uncertainty remains around other regional banks. And no one knows just how the Federal Reserve will react, via interest rate policy, at next week’s FOMC meeting.

It’s a confusing situation, one tailor-made for an intuitive data-parsing tool. The Smart Score at TipRanks, is just that – an AI-powered data collection and collation tool, that gathers and sorts the flood of statistical information generated by more than 8,500 publicly traded stocks. The tool then presents that data on an easy-to-use scale of 1 to 10, giving each stock a single digit score based on a distillation of 8 separate factors each of which has proven to match up with equity outperformance. A high Smart Score can’t guarantee that a stock will beat the market indexes – but it does give investors a strong clue toward positive performance, and the ‘Perfect 10’ stocks are always worth a closer look.

So let’s get this ball rolling. Using the Smart Score platform, we pinpointed two stocks that have earned the enviable “Perfect 10” Smart Score. Each also features a Strong Buy rating from the analyst consensus and double-digit upside potential for the coming year. It’s not just a perfect score, it’s a perfect combination of bullish indicators.

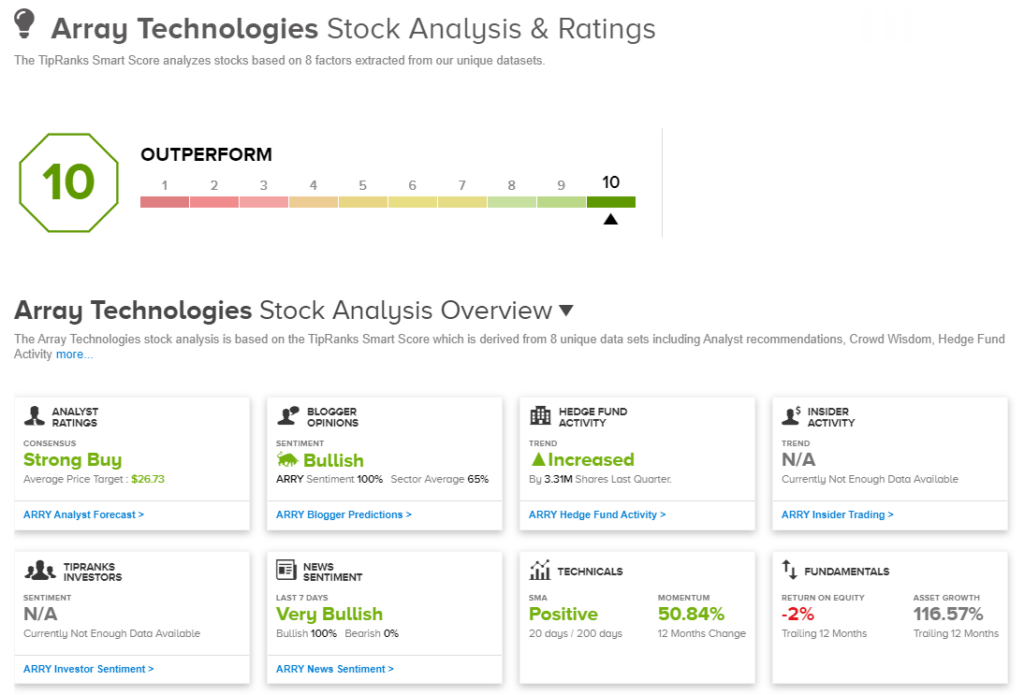

Array Technologies (ARRY)

We’ll start in the solar energy industry, with Array Technologies. This company specialized in solar tracker technology, the combinations of hardware and software needed to keep utility-grade photovoltaic panel arrays properly aligned with the sun, for maximum efficiency. Array’s flagship product, the DuraTrack system, is used in large-scale solar power projects, the types connected to public power generation utilities, and is considered a leading system in the solar tracker field.

Cutting edge companies in rapidly expanding fields will frequently run net losses – and as recently as 2H21, Array was not a net-profitable company. Starting in 3Q22, however, the company turned a corner, and achieved both record revenues and profitability. In Q3, Array posted a company-record top line of $515 million, up from $188.7 million in the prior-year period, and a net income to common shareholders of $28.6 million, compared to the 3Q21 loss of $33. The company’s EPS, at 19 cents per diluted share, beat the 11-cent forecast by a 72% margin and was a dramatic turnaround from the 7-cent EPS loss recorded one year earlier.

Array will report its Q4 and full-year 2022 results on March 21. In the meantime, the company has released preliminary financial results and guidance. Arrays is guiding toward $1.62 billion to $1.64 billion in total revenues for 2022; achieving this would represent a 73% year-over-year revenue increase from the $941 million reported in 2021. The company had $1.9 billion on its order book as of December 31, 2022.

Looking forward, Array is predicting 2023 total revenues in the range between $1.8 billion and $1.95 billion, with a full-year adjusted EPS of 75 cents to 85 cents.

Scotiabank analyst Tristan Richardson covers this stock, and looking at the company’s recent trendlines he takes an unequivocally bullish stand.

“Array is a direct play on the global secular growth trends in utility-scale solar capacity, with its ground-mount tracker product. While near-term uncertainties remain on project timing, related to module availability for developers, in the long term, we look for 15%-20% solar capacity growth, which offers Array a strong secular backdrop as well as the potential for increased market adoption of tracker solutions generally,” Richardson opined.

To this end, Richardson rates ARRY shares an Outperform (i.e. Buy), and his price target, of $26, indicates potential for 52% upside in the coming months. (To watch Richardson’s track record, click here)

The bulls are definitely on the run for ARRY, as the stock has 12 recent analyst reviews with a 10 to 2 breakdown favoring Buys over Holds – for a Strong Buy consensus rating. The shares are priced at $17.07 and the average price target, $26.73, implies ~57% upside by the end of this year. (See ARRY stock analysis on TipRanks)

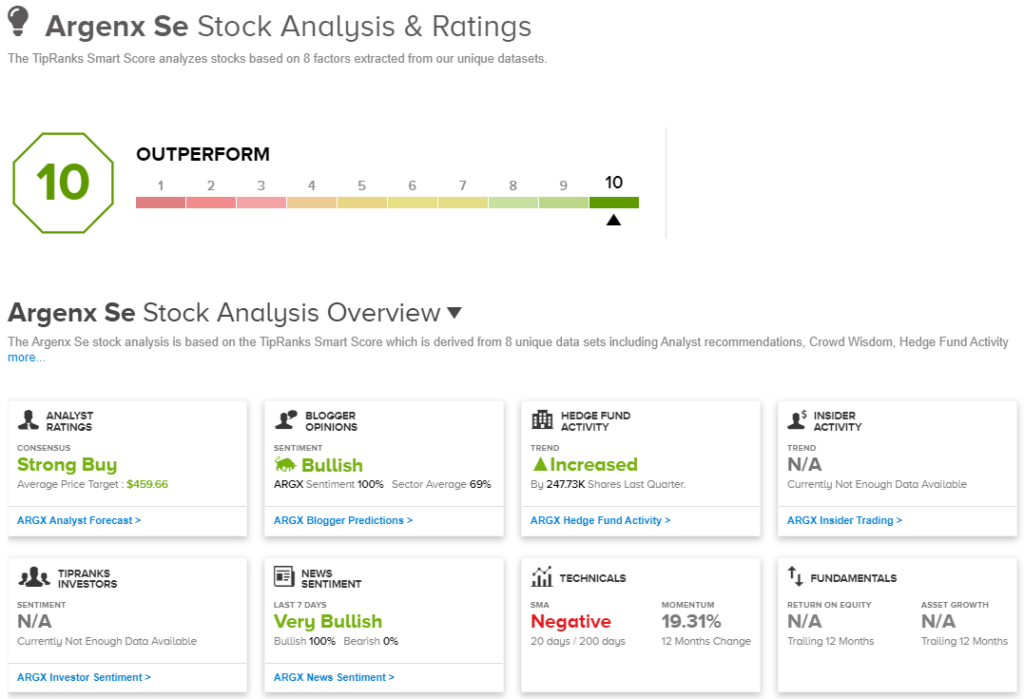

Argenx SE (ARGX)

The second ‘perfect 10’ stock we’ll look at is Argenx, a biopharma firm in the immunology niche, working on new treatments for rare diseases. The company has an extensive pipeline, with nearly 20 separate research tracks investigating the uses and efficacy of 3 different drug candidates.

The leading candidate, efgartigimod, has received approval in the US, Europe, and Japan for the treatment of the rare neuromuscular disease gMG, and the company was focused in 2022 on launch activities for the medication, branded as Vyvgart.

In its 2022 annual report, Argenx gave updated information on the Vyvgart launch. Worldwide, the company notes that there are some 3,000 gMG patients on Vyvgart, and that the drug generated a full-year net product revenue of $400.7 million. In addition, the company is following regulatory processes in multiple countries, including China, the UK, Canada, and Italy, preparatory to additional approvals and commercial launches.

Argenx is also putting efgartigimod through additional clinical trials, for label expansion purposes. These trials are at various stages, with the ADAPT-SC trials being the most advanced. This completed trial was for a neurological application, gMG in adult patients, of the drug, and the company, based on positive topline data, received FDA acceptance of the biologics license application with a PDUFA date of June 20, 2023.

The company’s ADHERE trial, a registrational clinical trial in the treatment of chronic inflammatory demyelinating polyneuropathy (CIDP) is on track to release topline data in 2Q23, and the registrational Phase 2/3 ALKIVIA trial, studying efgartigimod in the treatment of three subtypes of idiopathic inflammatory myopathies, is ongoing. Argenx even has a registrational clinical trial planned for the treatment of thyroid eye disease (TED) planned for initiation in 4Q23.

While we have outlined just the tip of the iceberg on Argenx’s extensive pipeline, these programs are at the heart of the Baird analyst Joel Beatty’s assessment of the stock. Beatty writes: “We now see this as a good entry point into the stock, ahead of what we anticipate will be successful registrational trial results for CIDP in 2Q23 (which could reintroduce a strong acquisition premium into the stock). Also, we anticipate efgartigimod sales for gMG will continue to grow at a good rate, bolstered by SQ formulation approval in June.”

In his view, ARGX shares deserve an Outperform (i.e. Buy) rating, and his $460 price target suggests the stock has room for a 28% upside in the year ahead. (To watch Beatty’s track record, click here)

The Strong Buy consensus rating here shows that the bull are out in force, as evidence by the 15 to 1 breakdown of the 16 recent share reviews, favoring Buys over Holds. (See ARGX stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.