While last year saw a wicked bear market, coupled with high volatility, investors have had an easier time of it so far in 2023. Volatility remains an issue, but it has moderated – and both the NASDAQ and the S&P 500 are up nicely year-to-date. The NASDAQ has gained over 16%, and the S&P is up more than 8%. The Dow is the laggard here, having gained only 2.2% in the same time. It’s a market environment that’s sure to present opportunities for gains – so long as investors can cut through the noise to find them.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

That’s where the Smart Score tool steps in. This tool, sifting the TipRanks database through a set of AI-enabled algorithms, collects and collates the data on thousands of publicly traded stocks – and rates them according to a set of 8 pre-determined factors known to correlate with share outperformance. The factors are combined for each stock, and each stock is given a single-digit rating, a simple score on a scale of 1 to 10, letting investors see at glance where the stock is likely to go. And shares that get a ‘Perfect 10’ Smart Score are more likely than not bound for better things.

So let’s go there. We can dip into the TipRanks database to pull up equities with the best Smart Scores – and then sort them for additional attributes. Doing this, we’ve found two that have earned that Perfect 10 – and are also seriously undervalued; according to the analysts, these Strong Buy stocks present an average upside potential around 90%. Here are the pair, along with comments from the Street’s stock pros.

Viridian Therapeutics (VRDN)

The first stock on our list is Viridian Therapeutics, a clinical-stage biopharmaceutical company with a focus on rare diseases – particularly on thyroid eye disease (TED), for which its pipeline features four active human clinical trials plus two more planned. Viridian also has three additional research tracks, on rare and autoimmune disease conditions. The company is producing its series of therapeutic molecules and monoclonal antibodies through its proprietary antibody discovery and engineering platform.

Viridian has chosen to base its discovery program on a patient-centric model, and is using known and proven biology and technology to more efficiently craft its range of precision medicine products. The company’s efforts are targeting disease areas which are known to be commercially established, an approach that promises to ease the way toward eventual profitability.

The leading drug candidate in Viridian’s pipeline is VRDN-001, a monoclonal antibody thought to serve as a full antagonist of insulin-like growth factor 1-receptor (IGF-1R). Viridian is currently assessing the drug in several clinical studies for the treatment of active and chronic TED.

In January, the firm disclosed positive data from the third, low-dose cohort in its ongoing Phase 1/2 clinical study of patients with active TED while Viridian has also initiated dosing on five patients in the Phase 3 THRIVE trials in patients with active TED, with results expected by the middle of next year. On a shorter time scale, Viridian expects to report additional proof-of-concept results for VRDN-001 as a treatment for patients with chronic TED in 2Q23.

Viridian has a subcutaneous program in the pipeline, as well, with several drug candidates under investigation – including VRDN-001. Of these programs, VRDN-002 – a novel anti-IGF-1R monoclonal antibody that incorporates technology for half-life extension – is the most advanced, and proof-of-concept data is expected by YE2023.

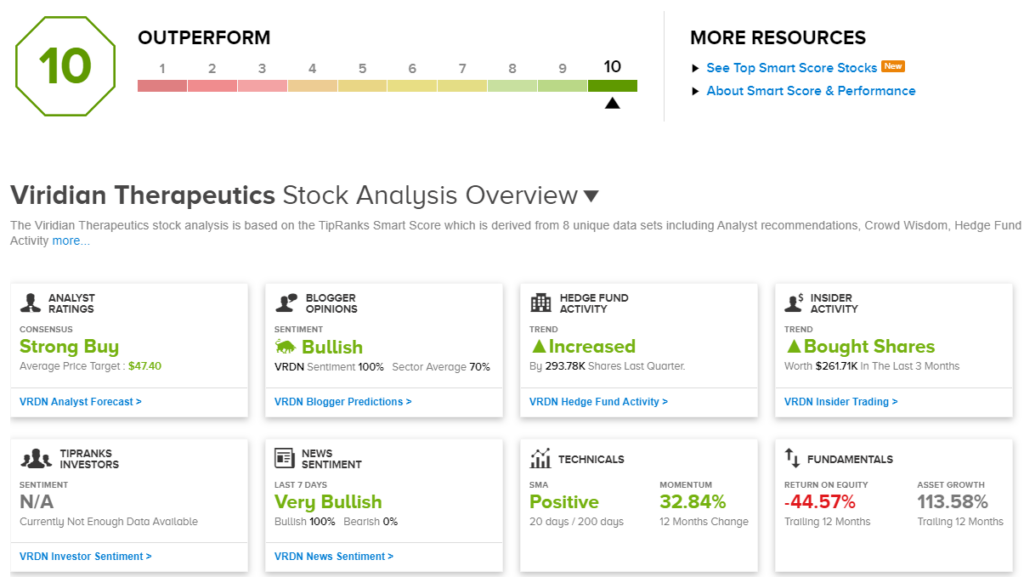

Turning to the Smart Score, we find that Viridian’s shares rate high on most of the 8 factors. Prominent among them are the news sentiment, which is 100% positive, and the financial blogger sentiment, also 100% positive. Among the hedges tracked by TipRanks, the funds increased their holdings by more than 293,000 shares last quarter, and in the last 3 months, corporate insiders have bought $261,700 worth of VRDN stock. This adds up to a Perfect 10 on the Smart Score.

Stifel analyst Alex Thompson has based his coverage of the stock on an optimistic view of Viridian’s pipeline when compared to its potential competition. Thompson writes, “We think VRDN is pursuing an interesting/pragmatic approach with three IGF-1R antibodies (lead program VRDN-001 in Ph3) designed to improve upon Tepezza in multiple ways including efficacy (magnitude/rate) and ROA (subcu vs. IV), while also working to expand into the larger Chronic/Low-CAS TED population in parallel. Ultimately, we think that VRDN will be able to achieve meaningful minority share of the growing TED market with their subcu/IV portfolio (~25% of the IGF-1R market). We model VRDN achieving ~1.7B in peak US revenue risk-adjusted at 66%. Our base-case is comparable efficacy to Tepezza in Ph3, but view superior efficacy as driving greater upside.”

Along with this outlook, Thompson gives the shares a Buy rating, and a $49 price target that implies a 94% upside potential for the next 12 months. (To watch Thompson’s track record, click here.)

Wall Street clearly doesn’t mind a bullish take on this one, as the stock has 11 positive reviews for a unanimous Strong Buy consensus rating. The stock’s $25.20 trading price and average target of $47.50 combine for an 88% upside on the one-year horizon. (See Viridian’s stock forecast.)

IDEAYA Biosciences (IDYA)

Next on our list is IDEAYA, another biopharmaceutical researcher. IDEAYA is working on precision medicines as new treatments in the field of oncology, basing its research platform and pipeline on molecular diagnosis methods to precisely match the patient population to the finely targeted synthetic therapeutic agents. IDEAYA’s team is world-class, and is leveraging its expertise in clinical studies, translational biology, small molecule therapeutics, and oncology to the development of the pipeline projects.

That pipeline is extensive and includes several pre-clinical studies backing up three candidates in clinical studies: darovasertib, IDE397, and IDE161. The first of these has two clinical trials underway, while the others are each the subject of one active trial. All three focus on specific cancers featuring specific gene deletions or mutations.

Darovasertib, the leading candidate, is subject of trials broadly addressing ocular melanomas, both as a monotherapy and in combination with crizotinib. The combo is the subject of a Phase 2 study of metastatic uveal melanoma (MUM), and the company has targeted 2Q23 to 3Q23 for a data update on ‘approximately 20 first-line MUM patients.’ An earlier data release, in September of last year, showed positive results, including 89% of patients with tumor shrinkage, and an 83% disease control rate. As a monotherapy, darovasertib is undergoing a Phase 2 trial against Neoadjuvant / Adjuvant Uveal Melanoma (UM), with interim clinical data expected later this year.

The second drug candidate, IDE397, is a small molecule inhibitor being tested in combination with AMG193, as a treatment in patients with solid tumors showing MTAP deletion. This is a significant patient bloc, totaling some 15% of solid tumor patients. The company is continuing to develop its Phase 1/2 clinical trial program for this indication. A Phase 2 clinical study is also assessing IDE397 as a monotherapy in a “basket” of MTAP-null Non-Small-Cell Lung Cancer (NSCLC), Esophagogastric Cancer and Bladder Cancer.

Finally, IDE161, a PARG inhibitor candidate, has entered the clinic in a Phase 1/2 study featuring patients whose tumors adhere to specifically defined biomarkers based on genetic mutations. The IND for this drug candidate was cleared in 4Q last year, and the trial was initiated in 1Q23.

On an important financial note, IDEAYA has the deep pockets to support these clinical trials and trial initiations. The company reported having $373.1 million in cash and other liquid assets at the end of last year.

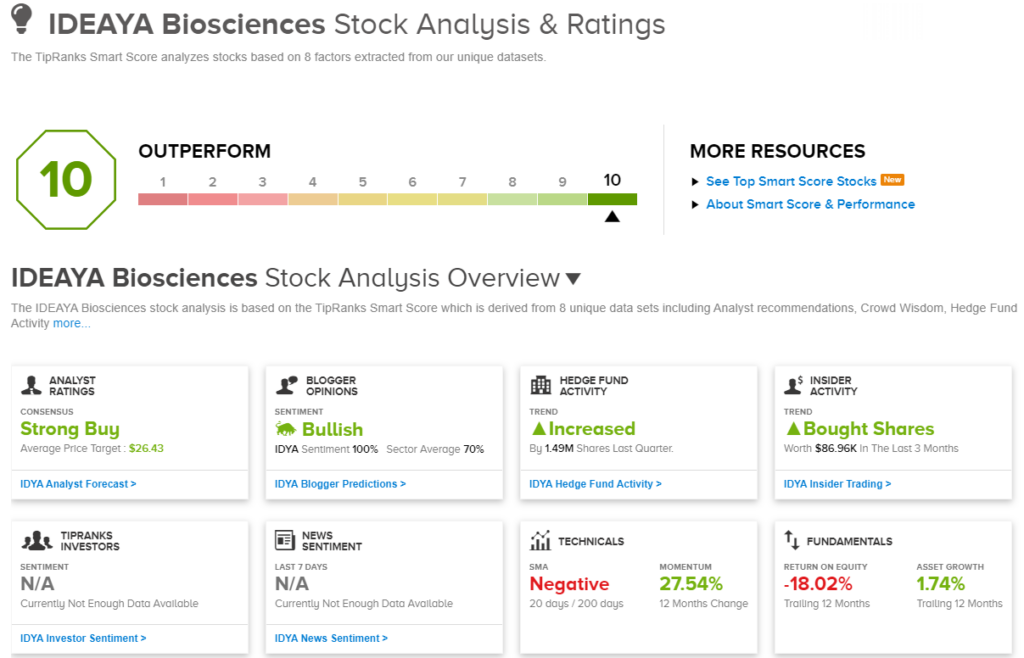

On the Smart Score, we find several reasons for optimism, including in the hedges, which bought $1.5 million worth of IDYA stock last quarter, and in the financial bloggers who are 100% positive here. The shares also saw purchases from the insiders, who, in the last 3 months, have picked up $87,000 worth of the stock.

IDYA has also caught the attention of Berenberg analyst Zhiqiang Shu, who writes of it, “We view IDYA as an attractive opportunity for three key reasons: 1) a potential near-term value driver is the success of PKC inhibitor darovasertib in metastatic uveal melanoma (MUM) studies; 2) substantial upside can potentially be derived from MAT2A inhibitor IDE397, a possibly best-in-class drug that is a cornerstone therapy for MTAP-deleted cancers; and 3) PARG inhibitor IDE161, which represents a new class of cancer drugs. We think many data-related catalysts over the next 12-18 months could likely provide upside to IDYA. Reported 2022 year-end cash of $373m should support operations into 2026.”

These comments support Shu’s buy rating, while his $26 price target suggests a one-year gain of 88% over the next 12 months. (To watch Shu’s track record, click here.)

The Strong Buy consensus rating on IDEAYA is based on 7 recent analyst reviews, which break down 6 to 1 in favor of Buy over Hold. The stock’s average price target is $26.43, implying a 91% one-year upside from the current trading price of $13.80. (See IDEAYA’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.